Source: Pixabay

- Risk-on sentiment remains perky

- UK Q3 GDP -0.2%-BoE says it’s the start of prolonged recession

- US dollar trading defensively, AUD outperforms

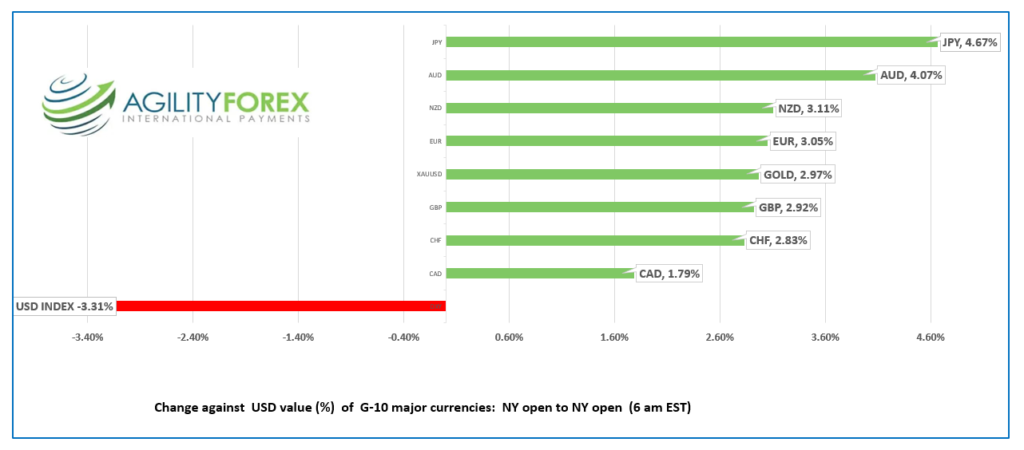

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3308-12, overnight range 1.3269-1.3359, close 1.3321

USDCAD lost 1.79% between Thursday’s opening level and todays. That is a decent move, but it paled in the face of the 4.67% slide in USDJPY, and it was a lot less than the Antipodean currency moves.

The catalyst was the better-than-expected US inflation data which rose 7.7% y/y from 8.2%. Traders reacted like it was confirmation that the US rate hike cycle was close to a peak. Bonds soared driving the US 10-year Treasury yield down to 3.811% from 4.117% pre-CPI.

The falling US dollar lifted commodity prices with WTI oil rising from $84.75/barrel to $89.54/b overnight. USDCAD traders mostly ignored the move as WTI has been rangebound in a $82.00-$93.00/b range since October 18.

The USDCAD underperformance may be because the CAD/US 10-year yield spread is still -65 bp’s in favour of the US.

Bank of Canada Governor Tiff Macklem may have undermined USDCAD after he said “The tightness in the labour market is a symptom of the general imbalance between demand and supply that is fuelling inflation and hurting all Canadians.” That suggests the peak Canadian interest rate is not in sight.

It is Remembrance Day in Canada and many parts of the world. Canadian banks are closed but the TSX is open. In the US, many banks are closed but the NYSE and bond market are open.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish while trading below 1.3320 looking for a break below 1.3260 to extend losses to 1.3210. A break above 1.3320 targets 1.3360.

The longer term technicals suggest USDCAD is extremely oversold and therefore vulnerable to a correction to 1.3510.

For today, USDCAD support is at 1.3260 and 1.3210. Resistance is at 1.3320 and 1.3370.

Today’s range 1.3260-1.3330

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

“Whoosh!” That was the sound on Wall Street yesterday, after US inflation was cooler than expected. S&P 500 futures exploded higher and finished the day with a 5.54% gain. FX traders crashed the party and torpedoed the US dollar

Traders seemed to believe “Mission Accomplish-Job done.” George W Bush was about 18 years too early when he said those words about the US invasion of Afghanistan, and financial markets may be a tad early as well.

They turned a deaf ear to remarks from Cleveland Fed President Loretta Mester who did not seem too impressed with the lower CPI reading. She said, “This morning’s October CPI report also suggests some easing in overall and core inflation. On the other hand, services inflation, which tends to be sticky, has not yet shown signs of slowing. Given the current level of inflation, its broad-based nature, and its persistence, I believe monetary policy will need to become more restrictive and remain restrictive for a while in order to put inflation on a sustainable downward path to 2%”.

Traders preferred comments from Philadelphia Fed President Patrick Harker (non-voter) and Kansas City Fed President Ester George (voter) advocating for a slower pace of hikes.

Fed Chair Powell has not said anything (publicly) about yesterday’s CPI report and on November 2, warned that the ultimate level of interest rates will be higher than previously expected.

Thursday’s price action may be a fantasy. The reality is that supply chain issues are still a problem, the war in Ukraine continues, Europe will have an energy crisis when winter arrives, and the US and EU are heading into, or already are in, a recession.

EURUSD boosted the currency pair from 0.9937 yesterday to 1.0323 in NY today. Traders dismissed warnings from the Economic and Financial Affairs Council that the EU would be in a recession next year and also ignored the hike in the inflation forecast to 6.3%.

GBPUSD rocketed higher, rising from 1.1356 Thursday to 1.1795 today as the fall-out from the US CPI continues. The UK economy shrank 0.2% in the three months to September, which was better than expected but still points a recession.

USDJPY was in free-fall, dropping to 138.78 today, from 146.50 yesterday. Ministry of Finance officials are happy as they made a tidy profit from selling $42 billion USDJPY in the 148.00-152.00 area.

