Photo: Some AI

July 31, 2023

- China data shows its economy still struggling.

- Eurozone inflation falls more than expected in July.

- USD ending July with sharp losses, CAD gains lag G-10

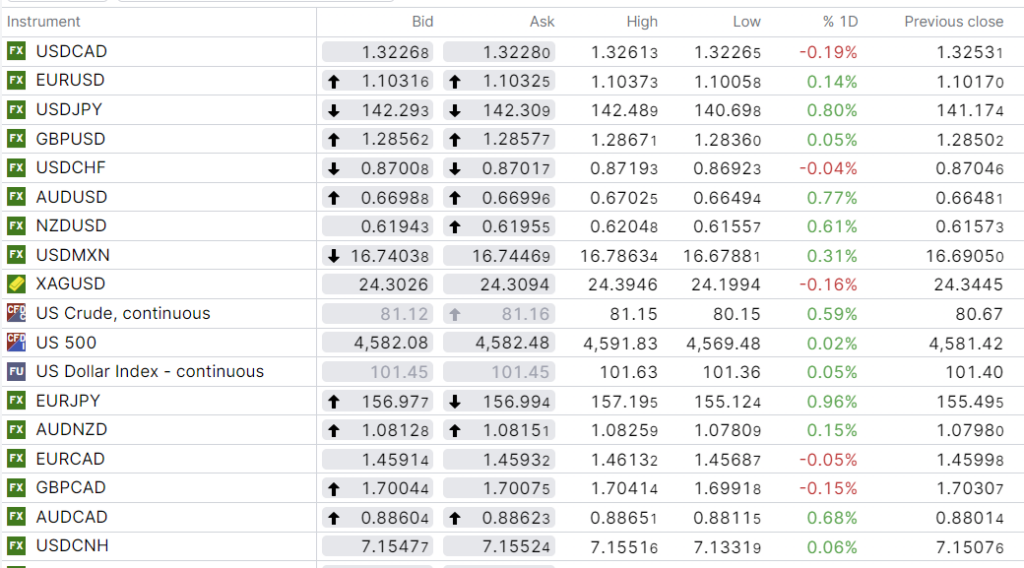

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3225-29, overnight range 1.3216-1.3261, close 1.3253

USDCAD retreated overnight due to improved global risk sentiment sparking broad US dollar weakness. Nevertheless, USDCAD remains well above last week’s low of 1.3148. That level may be seen today due to the monthly portfolio rebalancing flows.

USDCAD is getting a bit of support because although May GDP rose 0.3% (as expected but below the BoC forecast), it is expected to slow to 0.2% m/m gain in June.

WTI oil prices started to climb last week and continued to do so overnight, rising from $80.15-to $81.40/b. Goldman Sachs analysts claim the rise is because global demand is at a record higher while Saudi Arabia’s supply cuts are starting to bite.

USDCAD Technical Outlook

The USDCAD technicals are negative with todays retreat below 1.3230 that suggests further losses to 1.3160. A break below the 1.3140-60 area targets 1.3090.

The USDCAD downtrend from the beginning of June is intact while prices are below 1.3270 which keeps the focus on a test of long-term support in the 1.2980-1.3000 area.

For today, USDCAD support is at 1.3190 and 1.3140.. Resistance is at 1.3240 and 1.3270. Today’s range 1.3140-1.3240.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

It’s the end of the month and the start of a busy week, which is chock-full of top-tier economic data, including Canadian and US employment reports on Friday. In addition, the Reserve Bank of Australia (RBA) and Bank of England (BoE) monetary policy meetings are on Tuesday and Thursday, respectively.

Geopolitical tensions are simmering. Poland fears an invasion from Belarus by Russia’s rebellious Wagner Group. Russia’s nutbar deputy chair of the Security Council, Dimitry Medvedev, threatened to use nuclear weapons if Ukraine’s counteroffensive is successful.

