Source: foreignpolicy.com

- Equities roiled by Hong Kong stock plunge

- Rishi Sunak may become 57th UK Prime Minister today

- US dollar begins lower than Friday open but below the close

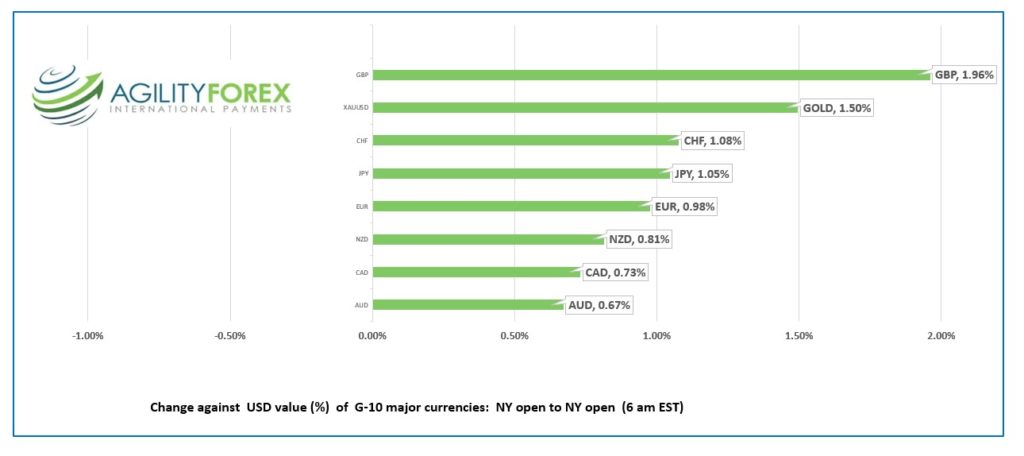

FX at a glance:

Source: IFXA Ltd/RP

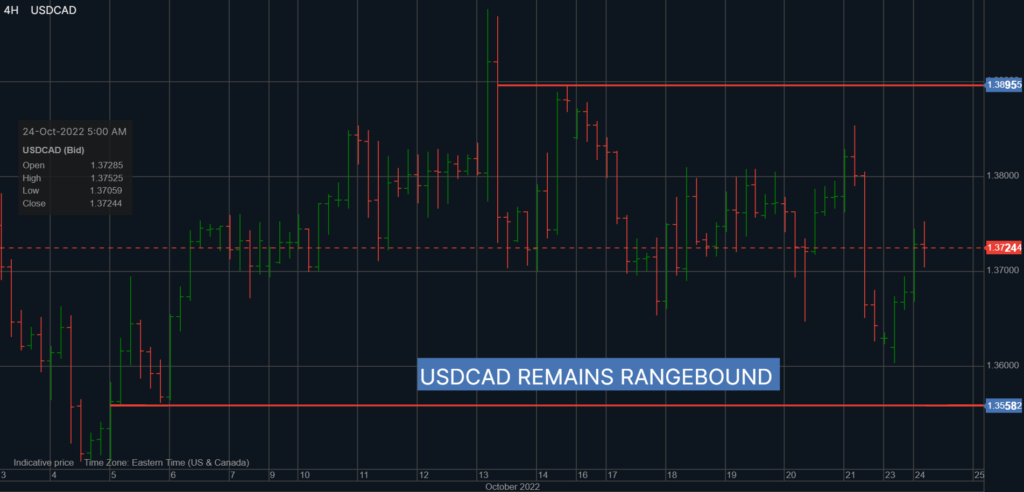

USDCAD Snapshot: open 1.3711-15, overnight range 1.3609-1.3753, close 1.3645

USDCAD opened today exactly where it opened Friday, but it is well travelled. Prices peaked at 1.3852 Friday and bottomed out at 1.3609 in early Asia today. They have since rallied to 1.3725 with direction determined by general risk sentiment as measured by S&P 500 price action.

The Bank of Canada will raise rates 75 bps on Wednesday which will likely generate chatter about slowing the pace of futures hikes. However, it will be the FOMC meeting on November 2 that drives USDCAD direction.

Canadian consumers feeling the pinch of rising prices for food and energy won’t get relief anytime soon, especially as the Federal government exacerbates rising prices through new carbon, fertilizer, and dairy taxes. Mr Trudeau is insulated because taxpayers feed his family. The National Post reports Trudeau billed taxpayers $55,000 for groceries last year which is a tad egregious when the average Canadian household income, before taxes is $75,452.00.

