January 30, 2024

- US Quarterly earnings reports overshadows geopolitics.

- Euro area data is sluggish.

- US dollar drifting lower on improved risk sentiment.

FX at a glance

USDCAD Snapshot: open 1.3401-05, overnight range 1.3399-1.3438, close 1.3415.

USDCAD started the NY session by trading defensively but that changed after support in the 1.3400 area held. Traders are adjusting positions ahead of tomorrow’s FOMC meeting. The Fed is expected to have adopted a dovish bias, but traders fear they will also push back against expectations for early rate cuts. Even so, the dovish bias has helped power the Dow Jones Industrial Average and the S&P 500 indexes to another record close.

Canada and US 2-year spreads have narrowed in Canada’s favor, which has exacerbated USDCAD selling in anticipation that US interest rates may fall faster and by a wider margin than Canadian rates.

WTI oil prices are steady in a $76.44-77.31/barrel range in part because there are ample crude supplies and Chinese demand has weakened in the past few months. However, an aggressive US response to punish Iran for its involvement in the attack on the US base could give prices a boost.

USDCAD Technicals:

The intraday USDCAD technicals are bearish while trading below 1.3440 which guards the longer term downtrend level at 1.3530 and is looking for a break below 1.3380 to extend losses to 1.3350. A move above 1.3440 shifts the focus to 1.3530.

Bollinger Band studies suggest that USDCAD is becoming oversold in the 1.3350-1.3390 area which would suggest an upside correction from the lower level.

For today, USDCAD support is at 1.3380 and 1.3350. Resistance is at 1.3440 and 1.3490. Today’s range is 1.3380-1.3480.

Chart: USDCAD 4 hour

Source: Daily FX

G-10 FX recap

Iran is hoping that President Joe Biden doesn’t cave in to Republican pressure and retaliate against Iran because one of its puppet militias, using drones, attacked a US base in Jordan and killed three servicemen. Iran may be on edge, but global markets are not overly concerned. They are focused on upcoming quarterly earnings reports from Alphabet and Microsoft today and Amazon, Meta, and Apple due Thursday.

Asian equity indexes followed Wall Street’s lead and closed with gains, except for Chinese indexes. Japan’s Nikkei 225 index gained 0.11% while Australia’s ASX rose 0.29%. European stock traders ignored weak data and are trading higher, led by a 0.56% rise in the UK FTSE 100 index. SP500 futures are down 0.14%. Gold prices are close to unchanged and are struggling to gain any upside traction from the Middle East hostilities. The US 10-year Treasury yield has ticked down to 4.062%.

Traders will pay attention to today’s JOLTS job openings data. They expect openings to have ticked lower to 8.75 million in December, which will provide more evidence that the labor market is normalizing.

EURUSD bounced from its session low of 1.081 to 1.0850 in NY, despite a barrage of weak Eurozone economic reports. The Eurozone narrowly avoided a recession when Q4 GDP came in flat . Eurozone Consumer Confidence, Services Sentiment and Business Climate data was mixed which left the EURUSD downtrend below 1.0885 intact.

GBPUSD is just above the bottom of its 1.2662-1.2722 range even after BRC retail prices rose at the slowest annual pace since May 2022. Traders fear a that the Bank of England may pivot dovishly which is narrowing the UK/EUR and UK/US yield advantage. The GBPUSD remains in an uptrend above 1.2660.

USDJPY dropped to 147.16 then rebounded to 147.58 in NY with price action dictated by the outlook for BoJ rates and US Treasury yields.

AUDUSD is trading bearishly in a 0.6584-0.6625 range. The currency is suffering from ongoing China growth concerns and soft Australia’s December Retail Sales which fell 2.7% m/m (forecast -0.9%, November 1.6%)

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

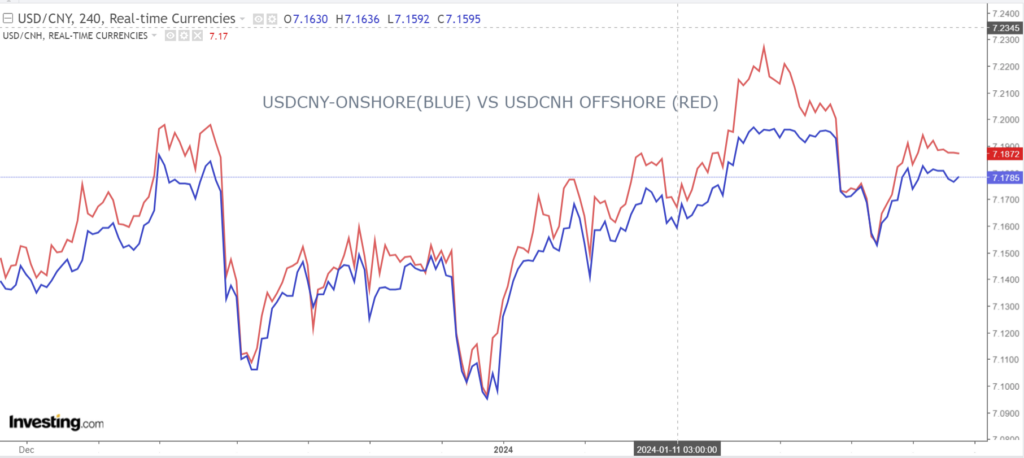

China Snapshot

PBoC fix: today 7.1763, expected 7.1763, previous 7.1097.

Shanghai Shenzhen CSI 300 fell 1.79% to 3245.04.

Chart: USDCNY and USDCNH 4 hour

Investors are not buying what Xi Jinping and his cronies are selling, and they took it out on the stock market. Last week’s action by authorities to get state-owned companies to buy stocks to shore up the CSI index failed as investors sold into the rally. The Evergrande Group liquidation order underscored the ongoing property sector issues. In addition, investors were chased away by heavy-handed government regulations that interfered with the tech sector.

Source: Investing.com