Source: Pixabay

- China cuts RRR ratios, effective December 5

- Early close for US bond and stock markets

- US dollar opens flat to slightly firmer-JPY underperforms

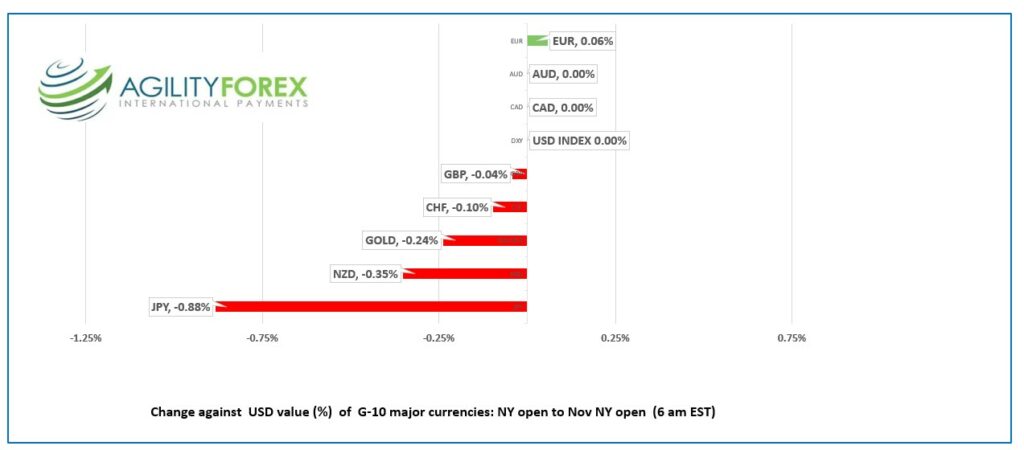

FX at a glance:

Source: IFXA Ltd/RP

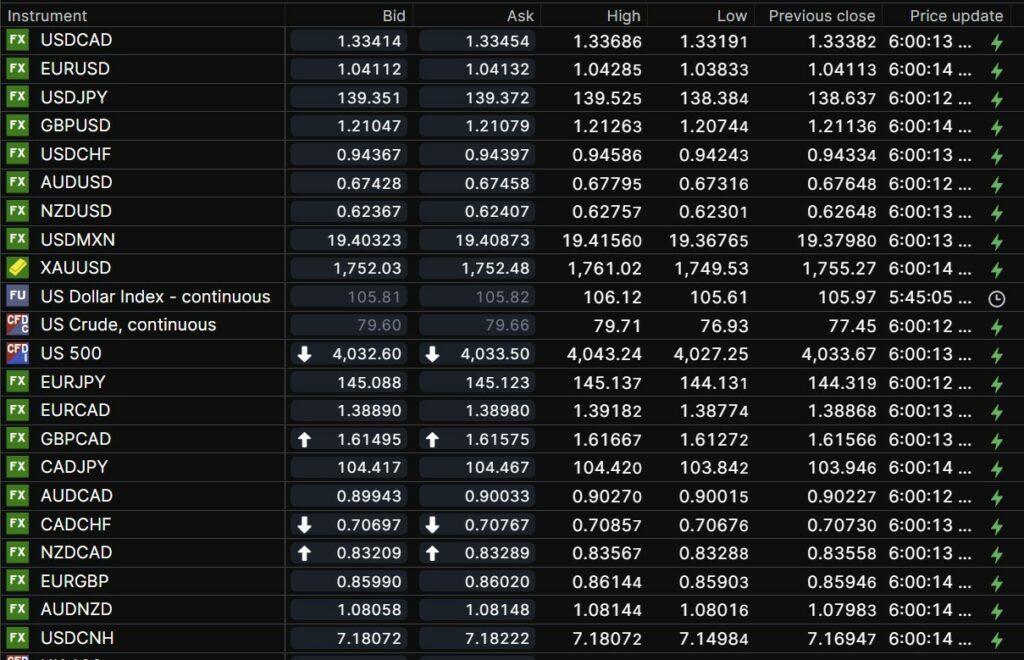

USDCAD Snapshot: open 1.3341-45, overnight range 1.3320-1.3369, close 1.3338

USDCAD dipsy-doodled in another uneventful FX session overnight. Traders are reluctant to get involved due to the World Cup and Black Friday, an unofficial US holiday.

