Photo: hdclipart.com

March 31, 2023

- Key US PCE inflation declines to 4.6% from 4.7%

- Risk sentiment improves following better than expected US and Chinese data,

- US dollar opens higher compared to the close but is down year-to-date.

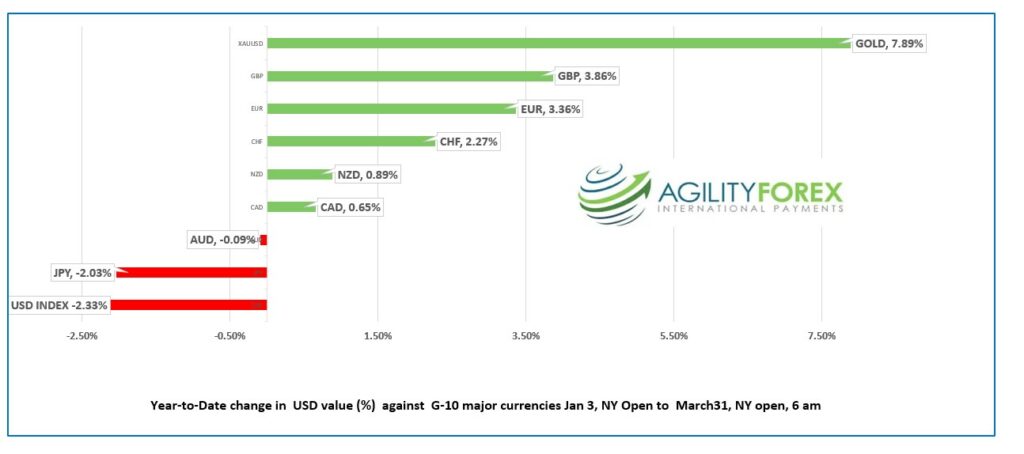

FX at a glance-Year-to-Date

Source: IFXA Ltd/RP

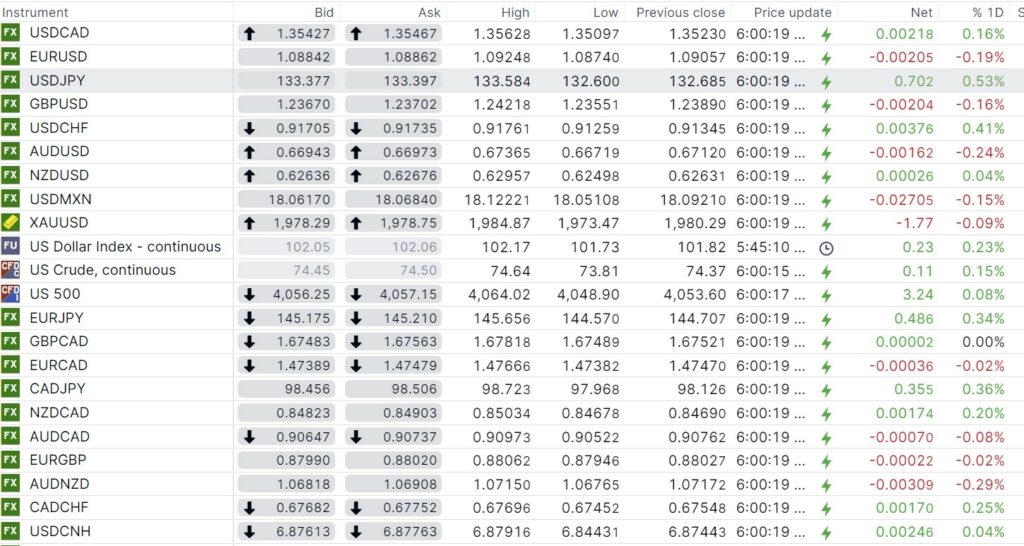

USDCAD Snapshot: open 1.3543-48, overnight range 1.3510-1.3563, close 1.3523

USDCAD bounced off of support and the 100-day moving average overnight with price action mirroring risk sentiment. China released better than expected Manufacturing and non-manufacturing PMI data which gave the commodity currency bloc a lift. Then profit taking and of today’s US PCE inflation report lifted USDCAD to the middle of its overnight band.

WTI oil prices have pushed above the 61.8% Fibonacci retracement level of the March range and is targeting the $76.85 area. Only a decisive break above the $78.50 area will negate the downtrend that has been in place since July and put $100.00/barrel on the menu.

The recent USDCAD weakness is partly driven by month and quarter-end portfolio rebalancing flows. The S&P 500 has gained 2.52% MTD and 5.93% YTD, implying US dollar selling. That implies USDCAD is a buy on dips around the 11:00 am fixing time.

Canada’s economy grew faster than even Stats Canada expected, rising 0.5% m/m in January (forecast 0.3%). Stats Canada is looking for 0.3% growth in February.

USDCAD Technical Outlook

The hourly technicals are bearish below 1.3570 and looking for a move below 1.3510 to test 1.3480. A move above 1.3580 targets 1.3660.

The daily USDCAD technicals are bearish while trading below 1.3690 with a break below the 1.3510-20 area suggesting further losses to 1.3450, looking for a break below 1.3510, which represents the 100-day moving averages as well as previous lows. A move below 1.3510 will extend losses to 1.3460.

For today, USDCAD support is at 1.3505 and 1.3480. Resistance is at 1.3590 and 1.3630.

Today’s range 1.3510-1. 3610

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Investors are happy to see the backside of March and the turmoil it brought.

The first quarter of 2023 is almost over and it wasn’t a good one for the greenback. The US dollar lost 3.86% against the Euro and 3.36% against sterling but gained 2.33% against the yen. The US dollar losses are mainly due to traders believing the Fed will not just pause rate hikes but cut them as soon as the summer.