WTI oil prices are trading near the middle of their $82.68-$85.81 range with slowing global growth concerns weighing on prices.

USDCAD Technical outlook

The intraday technicals are modestly bid above 1.3660, looking for a break above 1.3760 to extend gains to 1.3850. A break below 1.3660 targets 1.3610 then 1.3550. Longer term, the uptrend from June is intact above1.3050.

For today, USDCAD support is at 1.3690 and 1.3660. Resistance is at 1.3760 and 1.3790. Today’s range: 1.3660-1.3750

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

It was a topsy-turvy overnight session due to UK politics, economic data, the US interest rate outlook, and China politics, but as NY opened, it was a case of “different day, same crap.”

This morning, the US dollar is sharply lower than it was at Friday’s open, but well above Friday’s closing rates.

China got the ball rolling. News that Xi Jinping manipulated himself into a third term, then stacked key leadership posts with lackeys crushed Chinese equity markets. The equity damage was contained to China.

Suspected Bank of Japan FX intervention roiled FX markets in early trading but if the BoJ’s goal was to weaken USDDJPY, they failed miserably.

Eternally optimistic US equity traders cited a Wall Street Journal article written by the Fed’s preferred “leak conduit” (Urinal?), that speculated the Fed would discuss slowing the pace of rate hikes. Many traders believe the article was approved “forward guidance,” and stocks rallied hard. That’s not going to end well. US inflation is far too high and interest rates are not driving prices lower.

Asia equity indexes closed mixed. The main Chinese indexes closed with steep losses while Australia’s ASX 200 gained 1.54%. European bourses are modestly higher. The German Dax is 1.46% higher while the UK FTSE 100 flipped from negative to a gain of 0.25%. S&P 500 futures are 0.40% higher. WTI oil fell 1.93%% while gold is close to unchanged from Friday’s close.

EURUSD traded sideways with a negative bias in a 0.9808-0.9899 band. Part of the reason may have been reports of sizeable option strikes expiring at 10:00 am ET. Traders are also biding their time until Thursday’s ECB meeting where a 75-bps rate hike appears fully baked-in. Prices were weighed down by weaker than expected September German and Eurozone Manufacturing PMI data

GBPUSD has been front and center and churned in a 1.1275-1.1405 range. Prices plunged in Asia around the time of suspected BoJ intervention in USDJPY then rose from 1.1299 to 1.1405. That rally ended swiftly and GBPUSD dropped to the low in NY due to UK Gilt yields which fell from 4.05% at Friday’s close to 3.837%. Rishi Sunak, former Chancellor of the Exchequer is expected to be become Prime Minister today. Weaker than expected UK Services and Manufacturing PMIs didn’t help sentiment.

USDJPY traded erratically due to BoJ intervention. Prices chopped around in a 145.55-149.70 range with the bottom occurring at the Asia open.

AUDUSD traded in a 0.6274-0.6410 range with comments from RBA Deputy Governor Chris Kent and rising USDCNY roiling markets. Mr Kent suggested there would be more rate hikes, but they would be data dependent

Chicago Fed National Activity Index is ahead.