Former Bank of Canada Governor Stephen Poloz said he thinks that the Canadian economy is more sensitive to interest rate hikes than it was before and said higher Canadian debt loads is a vulnerability. He also said that trying to slow inflation with rate hikes is like stopping a car with lousy brakes.

The Bank of Canada is expected to hike rates by 50 bps in December.

WTI oil prices remain under pressure as rising Covid cases in China suggest reduced demand. The G7 is still trying to get an agreement on a Russian oil price cap. Many analysts say that discussions about a $65-$70/barrel cap will not have much impact on Moscow, as that is where Russian crude is trading.

There are no Canadian economic reports and FX trading will be very quiet.

USDCAD Technical outlook

The intraday USDCAD technicals are neutral and little changed from yesterday. A break above 1.3440 will extend gains to 1.3570 while a move below 1.3310 targets 1.3210.

Longer term, the USDCAD uptrend from June 2021 is intact while prices are above 1.2780, while the downtrend from October 2022 guides prices lower while below 1.3540.

For today, USDCAD support is at 1.3310 and 1.3270. Resistance is at 1.3370 and 1.3430.

Today’s range 1.3310-1.3370

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

It was another dull, slow overnight session and it won’t get much better today.

US Markets were closed Thursday and stock and bond markets close early today. Americans are focused on Black Friday shopping deals while most of Europe is fixated on the World Cup.

China announced a 25 bp cut in the Reserve Requirement Ratio effective December 5 but positive sentiment from the stimulus is tainted by the report of 32,695 new covid cases.

The Chinese covid cases raise fears that Xi Jinping’s strict covid-zero policies will drag domestic growth down and lower global oil demand. Lower oil prices will help lower inflation in many countries and thereby slowing the pace of rate hikes.

Asia equity indexes closed mixed with Japan’s Nikkei 225 sliding 0.35% while Australia’s ASX 200 climbed 0.24% in quiet trading. European bourses are lower but not far from unchanged while the UK FTSE 100 index rose 0.20%. S&P 500 futures are flat. The US 10-year Treasury yield is 3.709%.

EURUSD traded in a 1.0383-1.0429 range. Prices dropped to the low when Gfk Consumer Confidence Survey and Q3 GDP data were released then bounced to 1.0420 in the aftermath. GfK described consumer sentiment as continuing to stabilize suggesting the crash in sentiment has come to an end.

Q3 GDP rose 1.3% q/q a tick higher than the 1.2% forecast The Federal Statistical Office said, “Overall, the German economy remains robust.”

EURUSD technicals are bullish above 1.0220, looking for a break above 1.0490 to extend gains to 1.0620.

GBPUSD traded sideways in a 1.2074-1.2126 range and is in the middle of that band in early NY. Prices are underpinned by general US dollar weakness and talk the Fed will slow the pace of rate increases. The short term technicals are bullish above 1.1920.

USDJPY climbed to 139.52 in Europe from an Asia low of 138.34. Tokyo inflation data was higher than expected (actual 3.8% y/y, forecast 3.6%, October 3.5%), leading to some speculation that the BoJ will need to tweak its Yield Curve Control policy.

AUDUSD traded aimlessly in a 0.6732-0.6780 range and opened in NY today, unchanged from yesterday.

There are no US economic reports today.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 7.1201, previous 7.1281

Shanghai Shenzhen CSI 300 fell 0.44% to 3756.81

PboC cuts Reserve Requirement Ration by 25 bps, effective December 5 which is expected to release CNY 500 billion of long-term liquidity. PboC says weighted average for the RRR of financial institutions is 7.80%

Covid cases rise to 32,695

Chart: USDCNY 1 month

Source: Bloomberg