Photo: HDclipart.com

- Markets noisy and choppy awaiting FOMC Wednesday

- Light data calendar puts US earnings reports in focus

- US dollar opens firmer compared to Monday open, but a tad softer from close

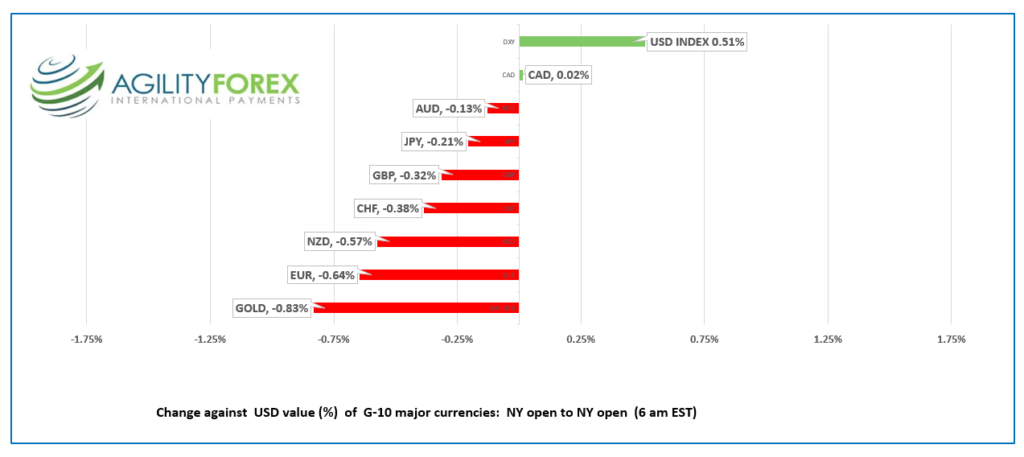

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.2865-69, overnight range 1.2818-1.2887, close 1.2847

USDCAD tested support in the 1.2820 area yesterday despite the S&P 500 drifting lower, WTI oil prices falling, and the other commodity currencies struggling. There were no economic reports of note suggesting the move was a factor of position adjusting ahead of the Fed meeting, in a thin market.

WTI oil prices are in a month-long downtrend while prices are below 101.50 with traders concerned that rising global rates will crush demand which is already suffering from China’s covid issues and slowing economy

USDCAD stayed relatively firm in the face of the Bank of Canada’s 100 bp rate hike July 13. BoC officials made the move because inflation was too high, and they were worried that Canadians were starting to believe that “inflation was here to stay.” They framed the narrative as a front-loaded, pre-emptive strike but in reality, it was a long-overdue reaction to a problem that they ignored for too long.

The BoC failed its mandate to keep inflation low, stable, and predictable. Nevertheless, the pathetic performance garnered pay raises and bonuses for 1,752 employees in 2021.

The Canadian economic calendar is empty, leaving USDCAD direction to be determined by Wall Street.

USDCAD technical outlook

The USDCAD technicals are unchanged from yesterday. The failure to break below support in the 1.2810 area suggests further consolidation in a 1.2810-1.3100 range. The intraday technicals flipped to bullish with todays move above 1.2850, which suggests an extension to 1.2950.

For today, USDCAD support is at 1.2810 and 1.2810. Resistance is at 1.2890 and 1.2930. Today’s Range 1.2820-1.2910

Chart: USDCAD 1 day

Source: Saxo Bank

G-10 FX recap and outlook

Traders are in a persnickety mood as they mark time ahead of Wednesday afternoon’s FOMC meeting and Fed Chair Powell’s press conference.

The Fed is widely expected to raise rates by 75 bps after policymakers downplayed the need for a 100 bp hike. Some analysts are already looking ahead to the Fed’s first rate cut as they are convinced, they know inflation has peaked and the level for the top of this rate hiking cycle. Those views are giving equity and bond traders some hope.

If you think the current inflation problem is a result of the world’s central banks mismanaging monetary policy during the pandemic, former RBNZ Governor Graham Wheeler agrees.

The report says that central banks overall

- were too confident about their monetary policy framework.

- were too confident about their models.

- were too confident they could control output and employment.

- lost their focus on price stability and took on too many mandates.

- faced conflicts in some cases with conflicting ‘dual mandate’ objectives; and

- were distracted by extraneous political objectives, such as climate change.

