Source: Adobe stock

- Contagion risks from UK financial market turmoil fades

- Negative risk sentiment knocks Wall Street futures lower, again

- US retreats from yesterday’s open, but surges compared to Wednesday close.

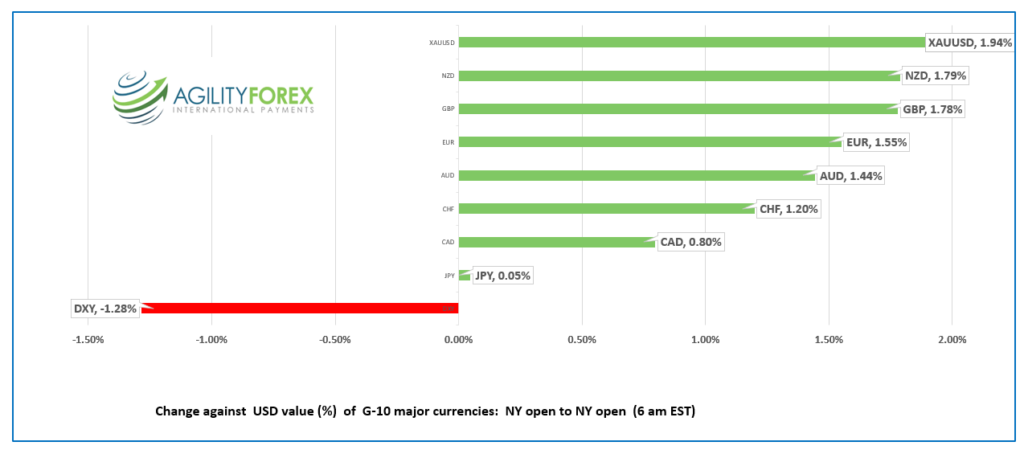

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3693-97, overnight range 1.3608-1.3754, close 1.3604

USDCAD rallied steadily from the NY close due to the bounce in the US 10-year yield which sparked broad-based US dollar demand and knocked S&P 500 futures lower. Prices are also underpinned by hawkish Fed rhetoric and expectations that BoC interest rate hikes will lag those of the Fed.

WTI oil prices rose from $76.60/barrel yesterday to $82.79 in NY today with the gains derived from talk that Opec will announce a 1 million barrel/day production cut beginning November 1 at the October 5 meeting.

Canada July GDP rose 0.1% m/m, a tad better than the 0.1% predicted. USDCAD traders ignored the results which were overshadowed by US data.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.3620, looking for a break above 1.3690 to extend gains to 1.3750 then 1.3810. A decisive break below 1.3580 would negate the September rally and extend losses to 1.3460.

For today, USDCAD support is at 1.3630 and 1.3610. Resistance is at 1.3690 and 1.3750. Today’s range: 1.3640-1.3740

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are a little bit calmer following yesterday’s UK-triggered chaos. But just a little. The reality of month and quarter-end portfolio rebalancing flows is clashing with the illusion of central bankers in control.

Asia equity markets closed with gains except for the Hong Kong Hang Seng Index. European bourses opened in positive territory but then dropped led by a 1.42% fall in the German Dax. S&P 500 and DJIA futures are down around 0.90%, but above their overnight session lows.

