Photo:wikipedia

February 1, 2023

- “To Pivot or not to Pivot”-What will Jay say?

- Eurozone Core HICP falls 0.8% m/m in January, unchanged at 5.2% y/y.

- US dollar consolidates yesterday’s losses.

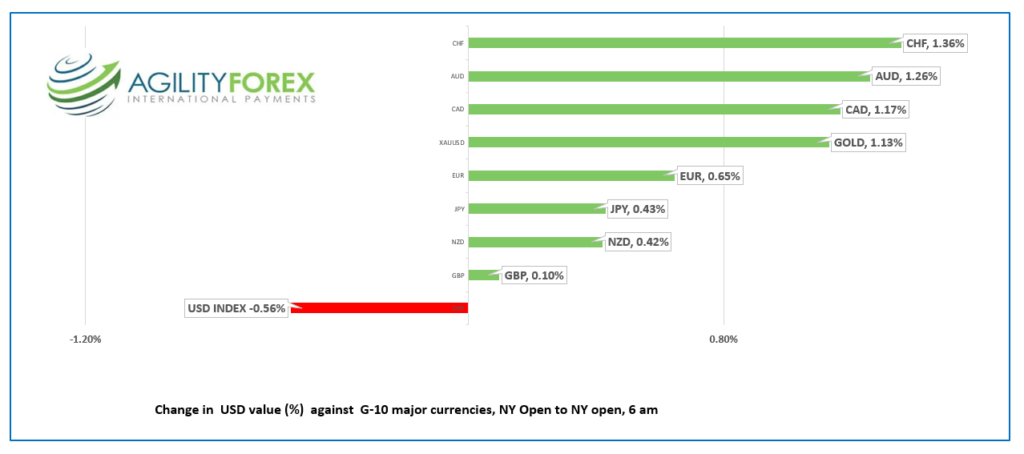

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3309-13, overnight range 1.3291-1.3323, close 1.3307

USDCAD had a bullish bias in early NY trading as souring risk sentiment seemed to overwhelm concerns about month end portfolio rebalancing flows. It didn’t last. The strong S&P 500 index performance in January (+6.16%) sparked a wave of USDCAD selling as portfolio managers scrambled to rebalance.

USDCAD fell from a peak of 1.3470 to a low of 1.3301 then consolidated the losses overnight.

Canada’s real GDP inched up 0.1% in January which was expected and not a factor for traders. However, economists suggest that the results point to stronger growth in Q4 2022.

WTI oil prices rallied from $76.59/barrel yesterday to close at $79.04/b, then consolidated the gains in a $76.79-$7970/b range overnight. Traders are awaiting the outcome of today’s FOMC meeting.

USDCAD Technical Outlook

Yesterday’s bullish USDCAD break-out proved not to be bullish, but merely a head fake, and served only to eliminate weak short USDCAD positions. The overnight move below support in the 1.3300-10 zone suggests a test of the June uptrend line at 1.3260. A downside break targets 1.3150, then 1.2960.

USDCAD needs to break above 1.3410 to suggest a short-term bottom.

For today, USDCAD support is at 1.3290 and 1.3260. Resistance is at 1.3350 and 1.3390

Today’s range 1.3280-1.3380

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Residual US dollar selling from portfolio rebalancing flows competed with positioning ahead of today’s FOMC meeting. The market wants the Fed to provide a clearer window as to when they will pivot, but a host of Fed policymakers have indicated that the timing for such a move, is not right. If the Fed sticks to its previously communicated view that interest rates need to remain in restrictive territory for longer than expected, the US dollar will rally, and equities will fall.

ADP employment change rose 106,000 compared to the forecast for a 178,000 increase and well below last month’s upwardly revised 253,000 gain. Despite evidence to the contrary, many analysts use the ADP data as precursor for nonfarm payrolls, which helps explain why the US dollar slid after the results were released.

EURUSD traded in a 1.0853-1.0896 range then climbed to 1.0908 after the ADP data. Headline Euro area inflation dropped from 9.2% in December to 8.5% y/y in January. However, the more important Core CPI remained unchanged at 5.2% y/y, suggesting a hawkish ECB meeting outcome tomorrow.

GBPUSD rose to 1.2343, post ADP, after wallowing in a 1.2305-1.2333 range overnight. A more hawkish then expected Fed outcome today, combined with rising recession fears in the UK, leave GBPUSD vulnerable to a retest of support at 1.2250.

USDJPY traded with a negative bias in a 129..37-130.40 range with the low posted in NY. The Jibun Bank Manufacturing PMI was unchanged at 48.9.

AUDUSD rallied from 0.70380 to 0.7092, underpinned by better-than-expected S&P Global Manufacturing PMI (actual 50 vs forecast and previous 49.8) and more positive risk sentiment.

NZDUSD climbed to 0.6457 from 0.6419, partly because unemployment rate report didn’t deviate much from the previous data, and reinforces the RBNZ’s economic outlook.

Today’s US ISM Manufacturing PMI is expected at 48, the same result as December.

