Source: Pixabay

- Global equities continue to slide, pare losses after US data

- Soft Euro area and German data weigh on EURUSD

- US dollar extends yesterdays gains, but off its best levels in NY trading

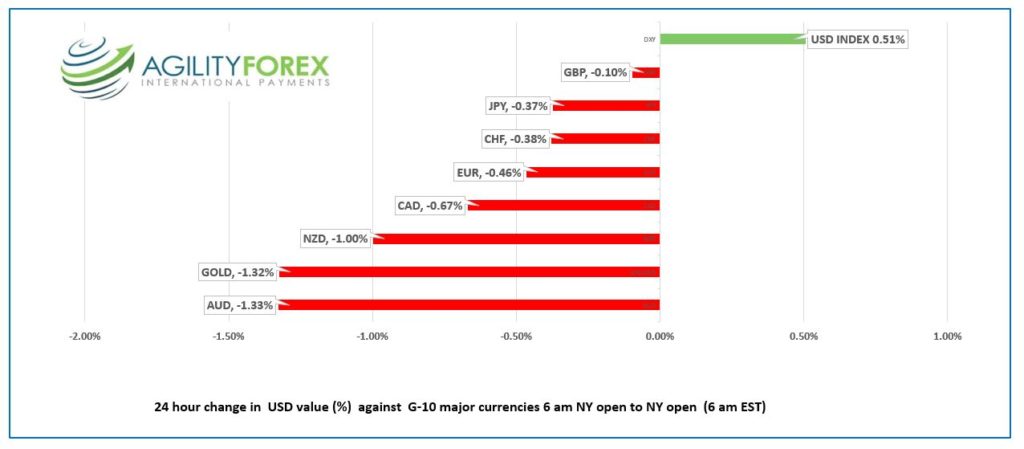

FX at a Glance

Source: IFXA Ltd/RP

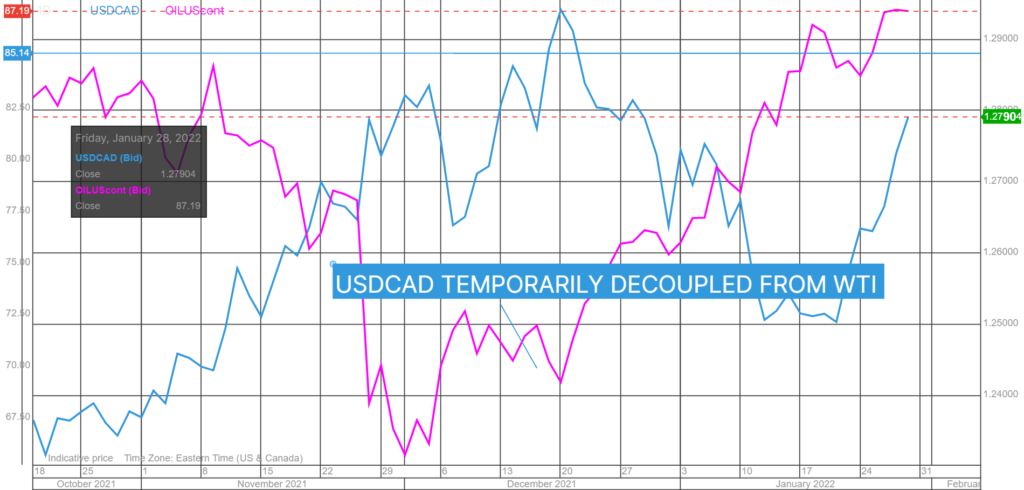

USDCAD Snapshot: Open 1.2787-1.2791, Overnight Range-1.2715-1.2795, previous close 1.2742

USDCAD traders attempted to breakout above 1.2800 today but were thwarted. Rising oil prices and the outlook for even more gains will function as a drag on USDCAD gains, but month-end portfolio rebalancing demand for US dollars is providing support.

