Photo: HDClipartAll.com

January 6, 2023

- Stellar Canadian jobs data 104,000 (forecast 8,000)

- US nonfarm payrolls rise 223,000,

- US dollar opens sharply higher compared to Thursday-slides after NFP

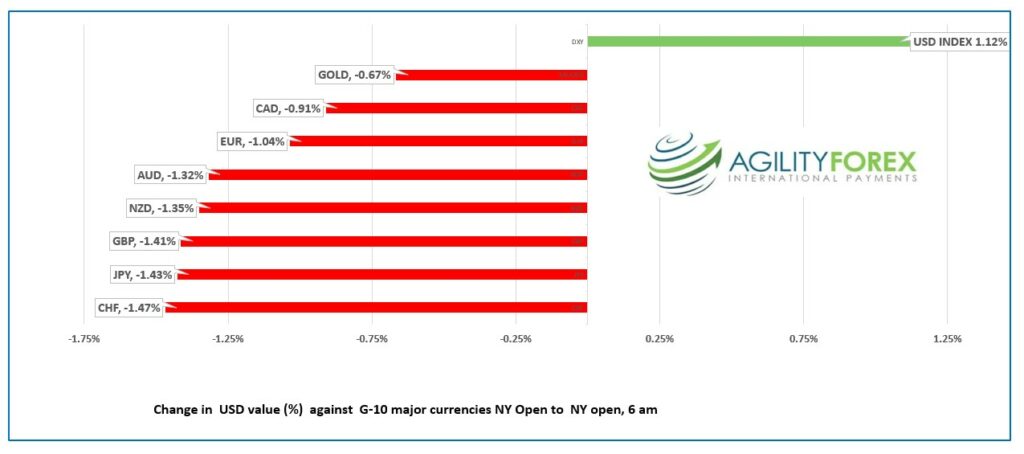

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3629-33, overnight range 1.3540-1.3663, close 1.3570

Canada gained 104,000 jobs in December, crushing the consensus view for just an 8,000 gain. USDCAD dropped from a pre-data level of 1.3655 to 1.3529. The sell-off got a boost from the US employment data which wasn’t as strong as feared.

Yesterday, USDCAD rallied from 1.3472 to 1.3594, yesterday, then extended those gains to 1.3663 in early NY, pre-employment reports.

Canada’s unemployment rate dipped to 5.0% from 5.1%

The strength of today’s employment data will ensure the BoC hikes rates by 25 bps at the January 25 monetary policy meeting because just like in the US, a tight labour market is inflationary.

USDCAD technical outlook.

The intraday technicals are turning bearish after failing to break resistance int the 1.3670 are and the subsequent break below support at 1.3570. A decisive breech below 1.3570 sets the stage for a retest of support in the 1.3440-50 area.

For today, USDCAD support is at 1.3520 and 1.3470. Resistance is at 1.3630 and 1.3660

Today’s range 1.3510-1.3610

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar was bid ahead of today’s US employment report and offered in the aftermath.

US nonfarm payrolls rose 223,000 in December, slightly higher than the 200,000 forecast. However, it looks like traders were positioned for a substantially higher result which is why S&P 500 futures are up 0.90% and the US 10-year yield is back down to yesterday’s 3.68% low.

Average hourly earnings dropped to 4.6% y/y from the downwardly revised 4.8% in November. This result is the kind the Fed wants to see before it pauses rate hikes. The FOMC minutes made it pretty clear that inflation will not return to target as long as nominal wage growth remain elevated due to tight labour markets.

EURUSD is consolidating losses in a 1.0497-1.0544 range, after dropping from 1.0631 to 1.0516 yesterday. The single currency barely moved after better-than-expected economic data. Eurozone inflation dropped to 9.2% y/y vs forecast 9.7% and 10.1% in November, mainly due to lower energy costs. Retail Sales, Industrial Confidence and Economic sentiment reports also topped expectations. The intraday technicals are bullish above 1.0280, looking for a retest of the July 2021 downtrend line at 1.0680.

GBPUSD dropped from 1.2077 to 1.1875 yesterday, then extended those losses to 1.1854 in NY today. Prices rebounded to 1.1934 after the US employment data. UK House prices dropped in December which merely reinforced the weak outlook for the domestic economy.

USDJPY traded in a 133.24-134.77 range overnight then dropped to the overnight low following the US data. A drop in the 10-year Treasury yield to yesterday’s lows spurred the retreat.

AUDUSD consolidated yesterday’s losses in a 0.6733-0.6787 range. Prices were weighed down by widespread US dollar demand but got a bit of support following news a Chinese firm placed an order for Australian coal, the first in two years.

US ISM Services PMI is also on tap today.

