Picture: greenpeace.org

- Some markets closed for Remembrance Day/Veterans Day

- UK data mixed, GBPUSD under pressure

- US dollar adds to post-CPI gains, CAD biggest loser

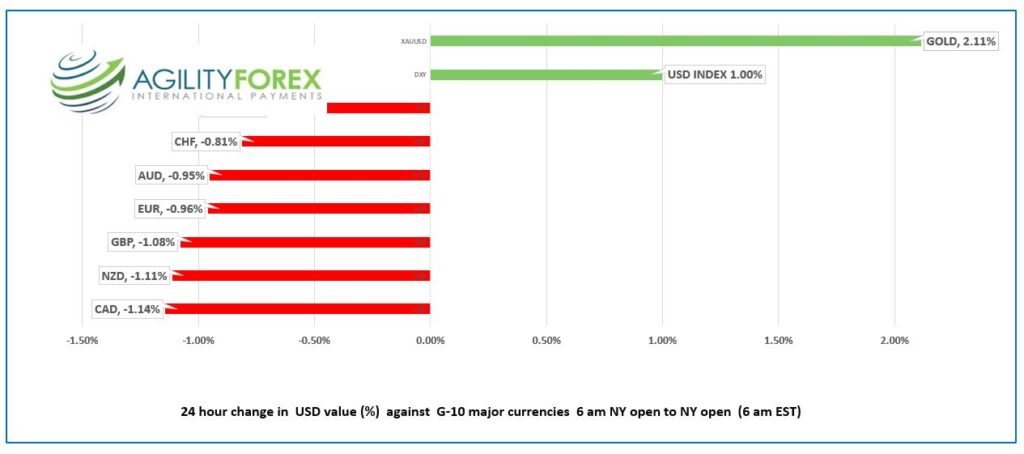

FX at a Glance:

Source: IFXA Ltd/RP

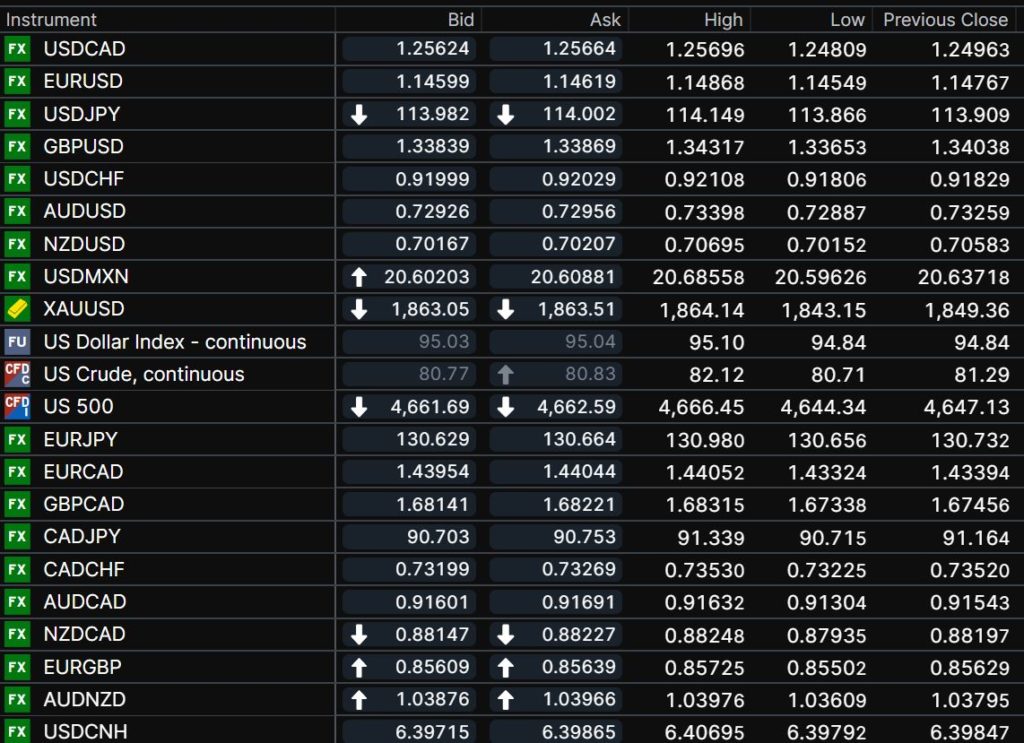

USDCAD Snapshot Open 1.2562-66, Overnight Range 1.2481-1.2583, Previous close 1.2496

USDCAD soared rising from 1.2386 around the 10:00 am ET option expiry window to 1.2583 in NY trading today. The rally was due to broad US dollar demand after the hotter than expected October US CPI data (actual 0.9% m/m vs forecast o.6% m/m) drove the US 10year Treasury yield from 1.422% to 1.57% today.

