Photo: Matt Groening

April 20, 2023

- China leaves interest rates unchanged.

- A barrage of Fed-speak is on tap today.

- US dollar opens mixed, trades narrowly overnight.

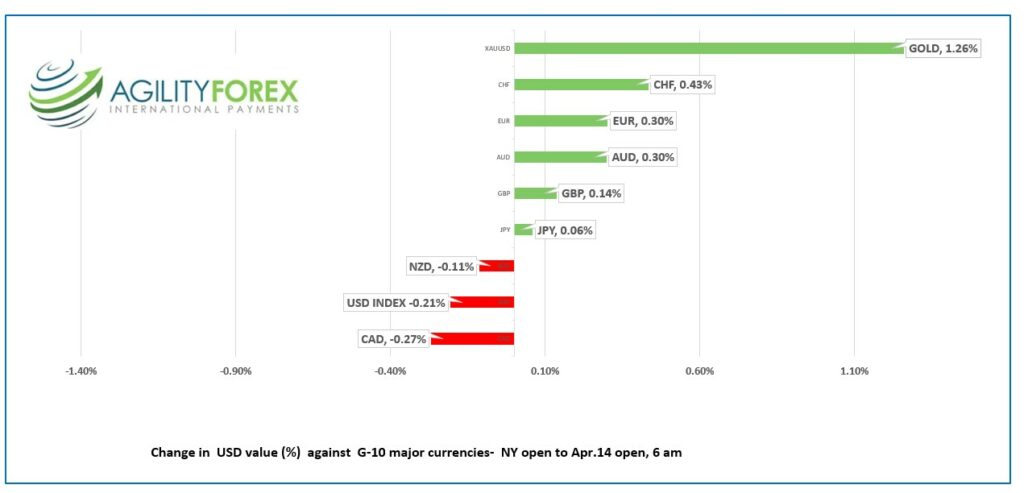

FX at a glance

Source: IFXA Ltd/RP

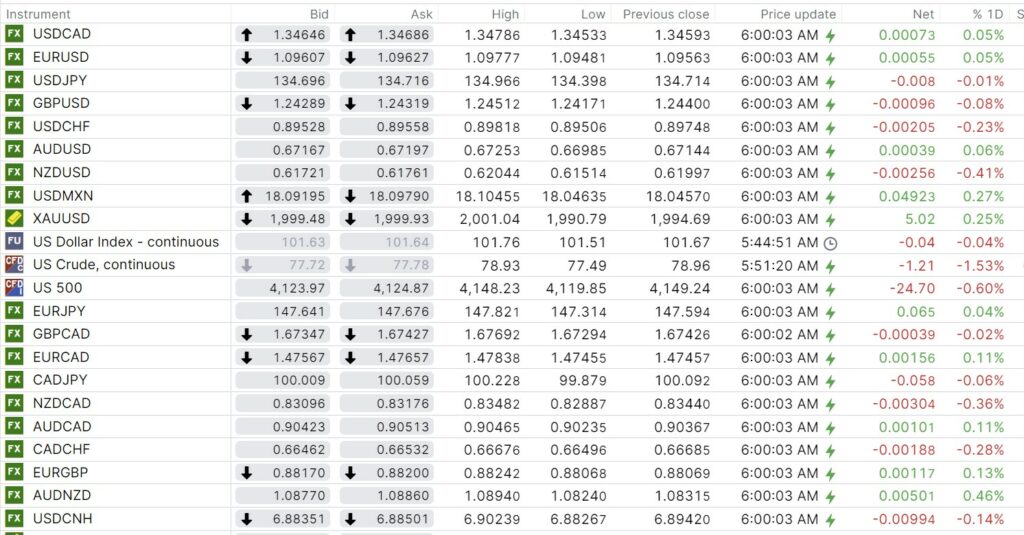

USDCAD Snapshot: open 1.3465-69, overnight range 1.3453-1.3479, close 1.3459

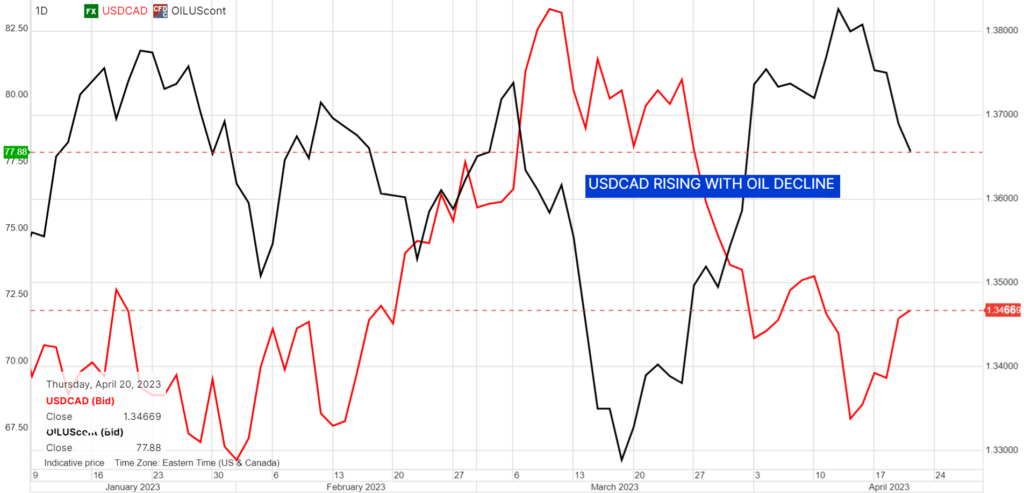

USDCAD has been bid all week and that didn’t change overnight. USDCAD gains have coincided with a decline in WTI oil prices, alongside renewed US dollar strength after traders downgraded expectations for the Fed to cut interest rates in the summer.

WTI is pushing through the post-Opec production cut low and appears poised to “fill-the-gap” which occurred when the cartel plus Russia announced a surprise production cut. Prices gapped open, rising from the Friday March 31 close of $74.37, to $81.42 on April 3, in Asia. Talk that US interest rates may go higher and stay elevated longer than expected is weighing on prices.

Russia found a new customer for its “sanctioned” oil. Reuters reported that Pakistan placed its first order with Moscow, with purchases expected to peak at 100,000 b/day.

USDCAD may also be supported by concerns that the Federal employees strike could negatively impact domestic growth. On the other hand, USDCAD gains could be capped after the Trudeau government caves to the PSAC demand and gives them the 13.5% raise over three years, they are demanding.

