March 13, 2024

- Hot US CPI numbers put on ice.

- UK GDP rises 0.2% m/m in January.

- US dollar opens steady; seeks new catalyst.

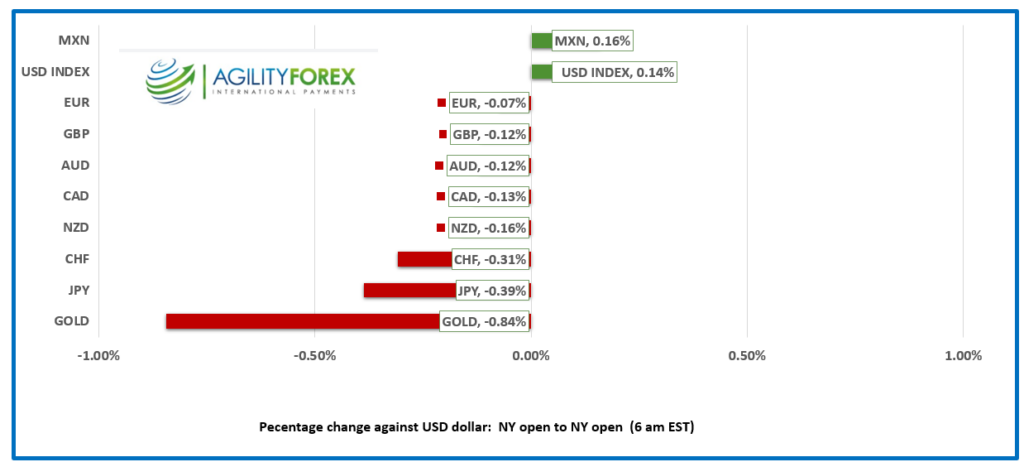

FX at a Glance

Source: IFXA/RP

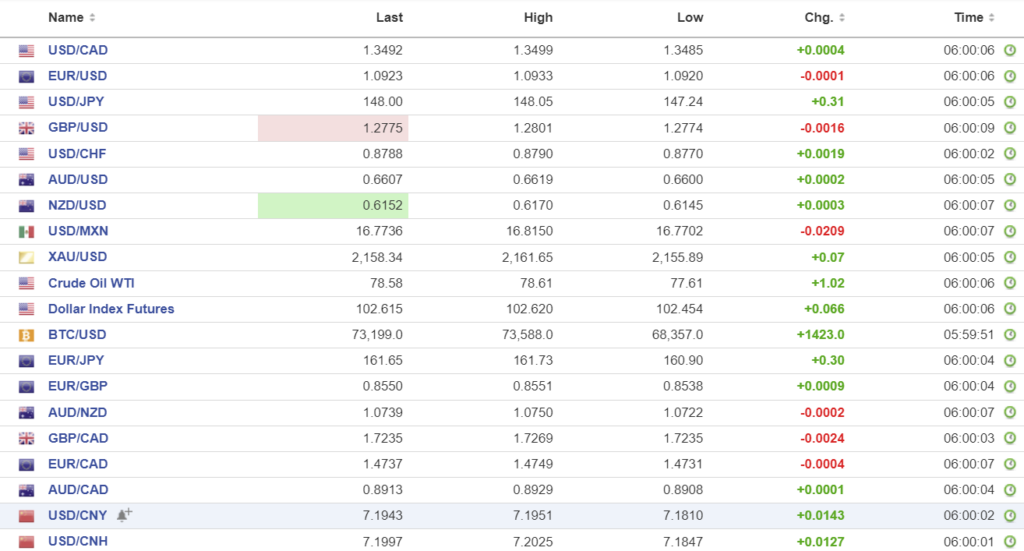

USDCAD Snapshot: open 1.3490-94, overnight range 1.3485-1.3499, close 1.3493

USDCAD is directionless and will continue to rise and fall with the prevailing risk sentiment. The loonie is at the mercy of the Fed’s interest rate outlook and the timing of the expected rate cuts. Yesterday’s CPI data did nothing to change the market’s view that the first cut may occur in June, despite Fed officials suggesting such a move may not occur until Q3.

WTI oil prices are at the top of its overnight $77.61-$78.77 range supported by the hefty drawdown of US crude inventories in the week ending March 8. The American Petroleum Institute reported a 5.52 million barrel decline in crude stocks.

There are no Canadian economic reports today.

USDCAD Technicals

The USDCAD intraday technicals ( hourly chart)l are bullish above 1.3460, looking for a break above 1.3510 to extend gains to 1.3570. A break below 1.3460 suggests further losses to 1.3410.

USDCAD price action is also contained by the 200 day moving average at 1.3475 and the 100 day moving average at 1.3520. 1.3550 is also the 50% Fibonacci retracement level of the November-December range.

For today, USDCAD support is at 1.3460 and 1.3410. Resistance is at 1.3520 and 1.3550. Today’s range is 1.3460-1.3530.