USDCAD saw additional support from falling crude oil prices, which dropped from $84.35/barrel to $80.89/b today.

It is Remembrance Day in Canada and Veterans Day in the US, and there are no economic reports as government offices are closed.

USDCAD upside may be limited if WTI oil prices remain steady, and if upcoming domestic data suggests Canadian rates will rise sooner than expected.

Technical view: The intraday USDCAD technicals bullish after supposedly strong resistance crumbled like Feta cheese. Prices easily took out the 200-day moving average at 1.2473 and the 100-day moving average at 1.2537, suggesting further upside ahead. Those levels will revert to support as USDCAD targets the 50% Fibonacci retracement level of the September 20-October 27 range (1.2590) and the 61.8% level at 1.2665.

For today, USDCAD support is at 1.2530 and 1.2470. Resistance is 1.2590 and 1.2660. Today’s range 1.2510-1.2590

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The robust US inflation report drove Treasury yields higher, and traders are pricing a 67.3% chance of a Fed rate hike in June, and a 76.4% chance in July, according to the CME Fedwatch tool.

The US dollar soared against the G-10 majors, as did the traditional inflation hedge gold, which climbed to $1,865.09 today. A week ago, XAUUSD traded at $1,761.00.

The major Asian equity indexes posted gains. The Nikkei 225 got a lift from the weaker yen, and Chinese markets rose after Evergrande made interest payments. Australia’s ASX 200 fell due to a weak employment report.

Most European traders are smiling. The DAX, CAC and FTSE 100 are flat to higher. Wall Street closed with losses, but S&P 500 and DJIA futures rebounded overnight.

EURUSD traders ignored the latest European Commission report, which upgraded GDP growth for 2021 to 5.0% ( 4.3% in May) but downgraded the forecast for 2022 to 4.3% from 4.8%. The dovish ECB monetary policy outlook contrast with US expectations which is weighing on prices. EURUSD blew through support at 1.1500 yesterday with a move below 1.1450, opening the door to 1.1210.

GBPUSD dropped from 1.3432 to 1.3365 overnight, suffering from broad US dollar strength, slower than expected GDP growth, and self-inflicted Brexit wounds. GDP grew 1.3% in the three months to September which missed the forecast for 1.5% growth and remained below the pre-pandemic level of 2.1%. A move below 1.3360 targets 1.3280.

USDJPY is consolidating recent gains in a 113.75-114.50 range. The rise in US Treasury yields fueled the move

AUDUSD fell from 0.7340 to 0.7289 due to both board US dollar strength and a weaker than expected employment report. Employment fell 46,300 compared to expectations for a 50,000 increase. Prices have ticked back to 0.7400 in NY. NZDUSD mirrored AUDUSD price action.

.Chart of the Day: US Dollar Index

Source: Investing.com

FX open, high, low, previous close

Chart: Saxo Bank

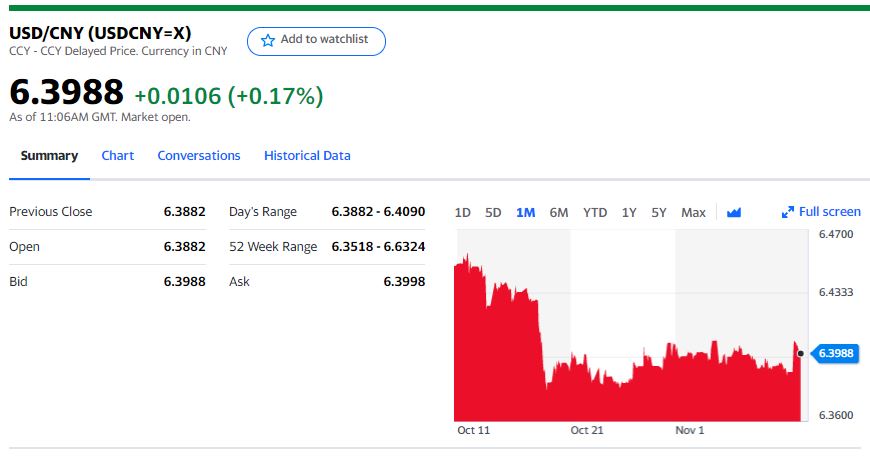

China Snapshot

Today’s Bank of China Fix 6.4145 Previous 6.3948

Shanghai Shenzhen CSI 300 ROSE 1.61% to 4,898.65

October CPI rose 1.5% y/y vs 0.7% in September, 0.7% m/m vs 0% in September

October PPI 13.5% y/y vs 10.7% in September

Evergrande paid overdue interest on three bonds

President Biden and President Jinping to have virtual meeting Monday

Chart: USDCNY 1 month

Source: Yahoo Finance