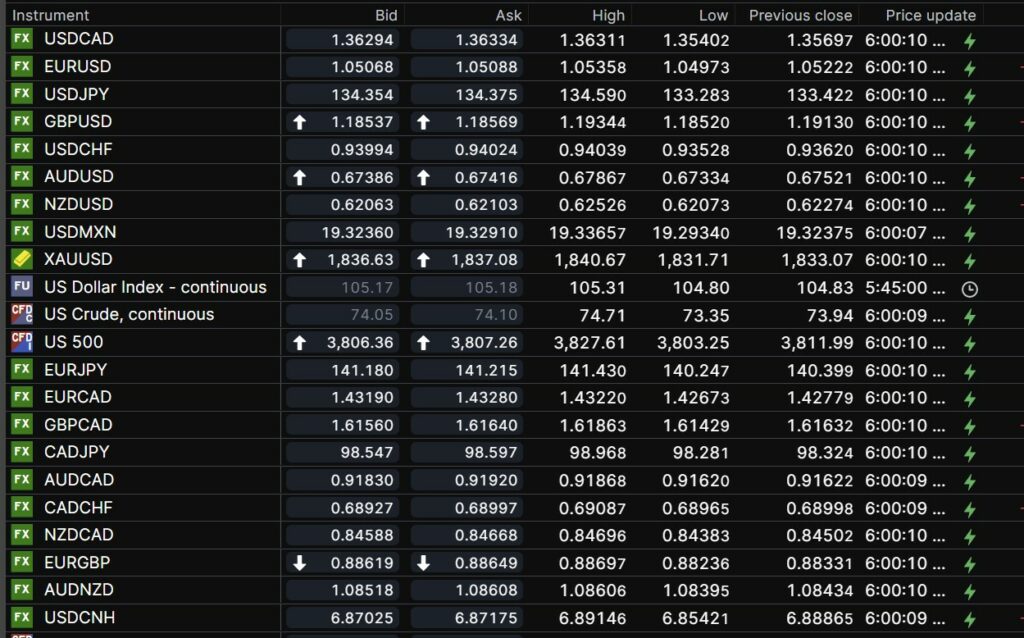

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

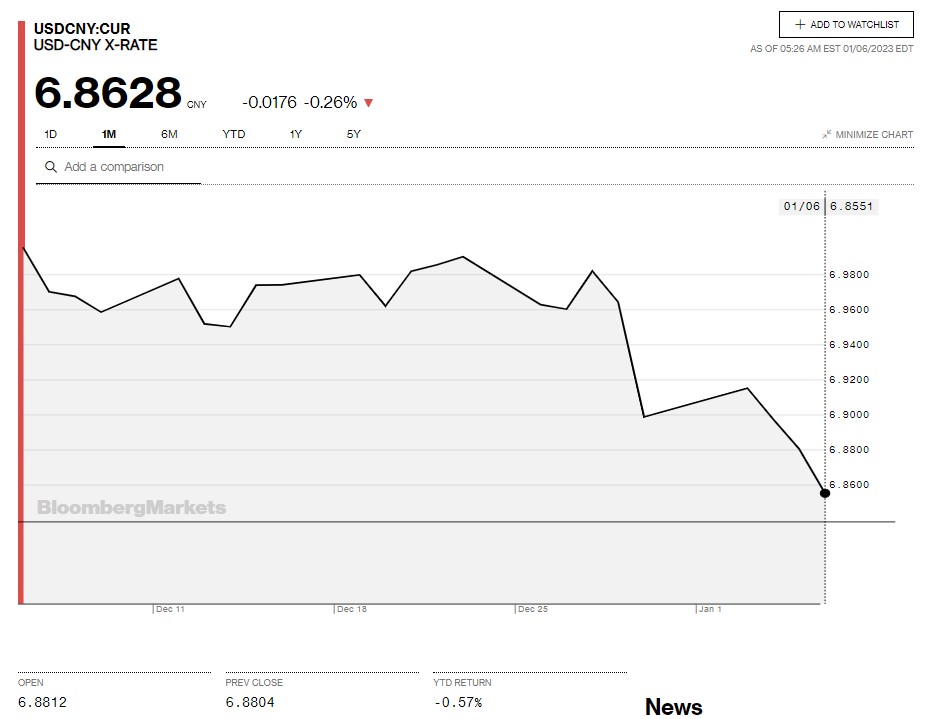

China Snapshot

Today’s Bank of China Fix: 6.8912, previous 6.8926

Shanghai Shenzhen CSI 300 rose 0.31% to 3980.89

PBoC and Banking regulator are allowing banks in cities where housing prices have fallen, to issue mortgages at rates below the current floor.

Chart: USDCNY one month

Source: Bloomberg