Photo: wannapik.com

March 17, 2023

- PBoC cuts RRR by 25 bps

- Triple-witching hour expiries may roil markets this morning.

- US dollar slides.

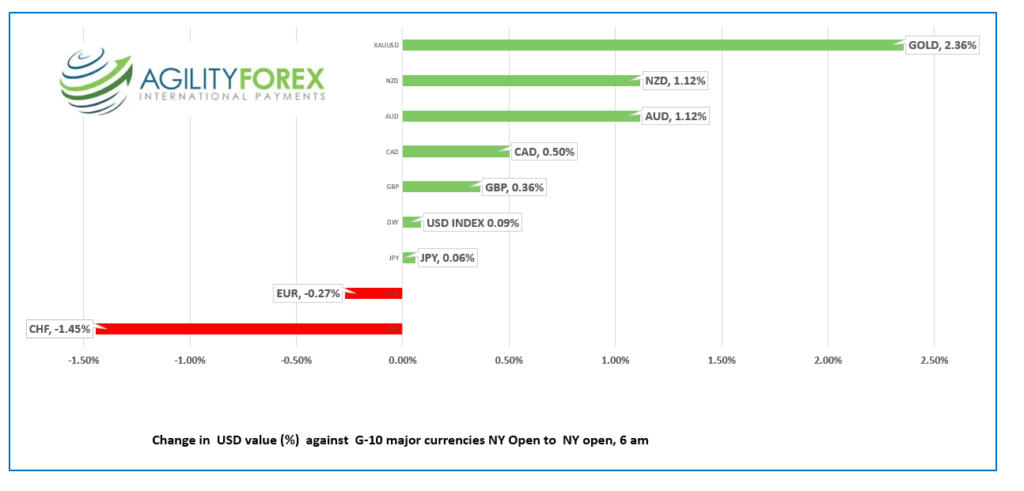

Weekly FX at a glance-Monday -Friday NY open

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3696-00, overnight range 1.3680-1.3735, close 1.3721

USDCAD dropped from 1.3786 yesterday to 1.3680 overnight after risk sentiment turned positive when the Swiss National Bank provided $54 billion in support to Credit Suisse. The S&P 500 index rallied and closed with 1.76% gain, which overshadowed weak oil prices.

WTI slid to $65.75/barrel yesterday then rallied to $69.62 overnight before dropping again, reaching $67.16 in NY. The nearly 20% drop, peak to trough since Monday seems overdone. ING Bank cut its Brent forecast price to $90.00/barrel from $98.00/b for 2023.

Canada Raw Materials and Capacity Utilization data is on tap but it won’t impact USDCAD trading.

USDCAD Technical Outlook

The intraday USDCAD technicals flipped to bearish with the move below 1.3730 yesterday, and are now looking for a break below support in the 1.3650-60 area to extend losses to 1.3550.

The 4-hour chart shows that the February 14 uptrend line is still intact above 1.3670 while the downtrend line from the March 10 peak comes into play at 1.3780.

For today, USDCAD support is at 1.3660 and 1.3610. Resistance is at 1.3740 and 1.3780

Today’s range 1.3660-1.3740

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

A series of bank rescue packages from the Swiss National Bank, US government departments (Fed, FDIC, Treasury) and eleven, generous US banking giants, turned the market’s doom and gloom outlook to one of sunshine and unicorns.

Global stock markets are higher, Treasury yields have rebounded from this week’s lows and the US dollar is lower except against the safe-haven currencies, Japanese yen, and Swiss franc.

The optimism seems misguided. Core-inflation (the measure that matters) is still very sticky in the US, Canada and Europe, the Fed is expected to hike rates next week, and of the 4,157 commercial banks in the US, it is really hard to believe that Silicon Valley Bank, Signature Bank and First Republic Bank are the only three with financial issues.

Equity markets may see additional turmoil today from “triple-witching” hour. Bloomberg reports $2.7 billion of derivative contracts mature today.

