December 9, 2019

USDCAD open 1.3255-59 (6:00 am EST) Overnight range 1.3250-1.3263

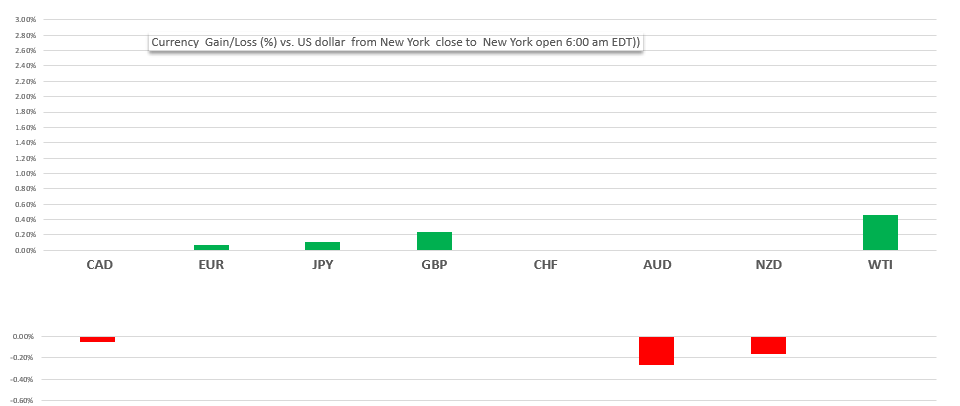

The impact on the US dollar from Friday’s forecast-smashing US jobs report (actual NFP 266,000 vs forecast 180,000) is already fading. The US dollar is trading mildly softer against EUR, GBP, and JPY. The impact of the butt-ugly Canadian Labour report has not. Canada lost 71,200 jobs and the unemployment rated jumped to 5.9% from 5.5%. USDCAD held on to Friday’s gains.

Weaker than expected China trade data, especially the 1.1% y/y drop in Exports pressured the commodity currency block against the US dollar and they opened with small losses.

FX Market Snapshot

Change in currency value against the US dollar from NY close to NY open

Source: Saxo Bank/IFXA

FX markets continue to await concrete news on the state of the US/China trade negotiations, ahead of the next US tariff hikes on December 15. China is still irate at the Americans for passing what they see as “anti-China bills” to interfere in domestic affairs. On Saturday, National Economic Advisor Larry Kudlow said that a deal was close, but President Trump was not ready to sign. He also said he didn’t know of any travel plans for US negotiators, suggesting a deal may be unlikely this week.

However, it was the weak trade data which

GBPUSD was the best performing G1-0 major currency again, rising from 1.3129 to 1.3180, driven by election polls pointing to a solid Conservative majority after Thursday’s election results. Analysts point out that “strategic voting” can make a mockery of the polls, leaving GBPUSD vulnerable to a sell-off.

EURUSD drifted higher overnight, getting a bit of support from German trade data which, although soft, was not as bad as expected. The intraday technicals are bullish while prices are above 1.1050, looking for a break above 1.1110 to extend gains to 1.1170.

USDJPY slid steadily overnight, falling from 108.65 to 108.45 in New York trading. The weak China trade data, and a wisp of risk aversion sentiment ahead of the tariff deadline on December 15. A drop in 10-year US Treasury yields from Friday’s close of 1.843% to 1.822%, also weighed on prices.

AUDUSD and NZDUSD suffered from China’s trade woes, trade data, and lingering US dollar demand from the nonfarm payroll report.

Oil prices are off their overnight peak. West Texas Intermediate (WTI) topped out at $59.14/barrel and is trading in New York at $58.57/b. Opec and Russia agreed to an additional 500,000 barrels/day production cut. Saudi Arabia stepping up for even steeper cuts, adding 400,000 b/day, on top what was agreed. All in all, the new cuts total 2.1 million/barrels per day since they were first implemented.

USDCAD continues to be supported by Friday’s weak employment report which some analysts saw as giving the Bank of Canada a green-light to cut interest rates in January. Other’s see the results as “noise’ and distorted due to the election.

The only data available today is Canadian Housing Starts, which are not usually a USDCAD driver.

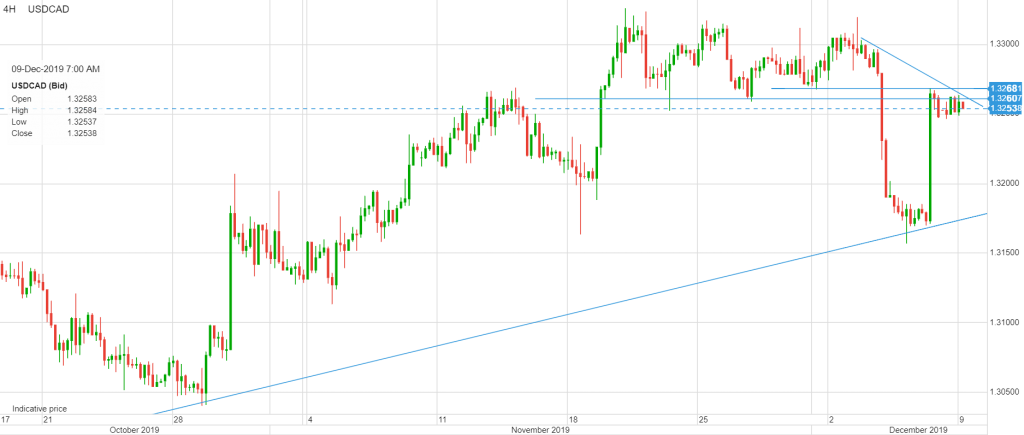

USDCAD Technical View

The USDCAD technicals are bullish will prices are above 1.3160, looking for a break of resistance at 1.3280 to extend gains to 1.3350. A break above 1.3350 targets 1.3440. A break below 1.3170 shifts the focus to 1.3050. For today, support is at 1.3230 and 1.3180. resistance is at 1.3280 and 1.3310. Today’s Range 1.3230-1.3280

Chart: USDCAD 4 hour

Source: Saxo Bank