Chart of the Day: USDJPY

Source: Saxo Bank

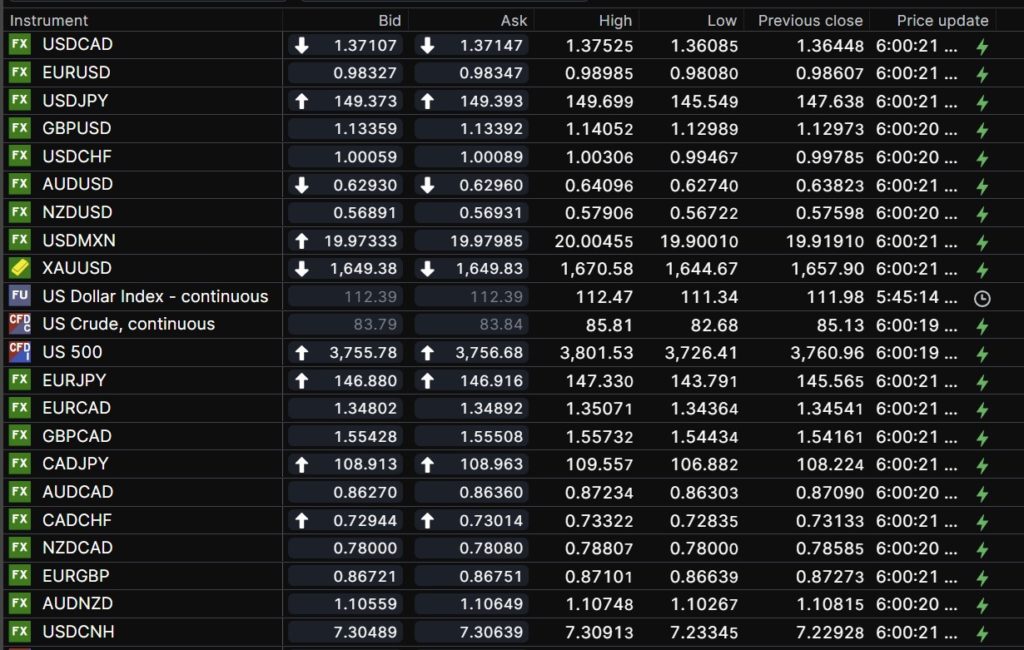

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

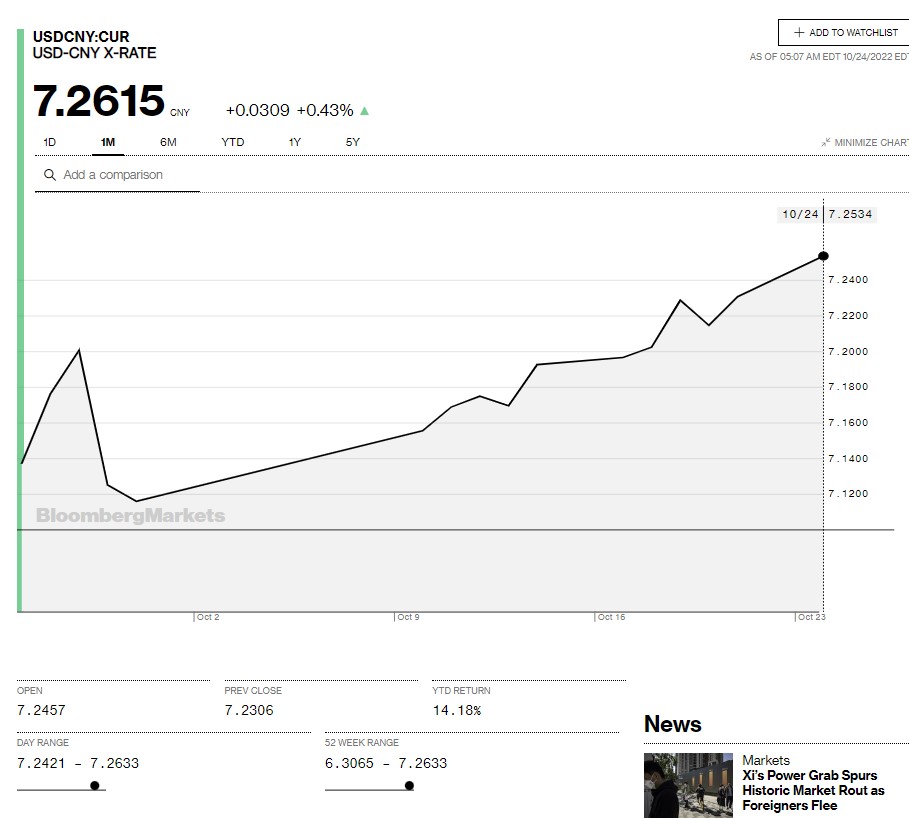

China Snapshot

Today’s Bank of China Fix: 7.1230, previous 7.1186

Shanghai Shenzhen CSI 300 fell 2.93% to 3633.37

China dumps a ton of data: The National Bureau of Statistics and Xi Jinping declared Q3 GDP rose 3,9% q/q (previous -2.9%) and 3.9% y/y compared to 0.4% previously.

China’s Trade surplus widened to $84.74 billion, September Retail Sales rose 2.5% y/y.

Hang Seng falls 6.3% to 15180.69 which was triggered by Emperor Xi Jinping stacks senior leadership role with lackeys, according to Bloomberg.

Chart: USDCNY 1 month

Source: Saxo Bank