The US 10-year Treasury yield climbed to 3.80% from an overnight low of 3.733%

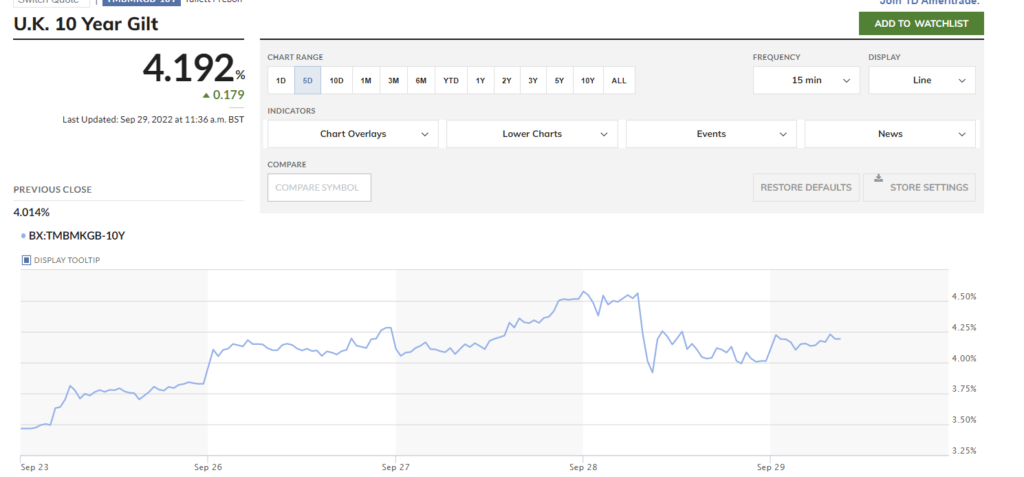

The warm and fuzzy feelings following the Bank of England’s bond market intervention yesterday are fading rapidly. The 10-year Gilt yield climbed to 4.192% compared to yesterday’s close of 4.014%, before easing back. Former BoE Governor Mark Carney said the Truss government budget plans of undercutting the Bank of England.

GBPUSD traded erratically and is just below the top of its 1.0764-1.0896 range in NY. The currency is tracking the 10-year Gilt yield is now 4.14% in NY. GBPUSD is not out of the woods and sentiment is bearish below the 1.0990 area.

EURUSD is in the middle of its overnight 0.9637-0.9737 range. Prices are supported by higher-than-expected German inflation data which rose 10.0% in September compared to the forecast for a 9.4% rise. EU economic sentiment deteriorated to 93.7 from 97.3. The EURUSD technicals are negative below 0.9780.

USDJPY was steady in a 144.10-144.80 band. Concerns about BoJ intervention limited gains while rising US Treasury yields contained losses.

AUDUSD traded in a 0.6437-0.6524 band and traders ignored August CPI data. (actual 6.8% y/y compared to 7.0% in July.

The US dollar caught a bit of a bid after weekly jobless claims were lower than expected (actual 193,000 vs forecast 215,000) and Personal consumption Expenditure data was higher than anticipated.

Chart: 5-day UK 10-year Gilt yield

Source: MarketWatch

The thirty-minute, one week, US dollar index chart clearly reflects the FX volatility and indecision in markets

Chart of the Day: US dollar index, 30 minute-one week

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

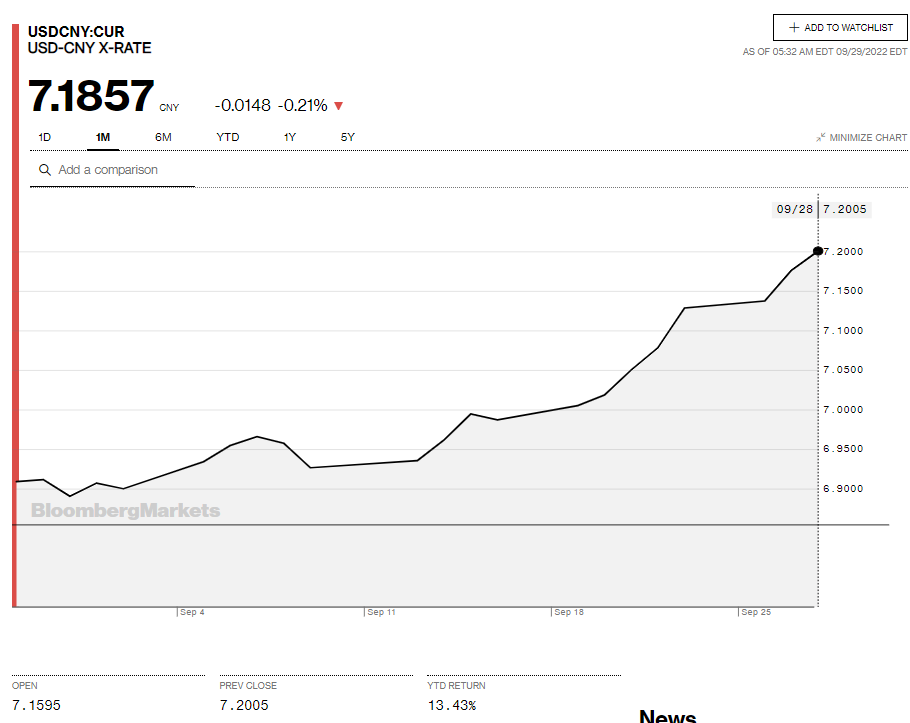

China Snapshot

Today’s Bank of China Fix: 7.1102, previous 7.1107

Shanghai Shenzhen CSI 300 fell 0.04% to 3,827.14

PboC promises to increase efforts to consolidate the economic recovery and expects CNY to remain stable for rest of 2022

Chart: USDCNY 1 month

Source: Bloomberg