AUDUSD and NZDUSD joined the risk-on rally. AUDUSD climbed from 0.6393, pre-CPI to 0.6686 today., making it the best performing major G-10 currency today.

The Michigan Consumer Sentiment report is due.

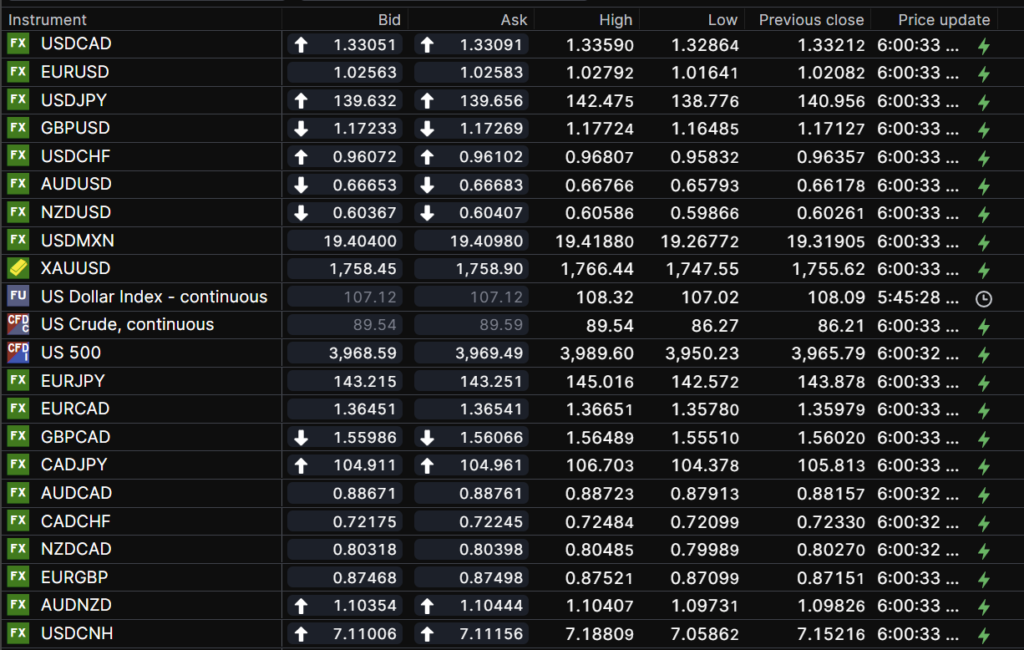

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

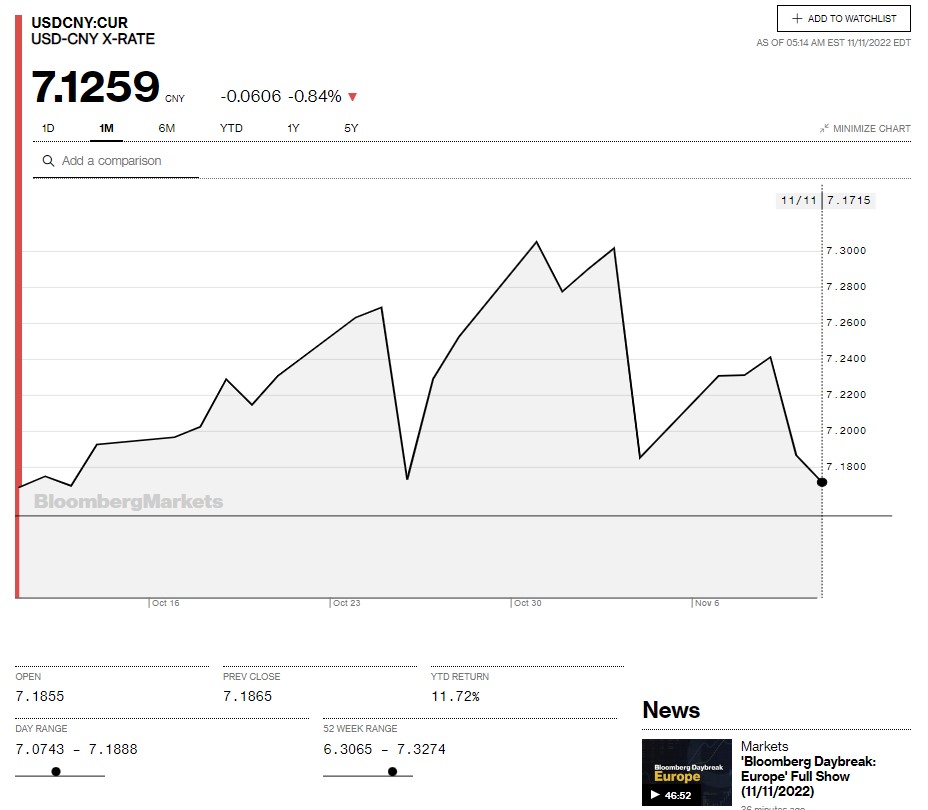

China Snapshot

Today’s Bank of China Fix: 7.1907, previous 7.2422

Shanghai Shenzhen CSI 300 rose 2.79% to 3788.44

China National Health Commission slightly ease covid controls. Quarantine for close contacts cut to 5 days in centralised location from 7. Quarantine for inbound travellers cut to 8 days from 10.

Meanwhile Haizhu district of Guangzhou extended its Covid lockdown until November 13.

Chart: USDCNY 1 month

Source: Bloomberg