Today’s US economic data releases are second-tier. The University of Michigan Consumer Sentiment could create a bit of stir if it deviates sharply from the 67 expected. Nevertheless, the focus is on Tuesday’s FOMC meeting. The Fed is expected to raise rates by 25 bps.

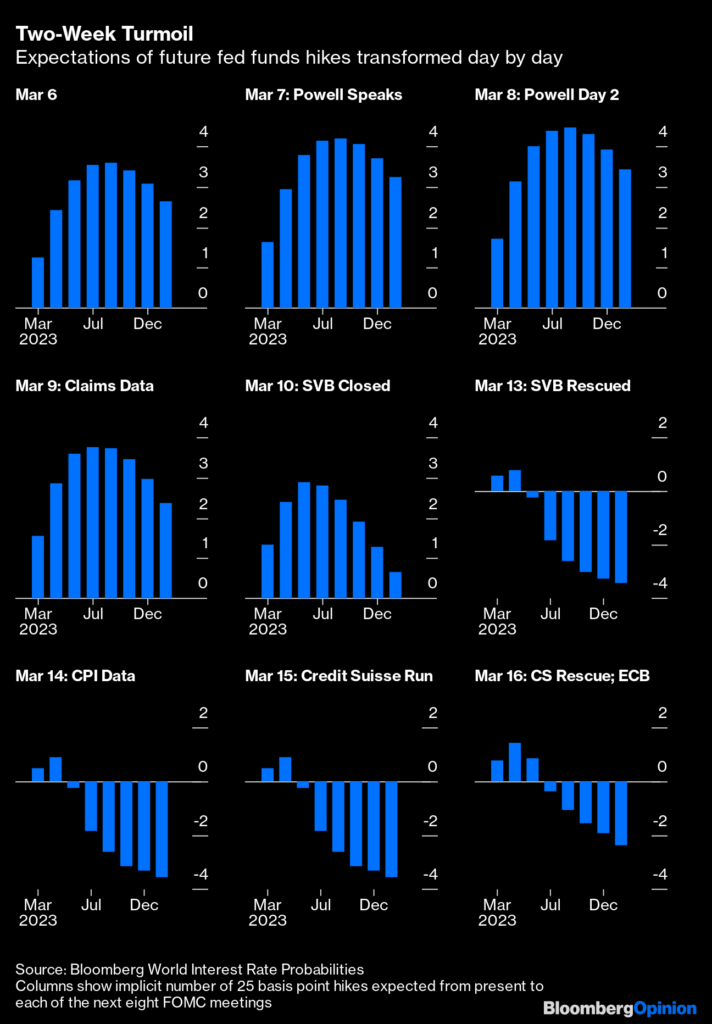

Bloomberg’s John Authers summed up the recent financial turmoil in a series of charts that show how the forecast for future Fed rate hikes changed over a two week period.

Source: John Authers-Bloomberg

EURUSD bounced from its ECB low of 1.0552 to 1.0669 in early European trading. Prices have since eased to 1.0618 in NY. The ECB hiked raised rates 50 bps and upgraded inflation forecasts to 5.3% in 2023 and 2.9% in 2024. The statement said that policymakers would revert to a data dependent approach to rate hikes.

GBPUSD is trading at 1.2134 in NY, after spending the overnight session in a 1.2104-1.2175 band. The Bank of England is expected to increase rates by 0.25% next week, partly because of the ECB’s actions.

USDJPY slid steadily, falling from 133.74 to 132.11 in NY on the heels of rapidly falling Treasury yields. The 10-year yield dropped to 3.447% today from 3.585% yesterday. Lingering safe-haven demand for yen is playing a role as well.

AUDUSD is giving up overnight gains with prices falling from 0.6723 to 0.6692 in NY, but still better than the overnight low of 0.6651.

