February 7, 2024

- Bank of Canada Governor repeats dovish view.

- Fed officials say they are in no hurry to rates.

- US dollar gives back some gains-Kiwi outperforms.

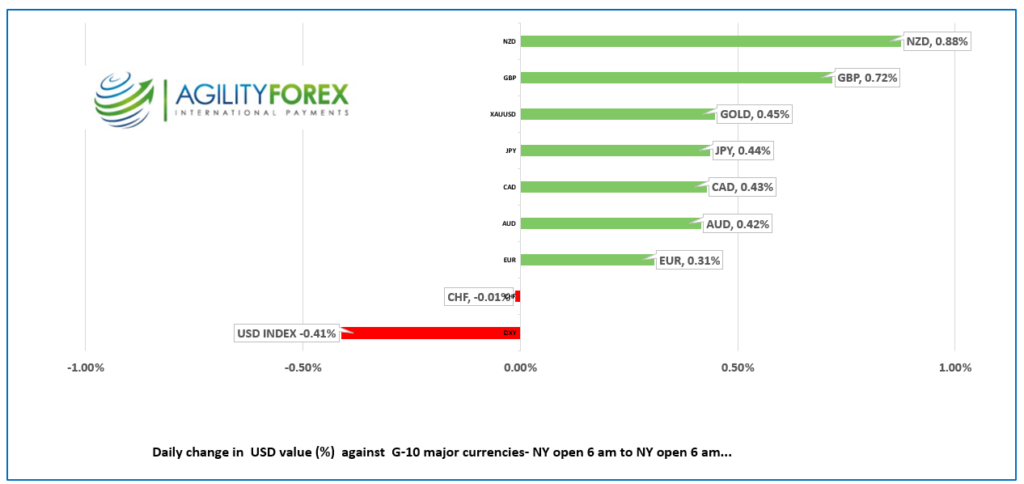

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3481-85, overnight range 1.3455-1.3496, close 1.3495.

USDCAD bounced off of resistance in the 1.3540 area yesterday and snapped the intraday uptrend in the process. Sentiment flipped from bullish to bearish yesterday after the US 10-year Treasury yield slid from its 4.155% peak yesterday to close at 4.09%. Those yields climbed back to 4.132% in early NY but dropped again. That prices action is continuing to weigh on USDCAD and is driving prices to the 1.3440-60 support zone.

The move followed on the heels of US 10-year Treasury yields sliding down to 4.09% from 4.15% yesterday.

BoC Governor Tiff Macklem aggressively defended his incompetence in managing monetary policy although he framed it as a hugely successful endeavor. He said the bank’s forceful tightening of monetary policy (raising rates 10 times in 17 months) slowed demand, rebalanced the economy, and is bringing down inflation. He didn’t mention that he extolled Canadians to strap on debt or say anything about how massive government spending exacerbated the problem.

He acknowledged the domestic housing issue saying, “Housing affordability is a significant problem in Canada—but not one that can be fixed by raising or lowering interest rates.” But it’s not the Bank’s fault—it’s government policies at all levels. He wrapped up his speech by repeating, “Governing Council’s discussion about future policy is shifting from whether monetary policy is restrictive enough to how long to maintain the current restrictive stance.”

Traders ignored the speech and are awaiting a catalyst to break USDCAD out of its 1.3350-1.3550 range.

USDCAD Technicals

The intraday USDCAD technicals flipped to bearish with the break below 1.3510 (which has reverted to resistance) and are now looking to test support in the 1.3440-50 area. A move above 1.3510 suggests another test of 1.3550.

The February range of 1.3350-1.3550 will contain price action until there is a new catalyst.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3510 and 1.3550. Today’s range is 1.3440-1.3520

Chart: USDCAD 4 hour

Source: Daily FX

G-10 FX recap

A gaggle of Fed officials agreed that US rates would be heading lower but cautioned that rate cuts would be gradual. Central bankers around the world have been regurgitating similar sentiments but it wasn’t until Treasury yields retreated that the US dollar gave back some gains.

The U.S. monthly international trade deficit increased in December 2023 according to the U.S. Bureau of Economic Analysis and the U.S. Census Bureau. The deficit increased from $61.9 billion in November (revised) to $62.2 billion in December, as imports increased more than exports. Traders ignored the data.

