March 6, 2024

- Fed Powell talks and BoC acts (no action is still an action)

- Hopes for tax cuts in UK budget underpin GBPUSD.

- US dollar opens with modest losses.

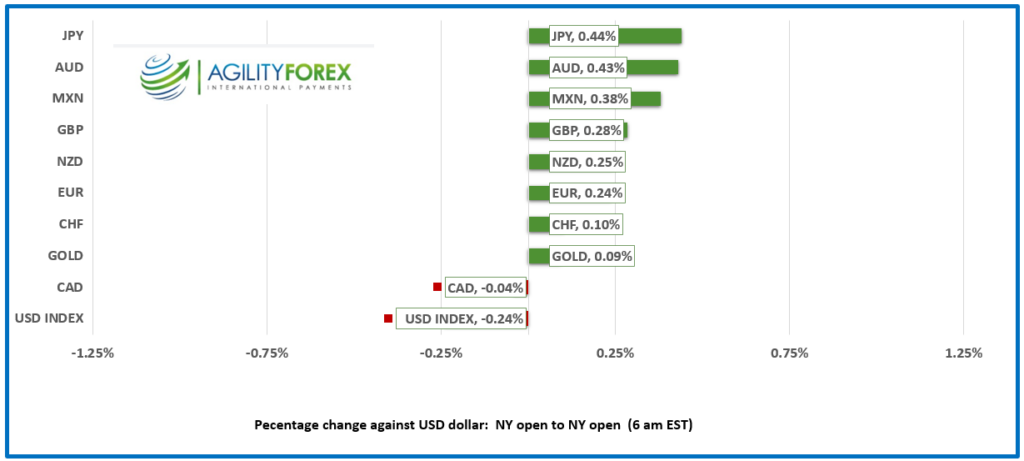

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3586-90, overnight range 1.3561-1.3600, close 1.3593

USDCAD drifted aimlessly in a narrow range overnight, unable to get and downside traction despite the generally weaker US dollar profile.

The Bank of Canada is universally expected to leave its benchmark rate unchanged at 5.0% at today’s meeting. Policymakers may take a bow and point out that recent data shows that high rates are slowing the economy and rebalancing the labour market. That’s good news unless you are one of the workers that got “rebalanced,” which is something that BoC employees need not fear.

But the Fed has not indicated that it is time to ease rates so neither will Tiff Macklem and company. The Bank will insist that rates need to remain in restrictive territory because of ongoing inflation pressures with an eye on “pent-up exuberance” in the housing market.

WTI oil prices are at the top of the $78.00-$79.03/b range supported by concerns that detours to avoid Red Sea shipping attacks will lead to tighter supply.

USDCAD Technicals

The intraday USDCAD technical are bullish a bullish above 1.3505 and looking for a move above resistance at 1.3620 to extend gains to 1.3780. A failure to break 1.3620 followed by a breech of 1.3450 sets the stage for a rest of the 1.3340 area.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3620 and 1.3650. Today’s range is 1.3510-1.3610.

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

There is a hive of economic activity today and the bees are swarming in Canada, the US and the UK. Chancellor Jeremy Hunt gets things rolling with the UK budget at 7:30 am when he is expected to offer a dollop of tax cuts. The JOLTS Job Openings survey (forecast 8.9m vs December 9.026 m) is next followed by the BoC monetary policy statement and Fed Chair Powell’s testimony to Congress.

The US ADP employment change data for February (forecast 150,000)

All this occurs against the contentious reoccurrence of the Biden/Trump Presidential election. Sleepy Joe vs Obnoxious Donny. Nikki Haley ended her campaign.

Wall Street had a bad day yesterday, and the three main indices closed down sharply, led by a 1.65% drop in the Nasdaq. Apple’s falling sales in China and the Tesla plant fire in Germany sparked the losses. Asian equity indexes were not concerned, as the Nikkei 225 index closed flat and Australia’s ASX 200 rose 0.12%. European bourses are higher in anticipation of somewhat dovish comments by Fed Chair Powell. The UK FTSE 100 leads the pack with a 0.22% gain ahead of the budget details.

EURUSD is at the top of its 1.0841-1.0880 range in NY, supported by German export data (actual 6.3% m/m vs. -4.5% in December) which suggest the Germany economy may have bottomed out. Unfortunately, the upcoming ECB meeting (Thursday) and Eurozone January Retail Sales (-1% y/y vs previous -0.5%) and are acting as a drag on gain. The EURUSD technicals are bullish above 1.0740, but a failure to break above 1.0910 suggests a retest of the uptrend line.

