Photo:Bing Image Creator

September 1, 2023

- US Nonfarm payrolls rise 187,000 same as July.

- Canadian economy shrinks 0.2%, as expected.

- USD opens narrowly mixed ahead of key US data

August FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3500-04, overnight range: 1.3490-1.3556, close 1.3507

USDCAD closed out August with a loss of 1.95% which placed it in the middle of the G-10 pack, ahead of the Japanese yen and the antipodean currencies. However, it started September as the best performing currency by gaining 0.22% overnight , which quickly changed after the weak Canadian GDP data and the tame US employment report. USDCAD spiked to 1.3556 in the aftermath of the data, then dipped to 1.3535.

Canada Q2 GDP was sharply weaker than expected, with the economy shrinking by 0.2% rather than growing tepidly at 1.2% y/y. The preliminary estimate for July is 0.2%, the same as in June. Statistics Canada says, “The slowdown was attributable to continued declines in housing investment, smaller inventory accumulation, as well as slower international exports and household spending.” That is music to the ears of Bank of Canada policymakers who are seeing hard evidence that the 475 basis points of rate hikes since March 2022 are having the desired effect. The BoC is likely to leave rates unchanged at next Wednesday’s meeting.

Canada and the US are closed for Labour Day on Monday.

USDCAD Technicals

The intraday USDCAD technicals flipped from bearish to bullish following the Canadian and US data with the rally above1.3530 negating the short term downside. Support at 1.3490 was tested and it held with the subsequent rally above 1.3540 suggesting further gains toward 1.3640 are likely.

For today, USDCAD support is at 1.3490 and 1.3440. Resistance is at 1.3560 and 1.3610. Today’s range 1.3490-1.3570

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

“The US dollar finished August with robust gains across the G-10 spectrum, despite giving back some of the rally in the last week of the month. The gains were mainly due to expectations that US interest rates would go higher and stay restrictive for longer than expected. NZDUSD was the biggest loser, falling 3.21%, mainly due to the Reserve Bank of New Zealand’s dovish bias.

However, overnight FX activity was a different story. G-10 currencies traded sluggishly, not unlike a fat man running in deep sand – lots of effort for little progress.

Nonfarm payrolls rose 187,000 in August, easily beating the “whisper number” of 150,000, and the consensus forecast of 170,000. The Bureau of Labor Statistics noted “The unemployment rate rose by 0.3 percentage point to 3.8 percent in August, and the number of unemployed persons increased by 514,000 to 6.4 million. Both measures are little different from a year earlier, when the unemployment rate was 3.7 percent, and the number of unemployed persons was 6.0 million.”

This was a market friendly report in that it showed the Labour market softening which downgraded rate hike risks. The US dollar dropped against the majors (except CAD), S&P 500 futures rallied 0.55% while the US 10-year Treasury yield barely budged from its pre-data level of 4.08%.

EURUSD consolidated yesterday’s losses in a 1.0828-1.0892 range. Weaker than expected Eurozone Manufacturing PMI (actual 43.5 vs. forecast 43.7 and July 43.7) and position adjustment ahead of today’s NFP limited gains.

GBPUSD shuffled in a 1.2636-1.2691 range then popped to 1.2713 after today’s US employment report. The gains did not last. Soft UK data weighed on prices. Manufacturing PMI was a tad higher than expected at 43 (forecast 42.5) but still very weak, while UK House prices fell 5.3% y/y. Gains are limited due to concerns that the Bank of England may be less hawkish than the Fed. That view was underscored by recent comments from Bank of England Chief Economist Huw Pill, who suggested rates may not go as high as the market is pricing.

USDJPY dropped to 144.50 in the wake of the tame NFP report after peaking at 145.71 overnight. USDJPY also traded with a negative bias due to Chinese stimulus activity and soft US Treasury yields. Traders ignored news that Capital Spending fell from 11% in Q1 to 4.5% in Q2 (forecast 5.4%) and unchanged Manufacturing PMI data.

AUDUSD traded in a 0.6446-0.6519 with the peak occurring post-NFP Prices are underpinned by the latest Chinese stimulus attempt and the better-than-expected Caixin China Manufacturing PMI result.

NZDUSD chopped in a 0.5943-0.5988 range then rallied to 0.6009 in NY.

US ISM August Manufacturing PMI expected at 47 (previous 46.4).

Top of Form

FX high, low, open

Source: Investing.com

China Snapshot

Bank of China Fix: today 7.1788, expected 7.2967, previous 7.1811.

Shanghai Shenzhen CSI 300 rose 0.70% to 3791.49.

PboC cuts banks foreign currency reserve requirements to 4%, effective September 15, from 6.0% currently.

Caixin Manufacturing PMI rose to 51. In August (forecast 49.3)

Hong Kong stock markets closed due to Typhoon Saola.

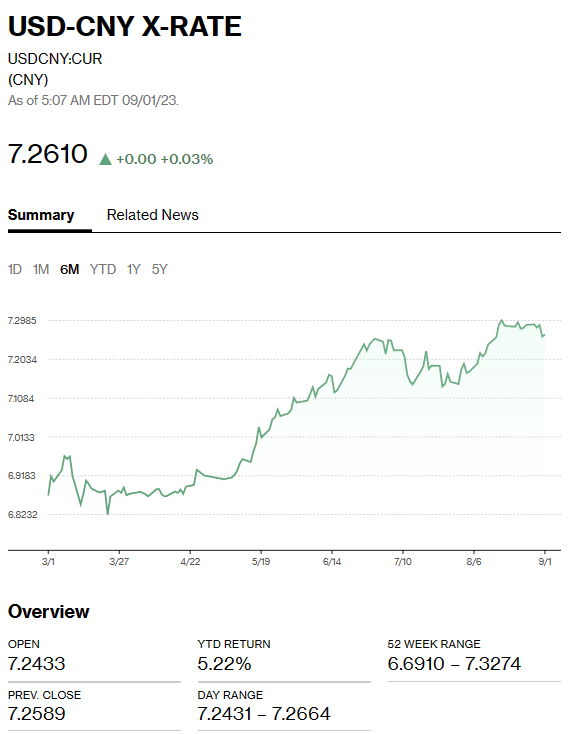

Chart: USDCNY 1 month

Source: Bloomberg