Photo: Freesvg.org

April 21, 2023

- Lower commodity prices and oil sink Loonie.

- Traders confused by mixed quarterly earnings reports and Fed-speak.

- US opens higher vs commodity currency bloc while JPY outperforms.

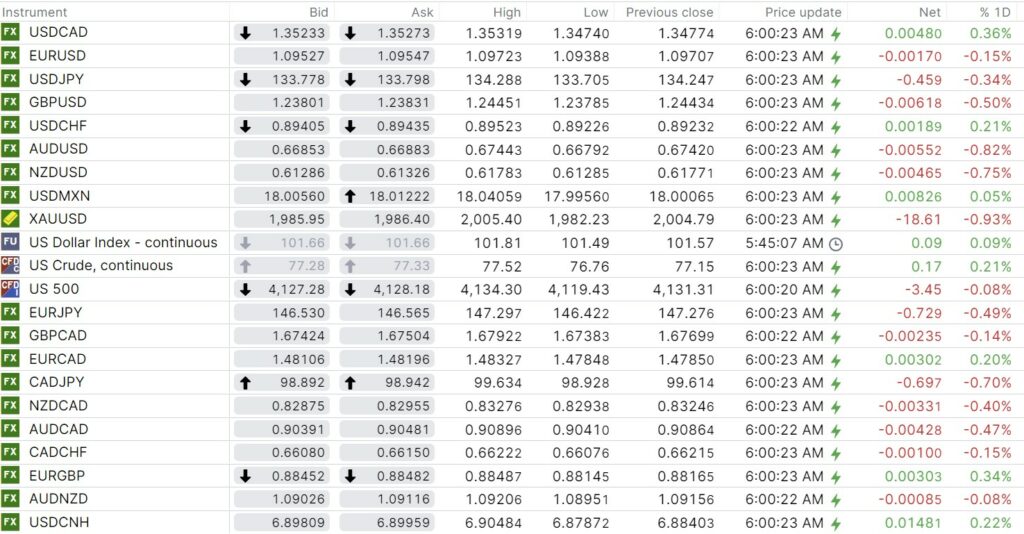

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3523-27, overnight range 1.3474-1.3536, close 1.3477

USDCAD is back to where it was on Easter weekend. It has recouped all the losses that occurred in the wake of the lower than expected US inflation report on April 12 and the FOMC minutes that gave rise to speculation the Fed would soon stop hiking interest rates.

The USDCAD rally is due to the drop in commodity prices, specifically oil. WTI prices are filling the gap between the March 31 closing price of $74.37/b and the post-Opec production cut announcement peak of $$83.40/b. Prices touched $76.76/b overnight and there is still a little room to fall further.

Chart: WTI oil-hourly, highlighting price gap.

Source: Saxo Bank

Oil wasn’t the only commodity falling. Gold prices dropped from $2005.40 to $1982.33. Perhaps it was in anticipation of a one off trade worth $22.0 million, which is the value of gold stolen from Air Canada at Toronto’s Pearson Airport. It should not surprise anyone, as Air Canada is number one at losing luggage.

Sooner or later, traders are going to look at the dog’s breakfast that Canada’s finances have become and realize that the economy cannot support growing debt from unrestrained government spending. Finance Minister Chrystia Freeland announced $43 billion of new spending when she tabled the 2023 budget, just three weeks ago.

Yesterday, the Trudeau government went back to the magic-money tree and plucked off $13 billion in the form of subsidies to give to Volkswagen AG to build a battery plant in Canada. There is another $700 million in cash as a “thank-you” for letting Canada be exploited by a German company worth $68 billion.

The gift beggars the question: “if Canada has so much money lying around, doesn’t it make sense to invest in modernizing the electric grid first, before flooding the country with electric cars?”

Canada Retail Sales were a tad better than expected, falling just 0.2% m/m rather than the 0.6% forecast. However, the ex-auto’s component was much worse, falling 0.7% compared to a gain of 0.9% in February. The news was ignored by traders.

USDCAD Technical Outlook

The intraday technicals are bullish with prices hovering around the 100-day moving average at 1.3426. The uptrend which began last Friday is intact while prices are above 1.3440, a level guarded by previous resistance and now support at 1.3490.

Fibonacci retracement analysis of the April 13-March 13 range suggests that the break above 1.3513 (38.2% retracement) will extend gains to 1.3643 (61.8% retracement level).

For today, USDCAD support is at 1.3490 and 1.3450. Resistance is at 1.3550 and 1.3580.