Today’s Washington Post headline screams Trump Indicted. Trump supporters are not the most introverted of people and they may take exception to the Democrat Manhattan District Attorney Alvin Bragg’s attempt to derail Trump’s 2024 election plans.

The Fed’s favourite measure of inflation, PCE dropped to 5.0% y/y in February (January 5.3% y/y) while the more important Core-CPI reading dipped to 4.6% from 4.7% y/y. The monthly core-CPI ticked down to 0.3% from 0.5%.

The Fed will be happy to see the downward trek in inflation, but it is still well above the target. At the moment, analysts are suggesting the results reinforce arguments for a “soft-landing.

EURUSD is close to the bottom of its overnight 1.0874-1.0925 range due to a bit of profit-taking ahead of this morning’s US PCE and Michigan Consumer Sentiment reports. Eurozone inflation data was encouraging as it fell to 6.9% y/y in March compared to 8.5% in February. However, core inflation rose 1.2% m/m from 0.8% previously. The unemployment ticked down to 6.6% from 6.7%. The intraday EURUSD technicals are bearish below 1.0930, looking for a drop to 1.0750.

GBPUSD rallied to 1.2422 in Asia before dropping to 1.2355 in Europe as the price action mirrored that of EURUSD. Traders are dealing with contradictory economic reports. The Lloyds Bank Business Barometer rose from 21% to 32% in March, while Q4 GDP rose 0.1% q/q compared to the previous estimate of 0.0%, avoiding a technical recession. UK house prices fell the most since 2009, dropping 3.1% y/y in March.

USDJPY traded choppily but with a bullish bias in a 132.60-133.588 range. Japanese economic data was mostly higher than expected. Tokyo CPI rose 3.3% y/y (forecast 2.7%) Retail Trade surged 6.6% in February (previous 5.0% y/y), and Industrial production rose 4.5% m/m. However, the unemployment rated ticked up to 2.6% from 2.4%.

AUDUSD rose then sank in a 0.6672-0.6737 range in Asia and Europe, then recouped some losses in early NY trading. Better than expected Chinese Manufacturing and Non-Manufacturing PMI data supported prices while the RBA interest rate outlook limited gains. Noted RBA “watcher” James Glynn wrote an article saying the central bank will pause hiking interest rates at next Tuesday’s meeting but issue a hawkish statement.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

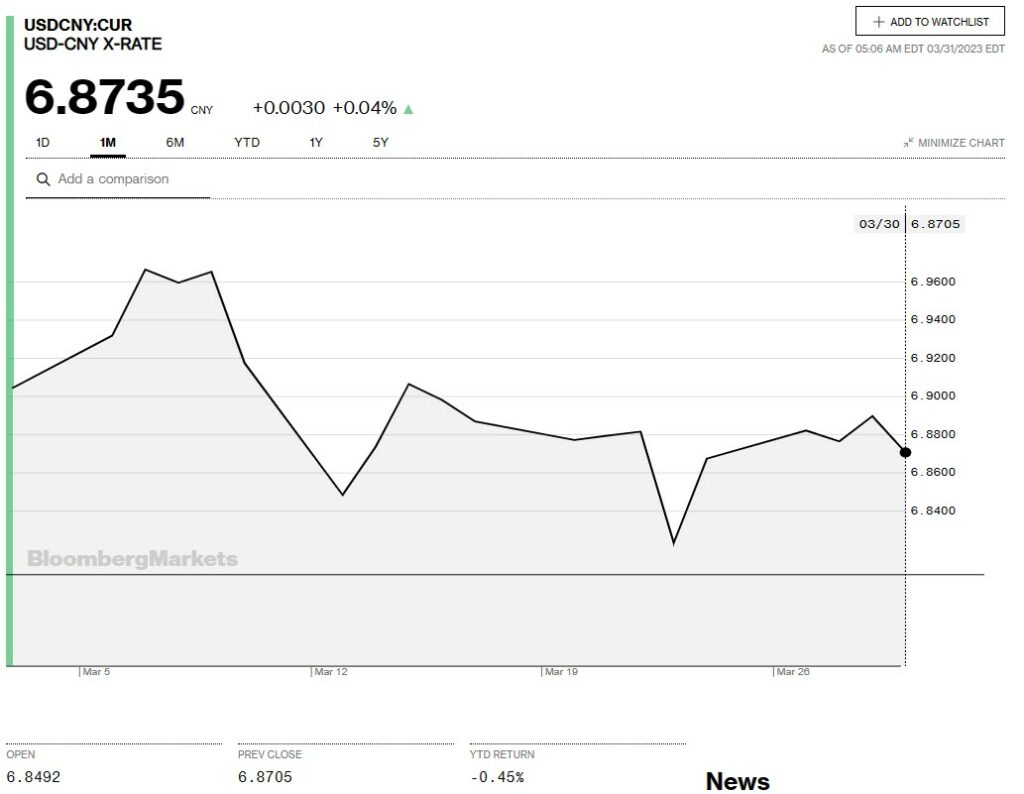

China Snapshot

Bank of China Fix: 6.8717, Previous: 6.8886

Shanghai Shenzhen CSI 300 rose 0.31% to 4050.93.

March NBS Manufacturing PMI 51.9 (forecast 51.5, previous 52.6)

March Non-Manufacturing PMI 58.2, February 56.3, highest since 2011.

Chinese Vice Finance Minister said the country needs to increase fiscal policy assistance as the economic recovery is “not yet solid.”

Chart: USDCNY 1 month

Source: Bloomberg