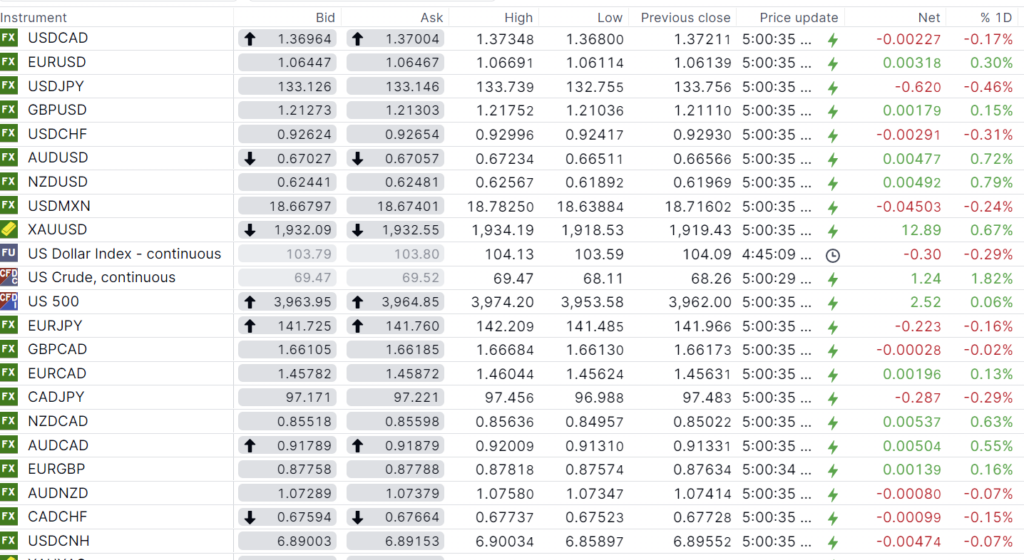

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Bank of China Fix: 6.9052, Previous: 6.9149

Shanghai Shenzhen CSI 300 rose 0.50% to 3958.82.

PboC cuts Reserve Requirement Ratio (RRR) 25 bps to an average of 7.6% for financial institutions

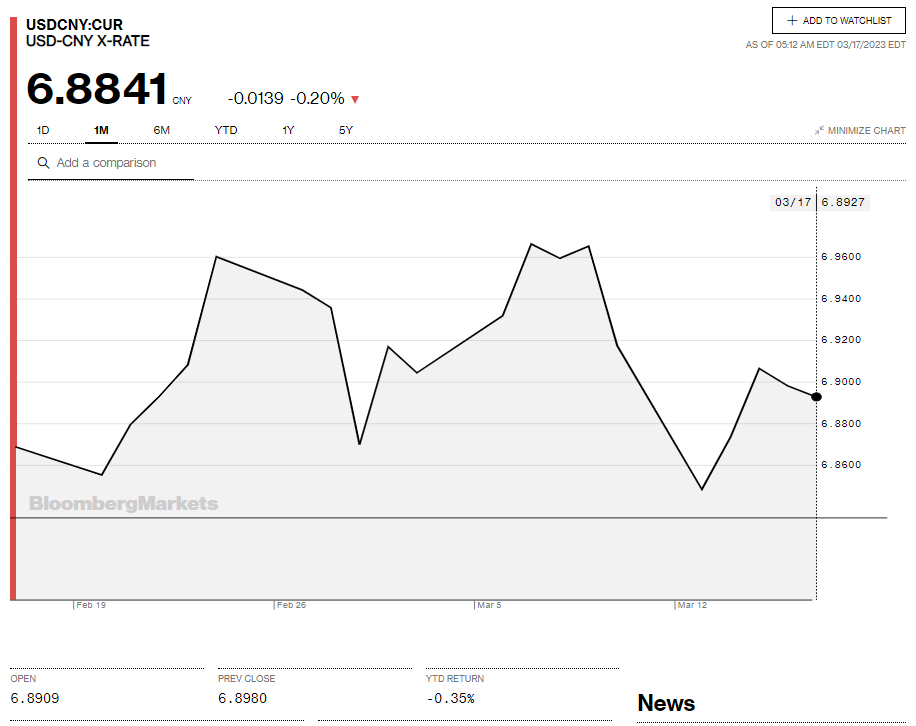

Chart: USDCNY 1 month

Source: Bloomberg