Elsewhere, the EU, particularly Germany, cheered when Russia turned on the gas taps, but the joy turned to dismay when Putin cut the flow by 20% of its previously reduced output.

Asian equity indexes were mixed. Japan’s Nikkei 225 fell 0.16%, while Australia’s ASX 200 gained 0.26%.

Hong Kong’s Hang Seng Index outperformed, rising 1.67% on news Alibaba will make its primary listing in Hong Kong.

European bourses are in the red but above their worst levels. The UK FTSE100, is the outlier, positing a 0.56% gain.

US equity futures are modestly lower on negative sentiment after Walmart cut its profit outlook and GM’s profit dropping 40%. Gold trades lower while WTI is 1.56% higher.

The US 10-year Treasury yield topped out at 2.84% yesterday and is trading at the overnight session low of 2.737%.

EURUSD traded in a 1.0117-1.0249 range. Russia is jerking the EU around on gas pipeline shipments. They restarted shipments when a repaired turbine was shipped which lifted EURUSD yesterday. Then Gazprom reduced the shipments by 20%, which is a big deal because the pipeline is only shipping at 40% of capacity.

The EU is outraged, and the group agreed to reduce gas imports from Russia by 15% this winter. The reduction is voluntary, leaving plenty of wiggle room for countries to put their citizens ahead of the bloc.

The EURUSD outlook is negative due to fears the economic slowdown and looming energy crisis will limit the ECB’s ability to address soaring inflation.

GBPUSD rose then fell in a 1.1965-1.2089 range with prices mirroring EURUSD moves. The currency got a bit of support after Barclay’s Bank predicted a 0.50% rate hike at the BoE meeting, August 4. However, ongoing political uncertainty and weak economic data limit gains.

USDJPY consolidated losses in a 136.29-136.84 range following the drop in the US 10-year yield to 2.737%.

AUDUSD traded sideways in a 0.6924-0.6966 range with price action tracking broad US dollar sentiment.

Today’ US data includes Case Shiller Home price index and Consumer Confidence.

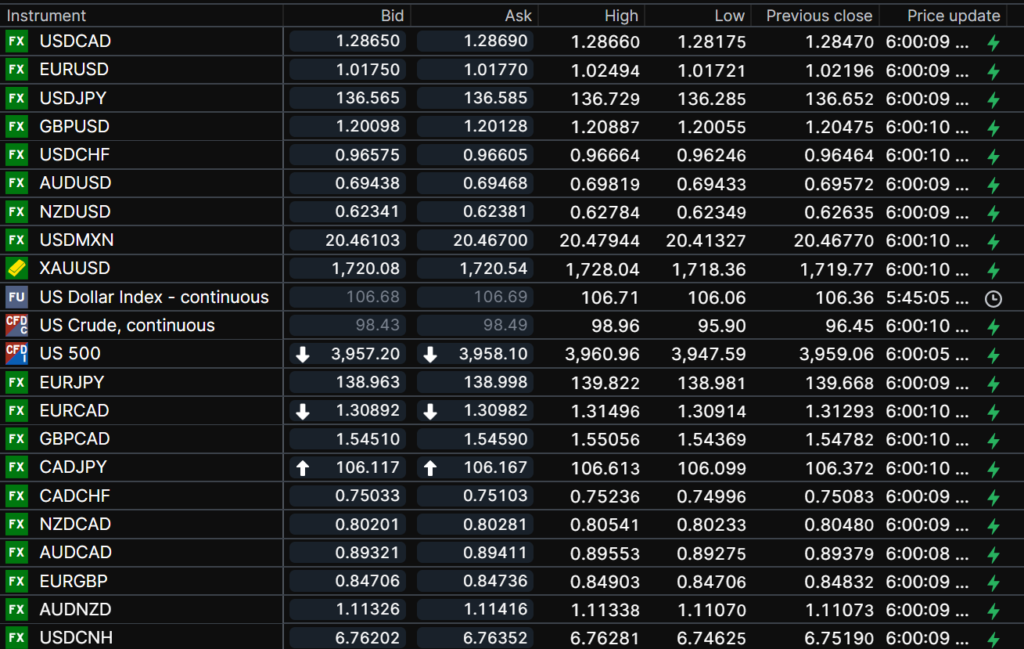

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.7483, previous 6.7543

Shanghai Shenzhen CSI 300 rose 0.79% to 4,245.96

Biden planning call with Xi Jinping to discuss Taiwan

Chart: USDCNY 5 day

Source: CNBC