USDCAD is being driven higher by the hawkish Fed outlook. However, the Bank of Canada is no less hawkish, merely timid. The BoC will raise rates in March and maybe another six times before year end.

USDCAD price action has decoupled from WTI moves for the past few days after being closely correlated for the past few months. That is unlikely to last. The mix of rising oil prices and BoC rate hikes suggest USDCAD gains are limited.

Technical view: The USDCAD technicals are bullish while prices are above 1.2640, looking for a break above 1.2810 to extend gains to 1.3000. A move below 1.2750 points to a retest of 1.2640, but only a decisive breach of the 1.2640 negates the upside pressure.

For today, USDCAD support is at 1.2740 and 1.2710. Resistance is at 1.2810 and 1.2850. Today’s Range 1.2750-1.2840

Chart USDCAD and WTI daily

Source: Saxo Bank

G-10 FX recap and outlook

January 2022 will not be looked upon favourably by equity market bulls or US dollar bears. The New Zealand and Australian dollars are shaping up to be the worst-performing G-10 currencies since the Jan.5 NY open, losing 3.55% and 3.09% against the US dollar. The Japanese yen is the only gainer, rising a mere 0.38%.

Asia equity traders rode the Wall Street roller-coaster and when the ride ended, the results were mixed. Japan’s Nikkei and Australia’s ASX 200 gained over 2.0% while Chinese indexes slumped ahead Lunar New Year.

European bourses are deep under water weighed down by month-end flows, poor risk sentiment, and weak Eurozone data. Gold continues to retreat as rate hike fears trump geopolitics, and WTI oil remains bid. The US 10-year Treasury yield is a tad firmer at 1.82%.

The risk outlook took a brief turn for the better after today’s US data was a tad softer than expected Fed Chair Jerome Powell watches the PCE index and it rose 0.4% m/m in December, below the 0.6% m/m increase in November. The Employment Cost Index rose 1.0% in Q4, down from 1.3% previously.

Russia Foreign Minister Sergei Lavrov said Russia is analysing NATO and US proposals and will respond, adding that Russia does not want war with Ukraine. His comments boosted the Russian rouble, but G-10 currencies were not impacted.

FX price action continues to be fueled by Fed Chair Powell’s hawkish flip and free-falling equity markets.

