August 7, 2024

- Risk sentiment is mildly positive

- BoC Summary of Deliberations released today.

- US dollar retreats, commodity currencies outperform.

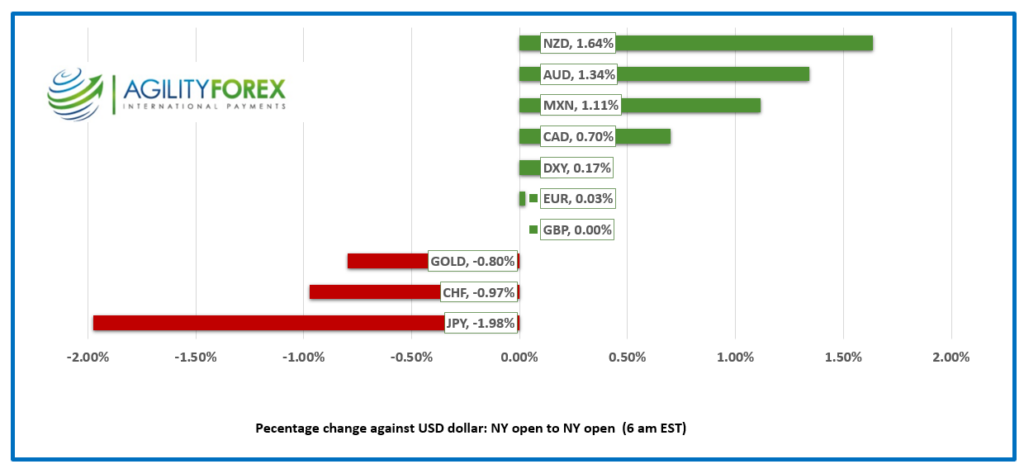

FX at a Glance

Source: IFXA/RP

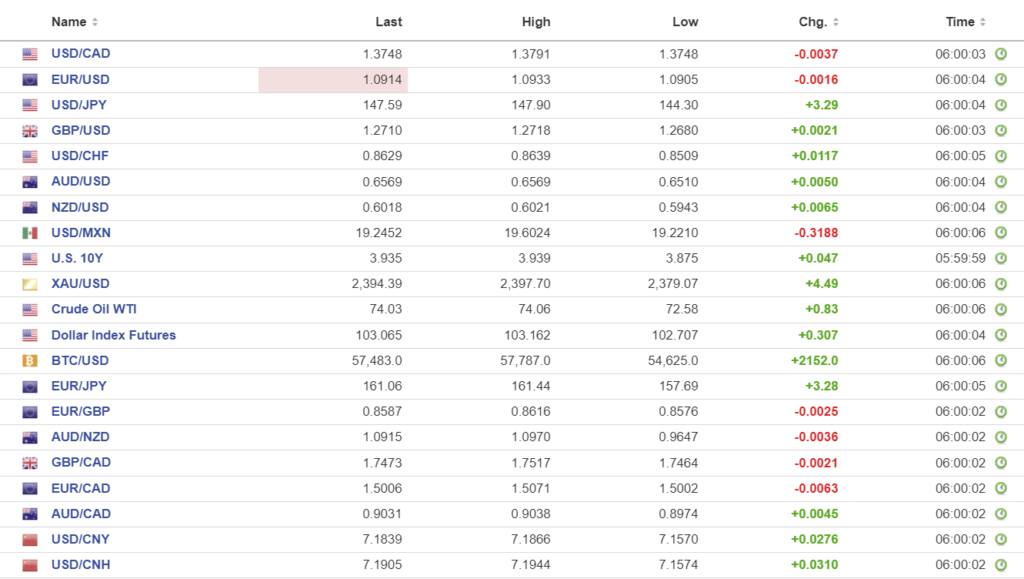

USDCAD open 1.3748, overnight range 1.3748-1.3791, previous close 1.3785

USDCAD soared and swooned with the ever shifting global risk sentiment currents. Rebounding equity markets and talk of an inter-meeting “emergency” Fed rate managed to turn negative risk sentiment into a sunny outlook. How long that sentiment lasts is anybody’s guess but its hard to believe everything is right with the world.