Governor Tiff Macklem and his sidekick Deputy Governor Carolyn Rogers are testifying before the Senate Committee on Banking today. Ho-hum.

USDCAD Technical Outlook

The intraday technicals are bullish while trading above 1.3410, looking for a break above 1.3490 to extend gains to 1.3550.

Longer term, the failure to sustain losses below the 2000-day moving average at 1.3405, and the subsequent rally above 1.3440 suggests that a short-term low is in place at 1.3305, and the 100-day moving average at 1.3530 is the next target.

For today, USDCAD support is at 1.3420 and 1.3390. Resistance is at 1.3490 and 1.3530.

Today’s range 1.3420-1.3520

Chart: USDCAD daily: CAD-Red, WTI-Black

Source: Saxo Bank

G-10 FX recap and outlook

Financial markets are standing around awaiting a call to action. So far, US quarterly earnings reports have not raised much of a stir and the latest economic reports, although fairly robust, have failed to deter hopes the Fed will chop rates before year end.

We will get more on that subject today from Fed policymakers, Williams, Waller, Mester, Bowman and Logan.

US weekly jobless claims rose 5,000 from the upwardly revised 240,000 seen last week. The Philadelphia Fed Manufacturing Survey was sharply weaker at -31.3 compared to 23.2 previously. It was the lowest reading since May 2020.

EURUSD is steady near the top of its overnight 1.0948-1.0978 range, supported by the belief the ECB will stay the course and continue to raise interest rates to at least 4.0%. The intraday EURUSD technicals are bullish above 1.0900, looking for a break of resistance at 1.1070 to extend gains to 1.1220.

