Photo: HDclipartall.com

February 10, 2023

- Canada adds 149,900 jobs.

- Russia plans oil production cut in March.

- US dollar opens with gains compared to Thursday-mixed bag overnight.

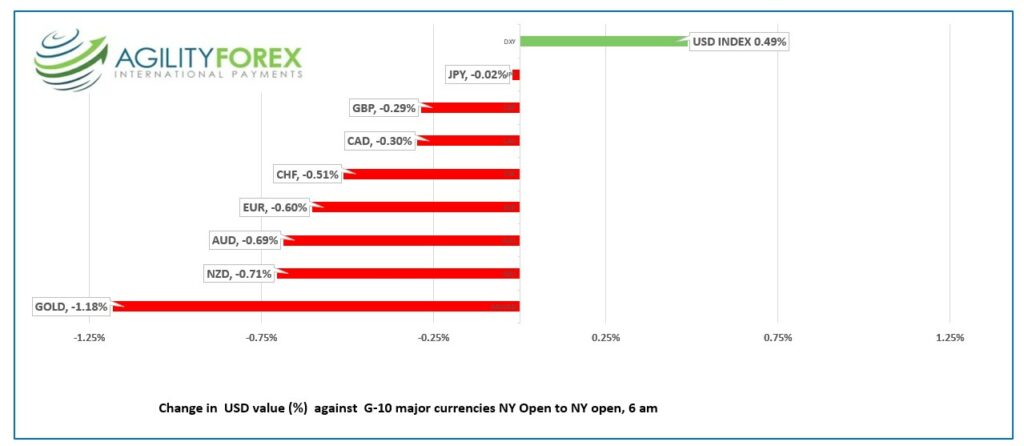

FX at a glance

Source: IFXA Ltd/RP

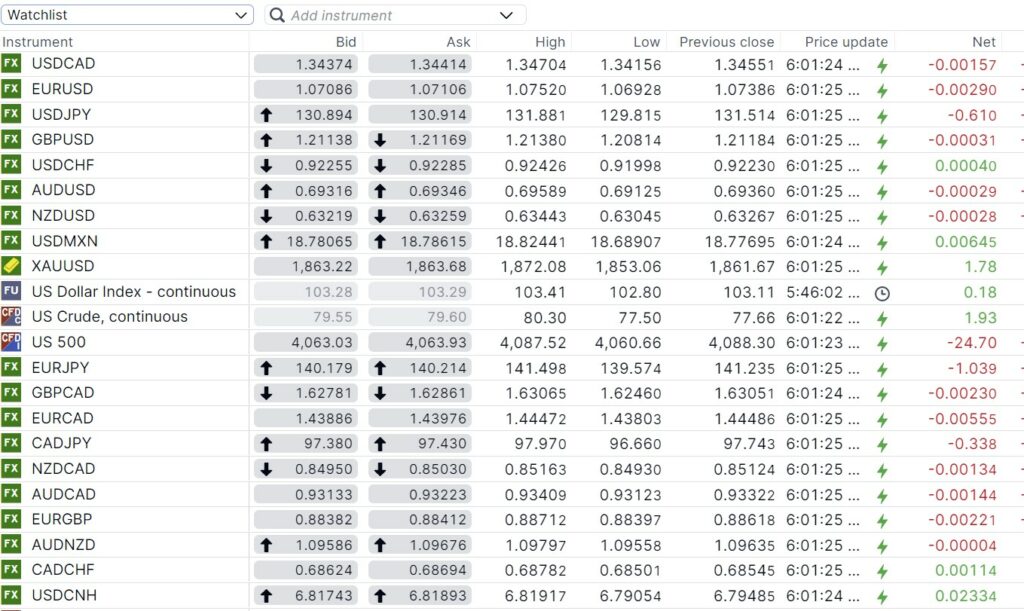

USDCAD Snapshot: open 1.3437-41, overnight range 1.3364-1.3470, close 1.3455

USDCAD traded in a 1.3416-1.3470 range overnight, pushed through the bottom before the employment data was released, then dropped to 1.3368 in the aftermath.

Canada added 149,900 jobs in January, a stellar performance considering it follows on the heels of a 104,000 increase in December. 114,700 of those jobs were full-time. Canada has gained 326,000 jobs since September. The unemployment rate remained unchanged at 5.0%.

It is a very strong report, and it could force the Bank of Canada to re-think their interest rate strategy. Perhaps they paused too early.

USDCAD resistance in the 1.3470 area is being reinforced by higher oil prices. WTI climbed to $80.30/b from $77.50/b overnight due to a report that Russia is cutting production by 500,000 barrels /day starting in March. Russian Deputy Prime Minister Alexander Novak blamed Western sanctions for the move.

USDCAD direction continues to be dictated by S&P 500 index moves.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3360 and looking for a break above 1.3480 to extend gains to 1.3700. It won’t be a straight shot higher due to resistance from the 100-day moving average at 1.3530. A break below 1.3360 will lead to a test of the June uptrend line at 1.3300 which guards the major support in the 1.3220 area.

