Photo:Bing Image Creator

August 25, 2023

- Markets on hold until Powell speaks at 7.00: am PDT.

- German GDP and Ifo data weigh on EURUSD.

- USD dollar consolidates yesterdays gains.

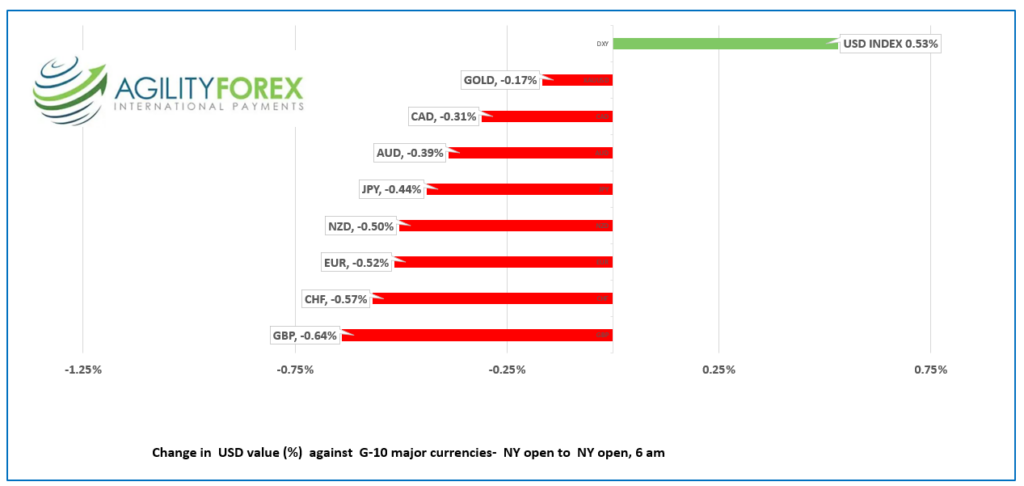

FX at a Glance

Source: IFXA/Raymond Peters

USDCAD Snapshot: open: 1.3586-90, overnight range: 1.3570-1.3602, close 1.3583

USDCAD rallied yesterday and consolidated the gains overnight with the direction determined solely by US dollar sentiment. There isn’t any notable Canadian data today and even if there was, it would be ignored as the greenback is the tail that is wagging this dog.

If Powell’s remarks are more hawkish than expected, USDCAD will rally to 1.3750. Conversely, a dovish Powell would knock USDCAD down to 1.3360. Neutral comments will lead to more 1.3360-1.3640 consolidation.

Oil prices squeezed out gains, with WTI rising from $78.88/b-$80.18/b overnight, mainly because of broad-based US dollar selling pressures. The oil market is unsettled with concerns that

Saudia Arabia could announce further production cuts and talk that the US may ease sanctions on Venezuelan oil.

There are no Canadian economic reports today.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3560, looking for a break above 1.3605 to extend gains to 1.3660. A break below 1.3560 targets 1.3510, then 1.3460.

The uptrend line from August 1 comes into play in the 1.3500-05 area.

For today, USDCAD support is at 1.3560 and 1.3510. Resistance is at 1.3610 and 1.3660. Today’s range 1.3520-1.3620

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

Markets have been rather choppy this week. Wall Street rallied from Monday to Wednesday, then erased the gains yesterday. The US 10-year Treasury yield rose to 4.356% by Wednesday, dropped to 4.186% yesterday, then climbed to 4.256% this morning. And the US dollar was quietly bid all week, with the US dollar index (USDX) climbing from 102.91 on Tuesday to 104.96 yesterday, then consolidating the gains in a 103.99-104.26 range overnight.

The catalyst for the volatility is Fed Chair Jerome Powell, and he hasn’t said anything yet. That will change at 7:05 am EDT when Mr. Powell mimics Moses and delivers his Sermon from the Hole.

Markets are obviously pricing in a hawkish outcome and conveniently ignored Philadelphia Fed President Patrick Harker’s comments yesterday when he suggested the “Fed has probably done enough.” Traders will be sorely disappointed if Mr. Powell hints that rates have peaked but will remain at current levels for some time.

ECB President Christine Lagarde may also provide EURUSD traders with some insight into the European interest rate outlook.

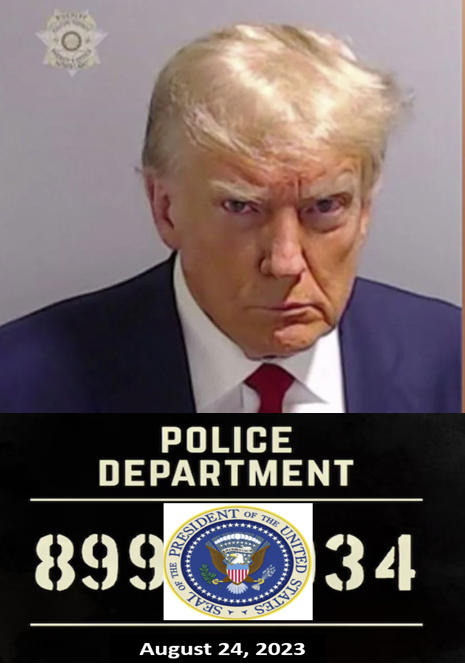

There was another current of uncertainty rippling through markets overnight in the form of former President Donald Trump being booked at the Fulton County jail in Atlanta. It’s hard to ignore the fact that a former president of the world’s most powerful and heavily armed country is facing charges of racketeering and conspiracy in relation to the 2020 election. To make matters worse, he’s the front-runner for the Republican nomination in the 2024 Presidential election. Interestingly, the other seven candidates seem to stand by him, considering him favorably.

