Source: HDClipartall.com

- Fed officials push back against fresh Fed Pivot chatter

- Oil gains on Opec cuts

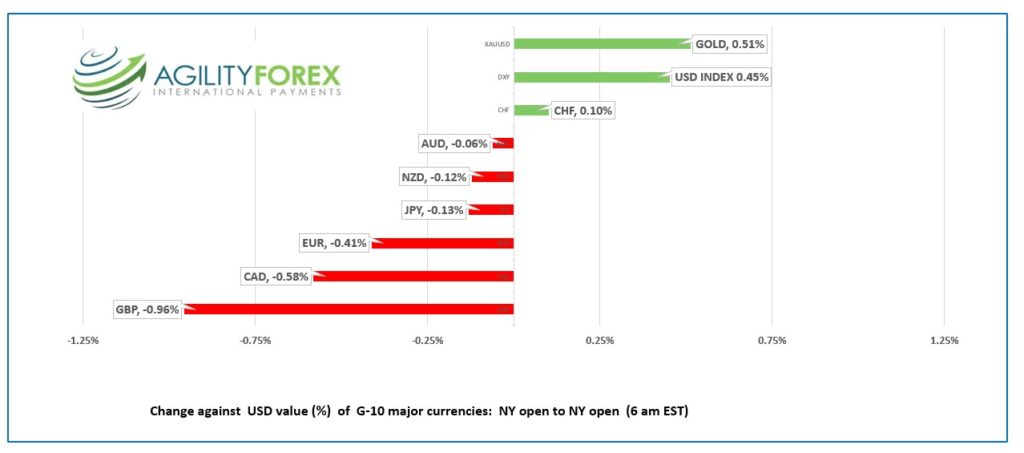

- US dollar rebounds, GBP underperforms.

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3666-70, overnight range 1.3567-1.3670, close 1.3618

USDCAD rallied aggressively yesterday, rising from 1.3503 to 1.3697 by mid-morning and has since consolidated the gains in a 1.3567-1.3683 range. The greenback has recovered a tad over 50% of its losses since last Friday when the latest Fed-Pivot story got legs. Those legs were chopped off at the knee yesterday thanks to better-than-expected US data, Fed-speak, and positioning ahead of Friday’s US employment report.

The US NFP report is expected to show jobs increased by 250,000. A higher-than-expected result should put Fed pivot chatter in a grave. Canada’s employment data is due as well with 20,000 jobs expected, although it will be overshadowed by the NFP data.

The prospect of a Bank of Canada pivot will be in the spotlight today as Governor Tiff Macklem speaks about the “Current economic situation” starting at 11:50 ET (8:50 PT).

USDCAD Technical outlook

The intraday technicals flipped to bullish yesterday with the failure to break support at 1.3500 then breaking through the intraday downtrend line at 1.3590. The subsequent move above 1.3660, suggests a retest of 1.3810 on a move above 1.3710.

The daily chart is bullish shows a double bottom at 1.3500 and an uptrend line from September 15 that comes into play at 1.3530.

For today, USDCAD support is at 1.3630 and 1.3560. Resistance is at 1.3690 and 1.3740. Today’s range: 1.3610-1.3710.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar reasserted itself in the past 24 hours. S&P 500 futures are trading lower, and the US 10-year Treasury yield is see-sawing around 3.77% as traders jockey for position ahead of Friday’s nonfarm payrolls report.

The risk of a lower-than-expected NFP report got a bit of a boost after weekly jobless claims rose 211,000 (forecast 209,000, last week 190,000)

The results flipped the Fed Pivot narrative again after the argument was weakened Wednesday, after the ISM Services and JOLTS employment reports were stronger than expected.

The Fed pivot story is fairy-tale. Chair Powell said as much at the end of August and most Fed policymakers seem to agree.

San Francisco Fed President Mary Daly reiterated the Fed’s commitment to fighting inflation noting that “inflation is problematic” while colleague Raphael Bostic of the Atlanta Fed observed “the overarching message I’m drawing…is that we are still decidedly in the inflationary woods, not out of them.”

Opec confirmed rumours of production cuts when they announced crude production will be reduced by 2.0 million barrel/day beginning November 1. Saudi Energy Minister Prince Abdulaziz said Opec production was well short off quotas’ the actual cut is just 1.0 m/bd.

Goldman Sachs raised its Q4 oil price forecast by $10/b to $110.00. Their oil price forecasts have been wrong all year, so the latest one shouldn’t cause concern.

North Korea fired a couple more missiles overnight and justified the launches as a countermeasure to US and South Korea military drills.

Asian equity markets closed mixed. Japan’s Nikkei 225 gained 0.70%, Hong Kong’s Hang Seng fell 0.42% and Australia’s ASX 200 was unchanged.

European bourses started higher but are modestly lower across the board in early NY trading. WTI oil is down compared to the close, while gold prices inched higher.

EURUSD opened in NY at the bottom of its overnight a 0.9876-0.9926 range before ticking higher post-jobless claims. Renewed US dollar strength ahead of Friday’s NFP data, and soft German and Eurozone data are weighing on the single currency. German Factory Orders fell 2.4% m/m in August (forecast -0.7%) while Euro zone Retail Sales fell 2.0% y/y (forecast -1.7%). The ECB minutes from September * showed policymakers expect inflation to remain above target for an extended period.

GBPUSD traded poorly in 1.1246-1.1381 band, undermined by UK credit downgrade warnings. Fitch ratings agency wrote “The large fiscal stimulus, announced without compensatory measures or an independent evaluation of the macroeconomic and public finances’ impact, and the inconsistency between fiscal and monetary policy stance given strong inflationary pressures, have in Fitch’s view, negatively impacted financial markets’ confidence and the credibility of the policy framework, a key long-standing rating strength.”

USDJPY was adrift, albeit with a modestly bullish bias in a 144.40-144.75 range. Prices were underpinned by the 10-year Treasury yield at 3.76%.

AUDUSD climbed in Asia the dropped from 0.6540 to 0.6458 in early NY trading. NZDUSD underperformed vs AUD, dropping from 0.5812 to 0.5701. The positive sentiment from RBA and RBNZ rate hikes this week has dissipated.

Fed officials, Mester, Evans and Waller are ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: Closed: previous 7.0998

Shanghai Shenzhen CSI 300 closed

NOTE: Chinese markets closed next week for Golden Week.

Chart: USDCNH (offshore) 1 month

Source: Saxo Bank