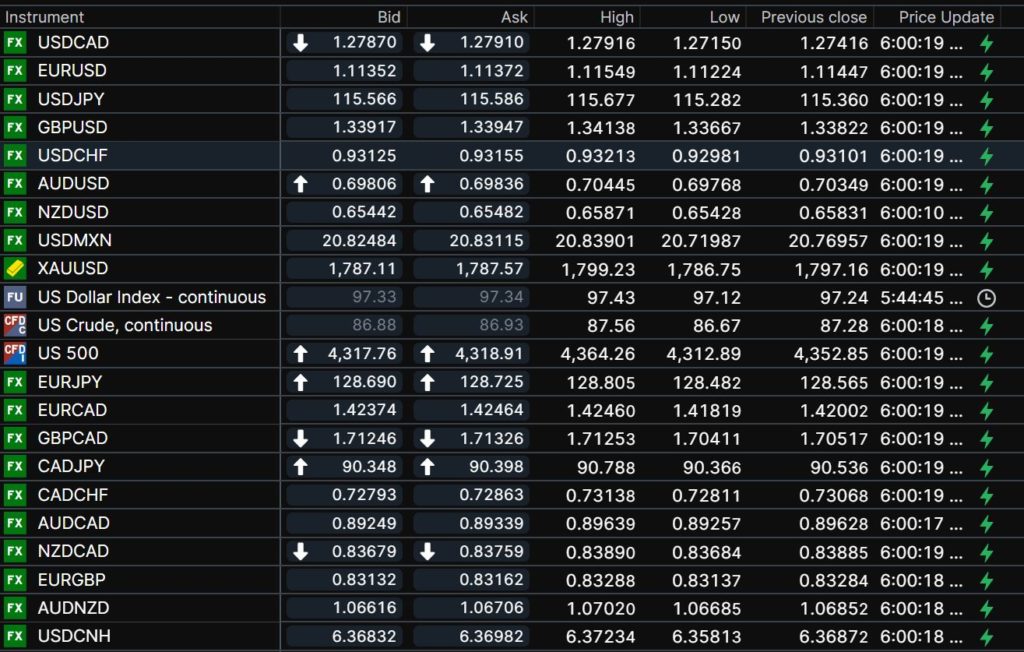

EURUSD dropped to 1.1122 from 1.1163 in Europe then bounced to the top of the band after the US data. Nevertheless, sentiment remains negative with traders looking ahead to next week’s ECB monetary policy meeting. Eurozone Economic Sentiment, Industrial Confidence, Services Sentiment, and German Q4 GDP were weaker than forecasts mainly due to Omicron and supply chain issues. The EURUSD outlook is negative below 1.1270.

GBPUSD bounced in a 1.3367-1.3414 range in Europe and then broke to the topside after the US data. Prices are underpinned due to expectations the Bank of England raises interest rates next week and issues a hawkish outlook.

USDJPY is tracking Treasury yields price action with prices drifting from to the bottom of its 115.26-115.68 range in NY trading.

AUDUSD rebounded in NY trading, but prices remained in the overnight 6969-0.7045 range. Traders are looking ahead to Tuesday’s RBA meeting anticipating a hawkish shift. NZDUSD outperformed against AUDUSD.

Chart of the Day: CBOE Volatility Index (VIX)

Source: Yahoo Finance

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

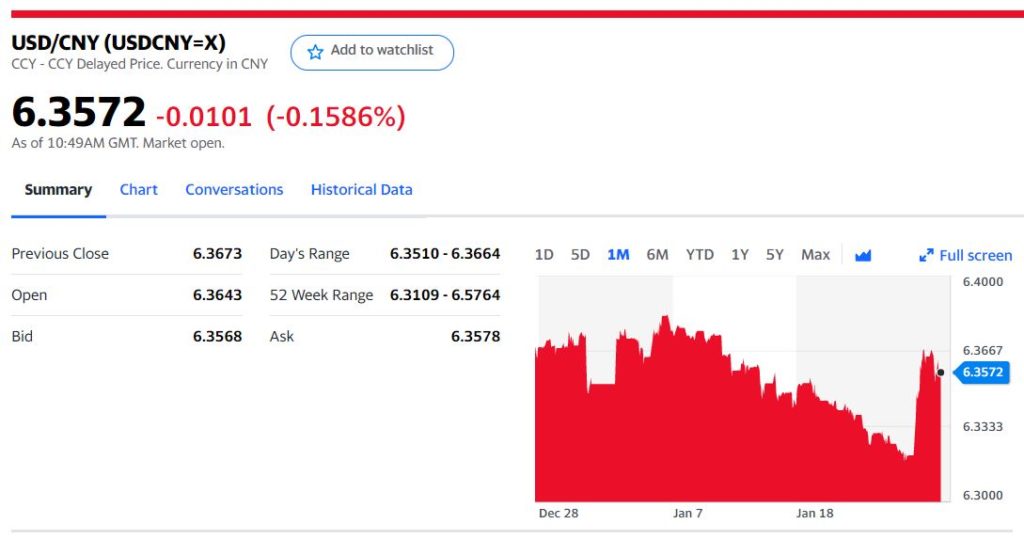

China Snapshot

Today’s Bank of China Fix 6.3746, previous 6.3382

Shanghai Shenzhen CSI 300 fell 1.21% to 4,563.77

Next week Chinese markets closed for Chinese New Year-January 31 to February 15.

Chart: USDCNY 1 month

Source: Yahoo Finance