Wall Street closed in the red and Asian equity indexes followed suit. Japan’s Nikkei 225 index lost 2.05% while Australia’s ASX 200 dropped 0.93%. European bourses are trading with an optimistic bias and a 0.73% increase in the French CAC 40 index is leading the pack higher. S&P 500 futures are grinding higher and have risen 0.46%, while the US 10-year Treasury yield is steady at 4.247%.

EURUSD dropped from 1.0816 to 1.0767 on the back of weak German Ifo data. The ifo Business Climate Index slipped to 85.7 points in August, down from 87.4 points in July, the fourth consecutive decline. Prices recovered to 1.0800 in early NY due to improved risk sentiment from higher equity prices. German economic growth was flat in Q2.

GBPUSD traded negatively in a 1.2561-1.2604 range but scraped back to 1.2600 in NY as risk sentiment improved. Traders ignored the Gfk news that August consumer confidence improved 5 points to -25 compared to -30 in July.

USDJPY climbed steadily, rising from 145.80 to 146.25 before retreating to 146.00 when risk sentiment turned positive. Tokyo CPI ticked down to 2.9% y/y in August compared to 3.0% in July.

AUDUSD is at the top of its 0.6403-0.6427 range but continues to trade defensively due to the contrast between a hawkish Fed and dovish RBA.

The US Michigan Consumer Confidence Survey (forecast unchanged at 71.2) will be lost in the furor around Powells speech.

Top of Form

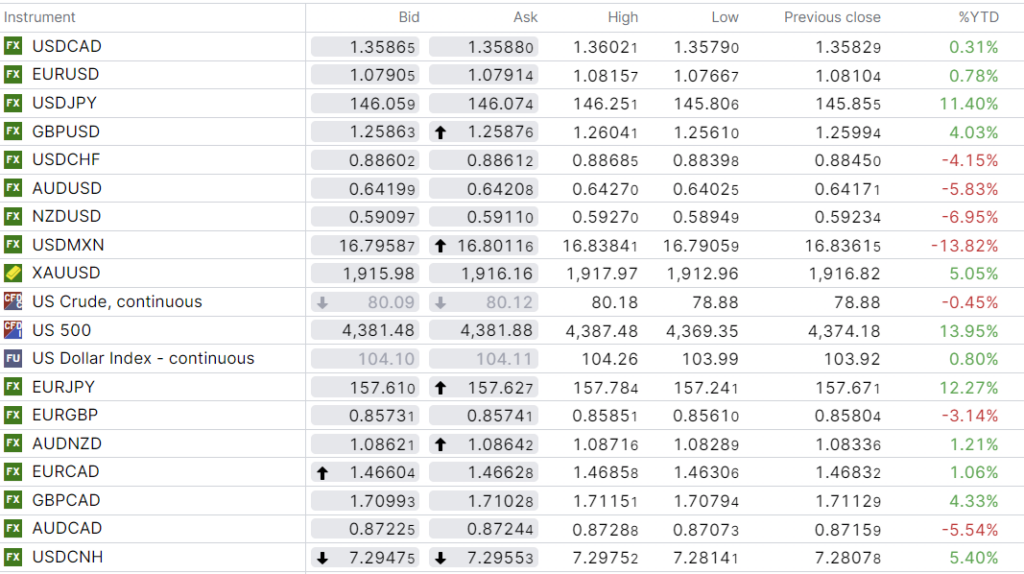

FX high, low, close

Source: Saxo Bank

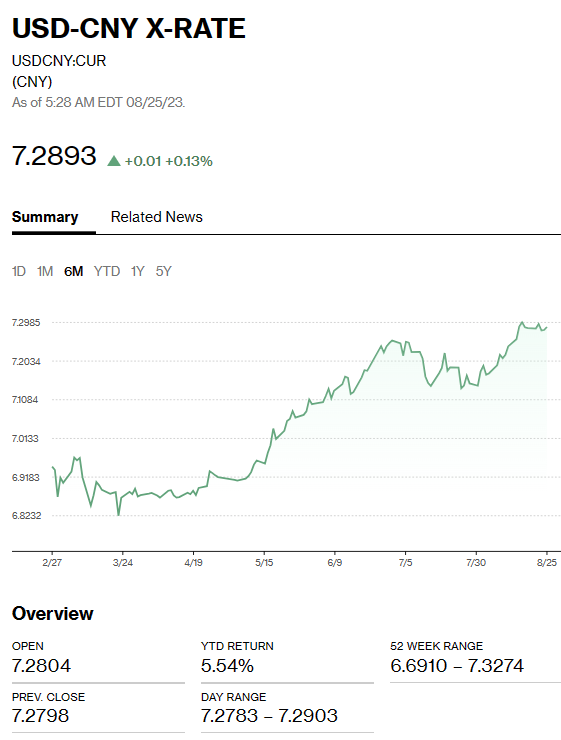

China Snapshot

Bank of China Fix: today 7.1883, expected 7.2923, previous 7.1886.

Shanghai Shenzhen CSI 300 fell 0.38% to 3709.15.

Chart: USDCNY 1 month

Source: Bloomberg