GBPUSD traded firmer in a 1.2690- 1.2732 range. Chancellor Jeremy Hunt is tabling his election-friendly budget which is promising tax cuts and an increase in the income threshold to receive benefits, along with cutting the employee national insurance rate. Jay Powell’s comments and the budget will determine if GBPUSD can break above 1.2830, a level which has capped gains since August 8, 2023.

USDJPY fell to 149.33 from 150.09from 150.09 to 149.31 after a Bloomberg article quoted Mitsubishi UFJ Financial Group analysts predicting that the Bank of Japan would end negative rates at the March 19 meeting. That move would be followed by another bump to 0.25% in October. Swaps traders are not convinced, and the odds are only 53% for a march rate hike.

AUDUSD is firmer, rising from 0.6492-0.6549 in Ny despite a mixed Q4 GDP report. The headline number was weaker than forecast (actual 0.2% q/q vs. forecast 0.3%) but the Q3 result was revised higher.

USDMXN traded in a 16.08946-16.9625 range due to broad US dollar weakness. The short-term technicals are bearish while prices are below 16.9750.

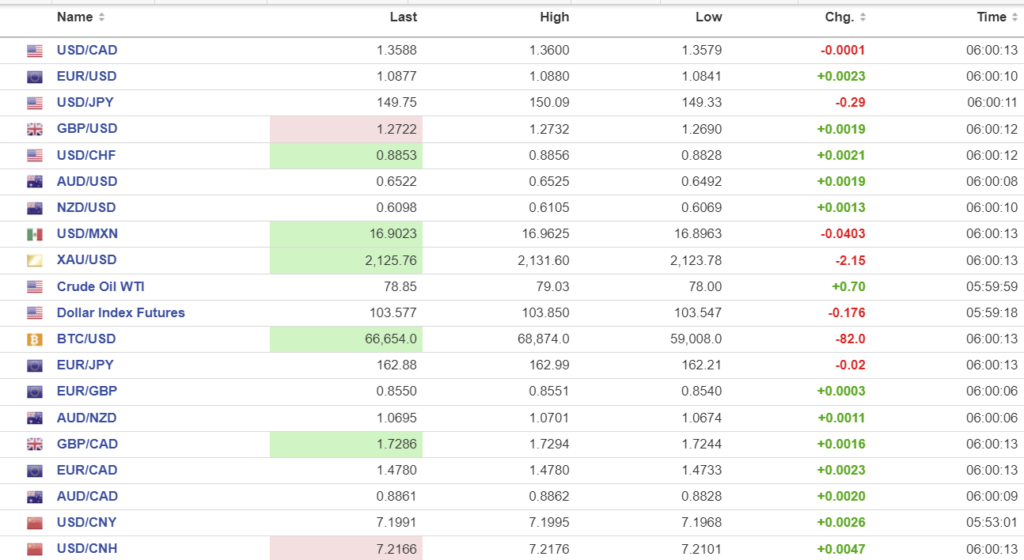

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

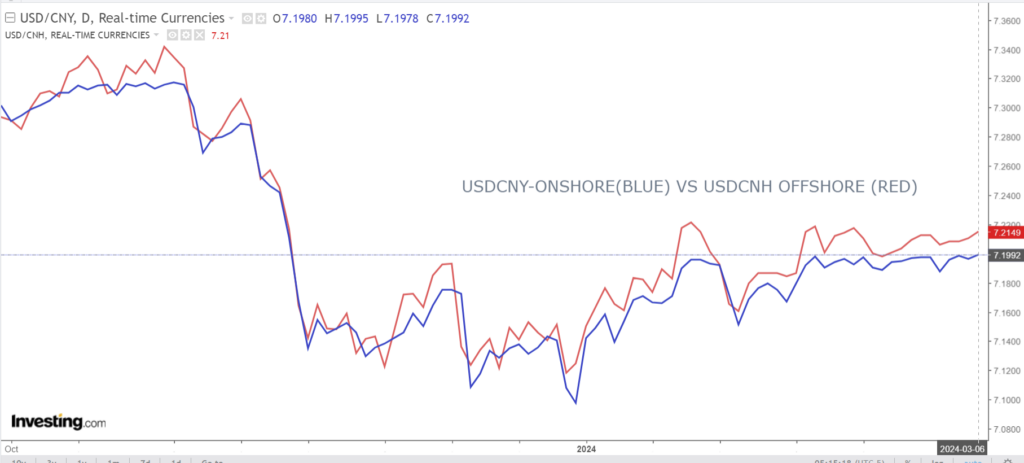

China Snapshot

PBoC fix: 7.1016, expected 7.1939, previous 7.1027.

Shanghai Shenzhen CSI 300 fell 0.41% to 3551.05.

Source: Bloomberg

Chart: USDCNY and USDCNH daily

Source: Bloomberg