Fed officials Michelle Bowman, Thomas Barkin, and Adrian Kugler are speaking today and with luck their make stoke some activity.

European bourses are in the red, led by a 0.30% decline in the German Dax. SP500 futures are unchanged, and the US 10-year yield has climbed to 4.13%. Prices were underpinned by comments from noted ECB hawk Isabel Schnabel. She pointed out that a tight labor market, sticky services inflation, and Red Sea issues suggested that a very cautious approach is necessary before adjusting policy.

EURUSD prices firmed in a 1.0751-1.0784 range and is currently testing the downtrend line in the 1.0770-80 area. The gains are due to broad US dollar weakness but he rally may run out of steam as there is no actionable data today.

GBPUSD is in the middle of its 1.2593-1.2641 range with a bit of support arsing after UK house prices were strong than expected.

USDJPY ebbs and flows depending upon the prevailing outlook for US and Japanese monetary policy. Prices drifted in a 147.72-148.29 range overnight. Activity may be muted as the major Asian centers get ready for the Lunar New Year holidays.

AUDUSD climbed in a 0.6517-0.6541 range overnight thanks to lingering support following the Reserve Bank of Australia leaving rate hikes on the table at Monday’s meeting.

NZDUSD traded in a 0.6092-0.6115 range with prices getting a boost from a stronger than expected employment report. NZ’s unemployment rate (actual 4.0 vs forecast 4.2%) and Labour Cost Index (actual 1.0% q/q vs forecast 0.8%) suggesting that if rate cuts were planned, they would be deferred.

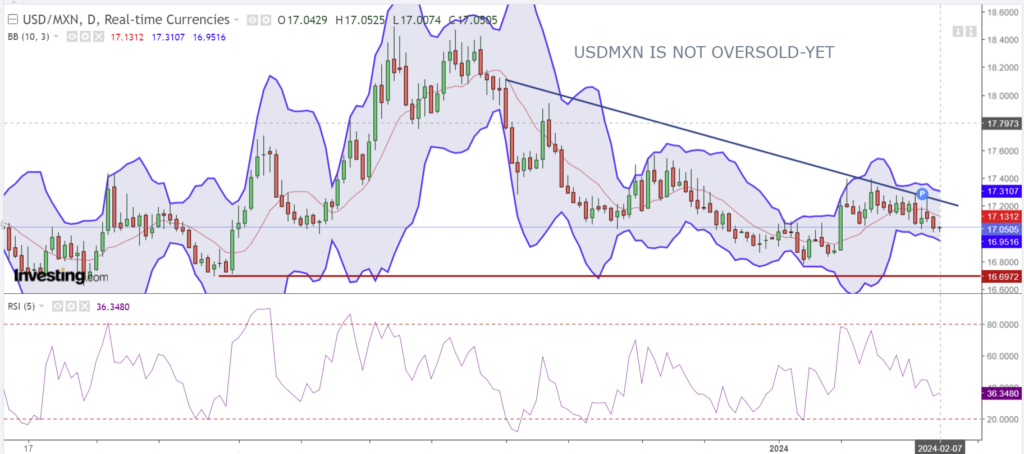

USDMXN traded defensively since peaking at 17.2809 on Monday and it traded sideways in a 17.0074-17.0594 range overnight. Banxico monetary policy meeting is tomorrow, and they are expected to leave rates unchanged at 11.25%. USDMXN is in a downtrend below 17.2600 with a move below 16.9320 targeting 16.7140, the bottom of the range that has held since the end of August.

Chart: USDMXN daily

Source: Investing.com

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1049, expected 7.1858, previous 7.1082.

Shanghai Shenzhen CSI 300 rose 0.96% to 3343.63.

Is the CSI 300 rally real or Memorex? (if you don’t know, google it). Analysts are suggesting that the State-orchestrated rally is to put investors in a good mood as they head into the Lunar New Year holidays.

Xi Jinping fired Yi Huiman as the chief of the Securities Regulatory commission because he failed to halt the stock market sell-off that erased $7 trillion in value since 2021. Jinping is conveniently forgetting his role in the debacle. He ordered the arrest of key business leaders, he bungled the covid response and he promoted aggressive real estate policies.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com