The BoC Summary of Deliberations from the July 24 monetary policy are released today but the recent market turmoil and Friday’s employment report suggest it will have limited impact.

Traders were emboldened by the sharp narrowing of CAD/US interest rate spreads which helped to fuel USDCAD selling.

WTI oil prices inched higher, rising from 72.58 to 74.50 and they are at the top of that band in NY trading.

The Ivey PMI survey is ahead but there are no top tier US economic releases.

USDCAD Technicals

USDCAD ran out of gas at the 1.3950 resistance area and plunged back to support in the 1.3740 area, which also defines the trading range, at least until next week’s US inflation report. The hourly USDCAD technicals are bearish while prices are below 1.3790 and looking for a break below 1.3740 to extend losses to 1.3710. A break above 1.3790 targets 1.3850.

Longer term, the USDCAD gently sloping uptrend line from February is intact above the 1.3590-1.3610 zone. Bollinger Band and RSI studies suggest USDCAD is not approaching extreme over-sold levels (daily chart) which suggests limited downside.

For today, USDCAD support is at 1.3740 and 1.3710. Resistance is at 1.3790 and 1.3850. Today’s Range 1.3730-1.3790

Chart: USDCAD daily

Source: DailyFX

There is Never Just One Raccoon

It’s over. Disaster has been averted. The Friday-Monday financial market meltdown that wreaked havoc across asset classes has given way to tranquility and optimism. Wall Street indexes rallied yesterday, and global indexes followed suit overnight. The US 10-year Treasury yield rose to 3.935% after touching 3.67% on Monday, and the greenback gave back some gains. Relieved traders and analysts are quickly dismissing the turmoil as merely another “summer market correction” that had outsized moves due to poor liquidity. Just remember, there is never just one raccoon in your attic, or one mosquito at your BBQ.

Be Happy, Buy Stocks

Asian equity indexes (except those in China) closed with gains. Japan’s Topix rose 2.26%, while Australia’s ASX 200 gained 0.25%. European bourses are higher, with the German DAX up 1.17%, which is a good intraday move but still below its combined Friday-Monday loss. The same holds true for the S&P 500. It closed yesterday with a gain of 1.04%, and S&P 500 futures are up 1.11% this morning. Even so, the combined Friday-Monday S&P 500 loss was 4.8%.

EURUSD

EURUSD is consolidating its Friday gains in a 1.0905-1.0933 range and trading with a bullish intraday bias while prices are above 1.0900. German industrial production rose 1.4% m/m compared to -2.5% in May, but the good news was offset by a slump in exports, which fell 3.4% in June.

GBPUSD

GBPUSD traded in a 1.2680-1.2718 range in a quiet session. News that UK housing prices rose 0.8% m/m in July did not have much, if any, impact on trading.

USDJPY

USDJPY took center stage overnight, rising from 144.30 to 147.90 before sliding back to 147.09 in NY. The gains occurred in the wake of comments by Deputy Governor Shinichi Uchida, who said, “the bank will not raise its policy interest rate when financial and capital markets are unstable.” Nevertheless, the comments merely suggest rate hikes will be delayed, not scrapped.

AUDUSD and NZDUSD

AUDUSD traded firmer in a 0.6510-0.6573 range due to an improvement in risk sentiment and higher commodity prices. Prices were also supported by the USDJPY rally.

NZDUSD rallied from 0.5943 to 0.6025 following an employment report that reduced the risk that the RBNZ would cut rates at the August 14 meeting. The unemployment rate rose to 4.6% from 4.3%, and the labor cost index ticked higher to 0.9% q/q compared to 0.8% previously.

USDMXN

USDMXN traded sideways in a 19.2210-19.6024 range but with a bullish bias as the uptrend from the middle of July is intact above 18.7000. US politics and carry trade flows are driving direction. Traders expect Banxico to cut rates by 25 bps to 10.75% tomorrow.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1386 vs exp. 7.1481 (prev. 7.1318).

Shanghai Shenzhen CSI 300 fell 0.34% to 3342.98

July Trade surplus drops to $84.4 billion from $99.95 billion

Chart: USDCNY and USDCNH

Source: Investing.com