Today’s range 1.3480-1.3560

Chart: USDCAD daily with Fibonacci Retracement levels

Source: Saxo Bank

G-10 FX recap and outlook

It is the middle of spring and that’s when a young man’s fantasy used to turn to love. Not today.

The rising risk of a US recession is getting all the attention. At least that’s the spin being used to explain market action today after economic data showed the US economy was slowing and voting members of the FOMC seemed united in their views that the Fed needs to raise interest rates further. None of them mentioned reducing rates this year.

China’s Foreign Minister Qin Gang laid claim to the entire Taiwan Strait, and sounded like a fortune cookie when he said, “Those who play with fire on Taiwan will eventually get themselves burned.”

China may be the country getting burned. President Biden is planning to sign an executive order to greatly limit Chinese investment in American companies.

Asian equity indexes closed with losses, while European bourses are flat to slightly lower. S&P 500 futures are down 0.19% and the US 10-year Treasury yield inched down to 3.519% from 3.545%.

EURUSD traded steadily in a 1.0939-1.0990 range. Prices churned after the S&P Global-Hamburg Commercial Bank flash German PMI (HBOC) data was released.

The German economy showed signs of improvement even though business expectations for the year ahead, dipped.

ECB policy maker Luis de Guindos said the ECB will not provide forward guidance at the next meeting. He said “I believe that the current approach will be maintained for a few months until the evolution of inflation and the effects of our measures become clearer.

GBPUSD traded in a 1.2379-1.2445 band with weaker than expected UK Retail Sales data weighing on prices. Retail Sales fell 0.9% m/m in March (forecast -0.5%) while the ex-fuel component dropped to -1.0% (forecast -0.7% m/m)

Consumer confidence and PMI data were better than forecast and offset the negative retail report. However the Manufacturing PMI data was soft.

USDJPY dropped from 134.29 to 133.61 in tandem with falling US Treasury yields. Manufacturing PMI rose to 49.5 from 49.2 but is still in contraction territory.

AUDUSD traded negatively in a 0.6679-0.6744 range due to lower commodity prices, particularly iron ore which lost over 5.0%.

Today’s US economic calendar only has second tier data.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

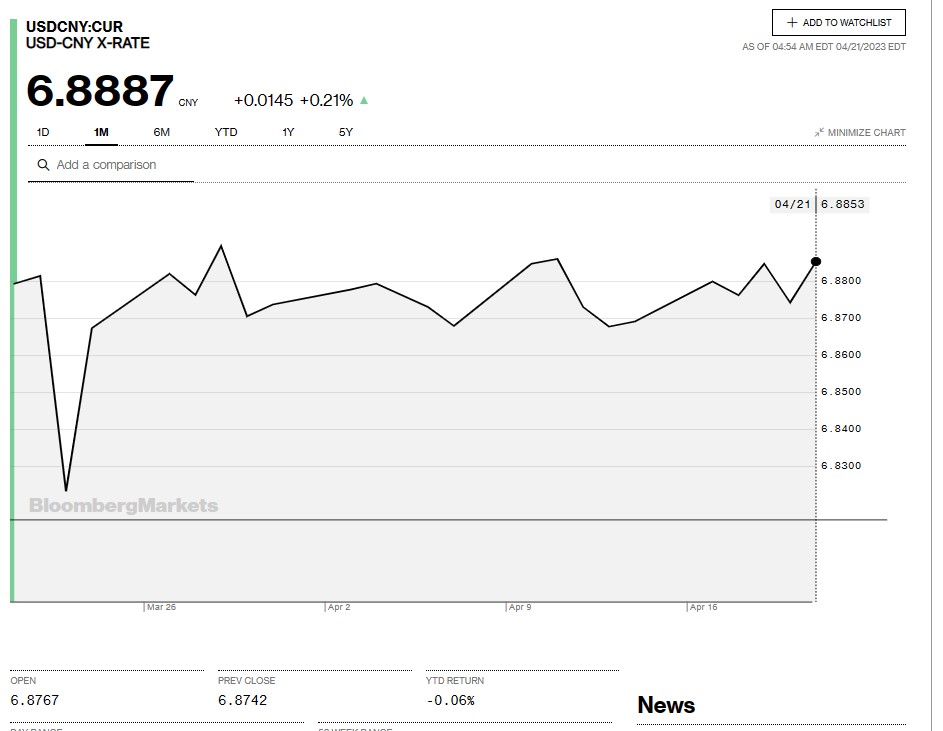

China Snapshot

Bank of China Fix: 6.8752, Previous: 6.8987

Shanghai Shenzhen CSI 300 fell 1.96% to 4032.57.

Chart: USDCNY 1 month

Source: Bloomberg