Chart: USDCAD daily

Source: Daily FX

G-10 FX

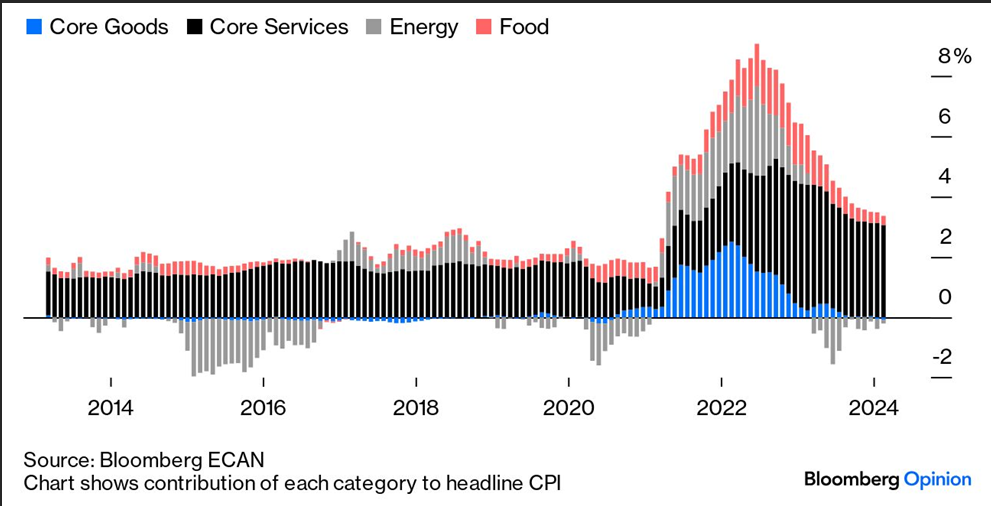

Global markets and a hamster in a wheel are energetic but going nowhere. The hotter than expected US CPI report was not really all that hot. The key metrics like the trimmed mean and supercore measures reversed January gains. Analysts pointed out that the CPI increase was in services and most of that was the cost of housing, which is also a lagging indicator. The results did not change expectations for the timing of the first Fed rate cut.

Source: John Authers, Bloomberg

Wall Street ignored the CPI data and powered the S&P 500 to a new record close. Asia markets were more subdued. Japan’s Nikkei 225 index fell 0.26% while the Australian ASX 200 gained 0.22%. European bourses are posting gains led by a 0.56% rise in the French CAC 40 index. SP500 futures are flat.

Traders are also ignoring fiery rhetoric from Russian President Vladimir Putin. The Madman of Moscow reiterated his threat to use nuclear weapons. “Our triad, the nuclear triad, it is more modern than any other triad. Only we and the Americans actually have such triads. And we have advanced much more here.” The comments were likely aimed at Western officials who suggested putting NATO troops on the ground in Ukraine.

News that the world will suffer from another Biden/Trump election has many people hoping Putin acts.

EURUSD inched higher in a 1.0920-1.0947 range despite soft Eurozone Industrial Production which dropped more than forecast (actual -3.2% m/m, forecast -1.5%, December 1.6%) in January.

GBPUSD is drifting in a 1.2774-1.2801 band. UK GDP data was promising as it suggested that the UK recession may have already ended (January GDP rose 0.2% m/m) but the results were expected. The GBPUSD uptrend line is intact above 1.2650. The odds for a June rate cut are 50% and 100% for an August cut.

USDJPY rallied to 148.05 from 147.24supported by the 10-year US Treasury yield rising to 4.162% from 4.087% on Tuesday. BoJ officials wanted to see higher wages to see if 2.0% inflation is sustainable before raising rates. Some of that wish was granted. Toyota agreed to its biggest wage hike in 25 years, while Panasonic, Nippon Steel, and Nissan also agreed to union wage demands.

AUDUSD is directionless in a 0.6600-0.6619 range. Negative Chinese developer news offset minor support from the news China repealed tariffs on Australian wine. Even so, the currency pair is above yesterday’s post-US CPI low of 0.6584.

NZDUSD traded quietly in a 0.6145-0.6170 range. The New Zealand food price index fell 0.6% from an upwardly revised 1.2% m/m in January. The results will do nothing to change the RBNZ “wait and see” approach to monetary policy.

USDMXN drifted lower in a 16.7702-16.8150 range with traders largely ignoring yesterday’s US inflation numbers. Mexico’s Industrial production data met expectations and helped to limit USDMXN gains.

The US data calendar is empty.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0930 vs exp. 7.1775 (prev. 7.0963}.

Shanghai Shenzhen CSI 300 fell 0.70% to 3572.36.

China’s property developer woes just won’t go away. China Vanke ( a state-backed developer) had its bonds downgraded to junk by Moody’s on Monday and authorities have ordered Chinese banks to “assist” the company. Country Garden holdings bondholders sai that did not receive a coupon payment on Tuesday .

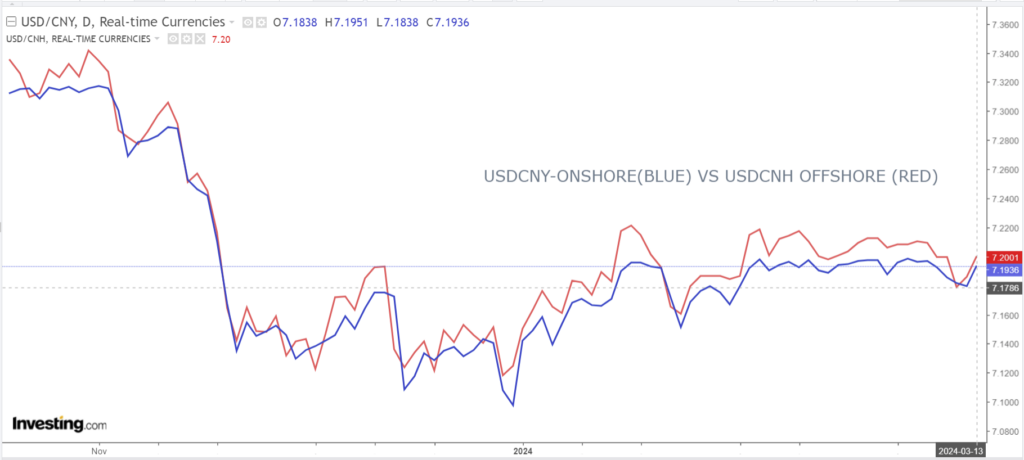

Chart: USDCNY and USDCNH daily

Source: Investing.com