GBPUSD traded in a 1.2417-1.2451 range as traders continued to digest Wednesday’s higher-than-expected inflation data. The inflation results suggest the Bank of England will lift rates by 25 bps to 4.50% on May 11. The intraday technicals are bullish above 1.2400, looking for a break above 1.2550 to extend gains to 1.2780.

USDJPY bounced 134.40-134.97 band with the session low occurring just as Europe opened. Broad US dollar demand and a steady US 10-year Treasury yield helped contain prices. Prices were also supported following a report that the BoJ will leave its yield curve control (YCC) policy unchanged at its next meeting.

AUDUSD rallied in Asia rising from 0.6669 to 0.6725 before retracing the move in Europe. Prices saw a little support from AUDNZD demand after the New Zealand inflation report, but the gains were erased by lower commodity prices.

The Australian government took the RBA to task in 2022 after RBA forecasts were out to lunch on inflation. The independent review criticized the make-up of the RBA board as it only included one economist, They want to see more economic expertise and they want to reduce the power of the Governor.

NZDUSD traded negatively in a 0.6152-0.6204 range. Prices dropped to the bottom after New Zealand inflation was lower than expected. Q1 CPI rose 1.2% m/m (forecast 1.7%), and 6.7% y/y (forecast 7.1%) which raised speculation that RBNZ interest rates may be closed to peaking.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

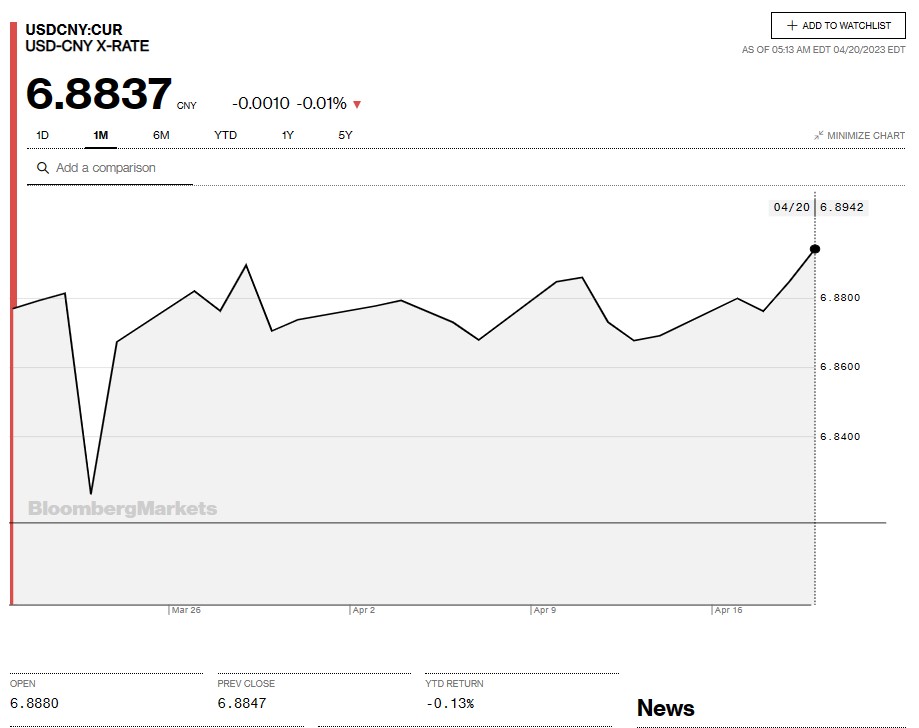

China Snapshot

Bank of China Fix: 6.8987, Previous: 6.8731

Shanghai Shenzhen CSI 300 fell 0.26% to 4113.02.

PboC leaves rates unchanged: 1-year Loan Prime Rate (LPR) 3.65%, 5-year LPR 4.30%

Chart: USDCNY 1 month

Source: Bloomberg