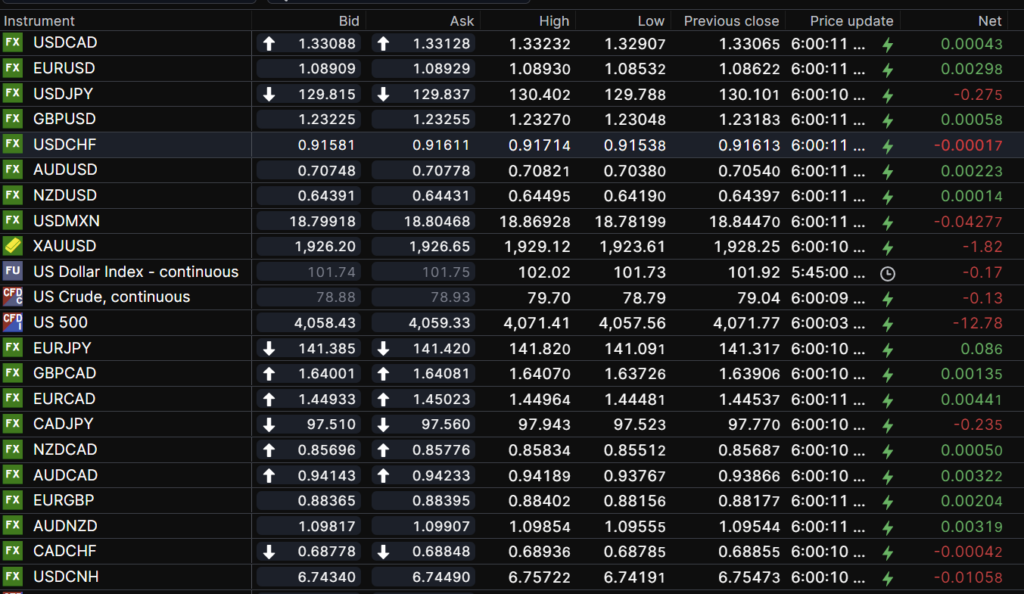

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

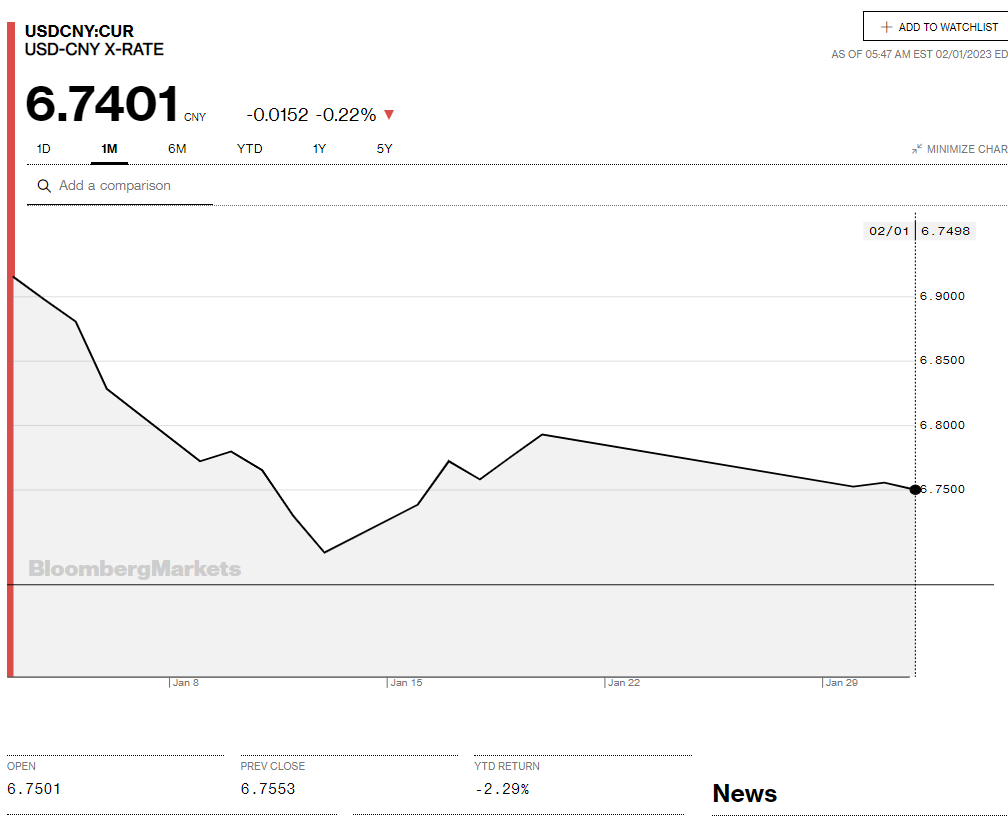

China Snapshot

Bank of China Fix: 6.7492, Previous 6.7604

Shanghai Shenzhen CSI 300 rose 0.94% to 4195.13.

Caixin January Manufacturing PMI 49.2 (forecast 49.5, December 49)

Chart: USDCNY 1 month

Source: Bloomberg