For today, USDCAD support is at 1.3360 and 1.3340. Resistance is at 1.3470 and 1.3530

Today’s range 1.3360-1.3460.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are pessimistic and risk averse. The modest increase in US weekly jobless claims on the heels of a robust nonfarm payrolls report led to the 10-year Treasury yield grinding higher to 3.713% from 3.615% yesterday.

A report from Kyiv claiming Russian missiles crossed Romanian airspace raised concerns of rising NATO/Russia tensions, and another reason to buy US dollars.

Traders are awaiting the next major piece of the US interest rate puzzle, January inflation. Core-CPI is expected to drop to 5.3% y/y from 5.7% y/y. The methodology used to calculate the data has been tweaked, leaving lots of room for interpretation.

EURUSD is trading at the bottom of its 1.0693-1.0752 range due to broad dollar strength, fears of higher oil prices and rising geopolitical tensions due to errant Russian missiles flying in NATO airspace. Traders are looking ahead to next week’s US inflation report while turning a deaf ear to hawkish comments from ECB policymakers.

GBPUSD churned in a 1.2081-1.2138 range, and it is trading in NY slightly lower than where it yesterday. All the volatility occurred in the European session following the release of a slew of economic data which included Industrial Production, Manufacturing Production, Trade and GDP. The UK economy avoided a technical recession. Q4 GDP was 0%, q/q which was as forecast.

USDJPY traded wildly in a 129.81-131.88 band overnight, but when it was all said and done, the currency pair opened in NY, nearly unchanged from Thursday. The volatility occurred when the Japanese government surprised traders by announcing the nomination of 71-year-old Kazuo Ueda to be the next governor of the Bank of Japan. Previously the government had hinted that current Deputy Governor Masayoshi Amamiya would get the job.

AUDUSD was whippy in a 0.69313-0.6959 range but despite all the travel time, it opened in NY right where it closed yesterday. The RBA released its Statement of Monetary Policy which showed an upgraded “trim mean” CPI forecast to 4.3% from 3.8%.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Bank of China Fix: 6.7884, Previous: 6.7905

Shanghai Shenzhen CSI 300 fell 0.59% to 4106.31.

January CPI lower sharply lower than in December. (actual -0.8%, forecast 0.7%, December 0% m/m),

On an annual basis CPI rose 2.1% (forecast 2.2%, December 1.8% y/y)

Producer prices fell 0.8% (forecast -0.5%, Dec -0.7% y/y)

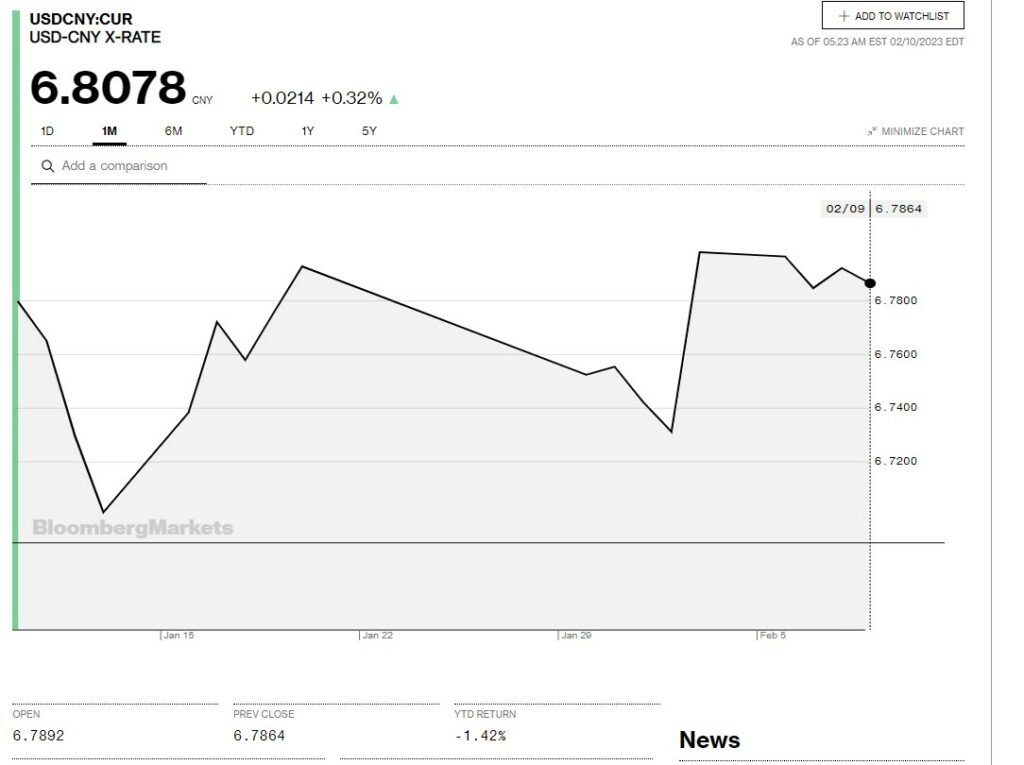

Chart: USDCNY 1 month

Source: Bloomberg