The Bank of Japan made things interesting in Asia when they intervened to prevent JGB yields from rising by making special bond purchases. Asian markets closed with healthy gains, led by a 1.26% rise in Japan’s Nikkei thanks to BoJ actions boosting USDJPY. Australia’s ASX 200 rose a mere 0.9% ahead of the RBA meeting tomorrow.

European bourses are mixed. The German DAX is up just 0.5%, while the UK FTSE 100 is down 0.11%. The US 10-year Treasury yield is slightly higher at 3.98%.

The latest release of better-than-expected US data is fueling discussions that the Fed will achieve a “soft landing.” Minneapolis Fed President Neel Kashkari agrees, saying that the base case is that the economy will be slowing but avoid a recession. He also did not rule out another rate increase.

EURUSD traded in a 1.1006-1.1040 band with prices underpinned by better than expected Eurozone Q2 GDP (actual 0.6% q/q, forecast 0.4%) while July inflation ticked lower (actual -0.1%, forecast 0.3%). German Retail Sales fell 0.8% m/m in June which was worse than expected.

ECB President Christine Lagarde repeated that the central bank could pause or could hike rates in September, saying, “We are committed to returning inflation to our target in a timely manner, and for this, we need a sufficiently restrictive policy in terms of level and length.”

GBPUSD inched higher, rising from 1.2836 to 1.2972 due to broad, but modest US dollar weakness. Traders are looking ahead to Thursday’s BoE meeting.

USDJPY soared overnight, rising from 140.70 to 142.49 before sliding to 142.17 in NY. The volatility occurred after the BoJ intervened in the bond market to drive JGB yields lower.

AUDUSD climbed from 0.6649-0.6717 range due to improved risk sentiment. Traders are undecided as to whether the RBA will raise rates by 25 bps or leaves them unchanged.

The Chicago PMI index is expected at 43, vs 41.5 in June.

FX high, low, previous close

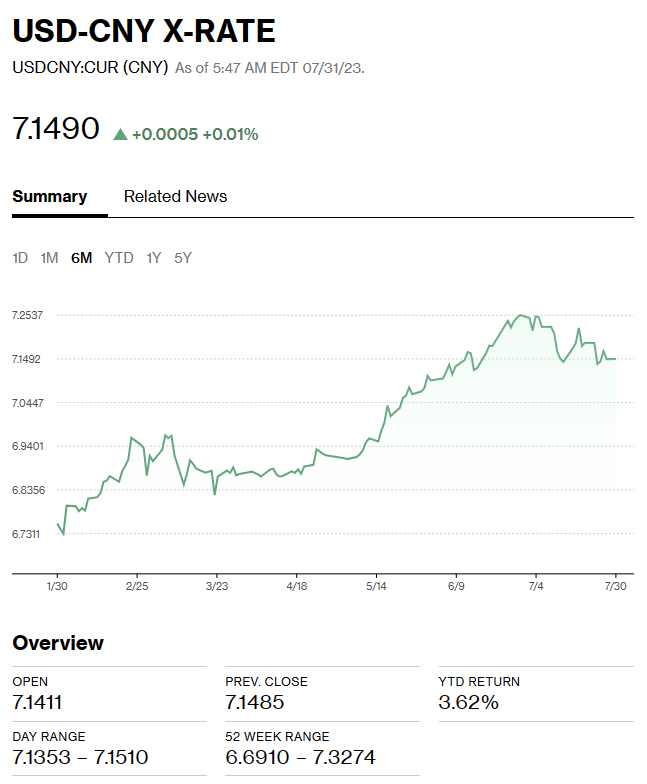

China Snapshot

Bank of China Fix: 7.1305 , forecast 7.1524, previous 7.1338.

Shanghai Shenzhen CSI 300 rose 0.55% to 4014.63.

NBS July Manufacturing PMI 49.3 (forecast 49.2, June 49.0)

Non-Manufacturing PMI 51.5 vs June 53.2.

Manufacturing PMI contracted for the 4th consecutive month, but it was still better than expected. China’s National Development and Reform Commission released a slew of measures to encourage domestic demand, including building more shopping malls.

Chart: USDCNY 6 month

Source: Bloomberg