March 11, 2024

- Trader focus shifts to US CPI on Tuesday.

- Japan avoids technical recession.

- US dollar consolidates post NFP losses.

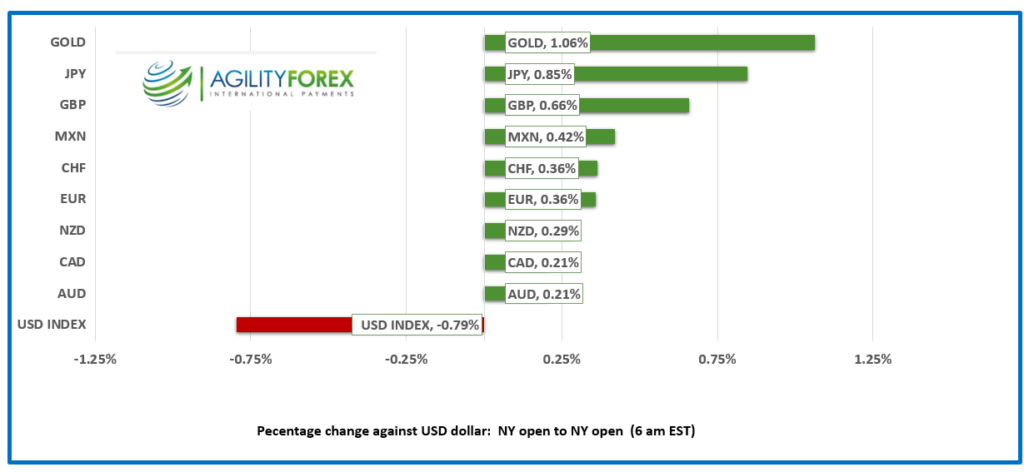

FX at a Glance

Source: IFXA/RP

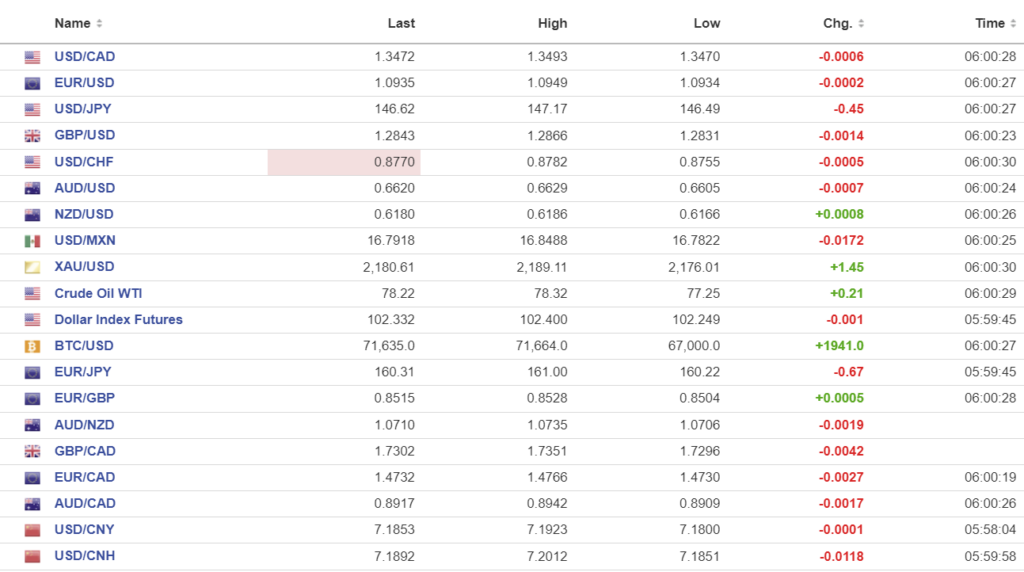

USDCAD Snapshot: open 1.3470-74, overnight range 1.3470-1.3493, close 1.3486

The Canadian employment number was far better than expected but it didn’t fool any economists. Canada is still bringing in far more immigrants than it has jobs for, and attention quickly shifted to the US data.

Friday’s US nonfarm payrolls report indicated that the labour market was rebalancing, which Fed Chair Powell said was necessary before rates could be cut, which fueled US dollar selling. Tuesday’s US inflation data and Thursday’s Retail Sales reports will either keep the US dollar on the defensive or spark a profit taking rally.

WTI oil prices drifted lower in a $77.25-$78.35 range. Traders fear that even with Opec extending production cuts, it won’t be enough to offset weak Chinese demand.

USDCAD Technicals

The USDCAD technical are unchanged. The break of the 2024 uptrend line (1.3520 daily chart) and the move below 1.3490 targets 1.3360, A break above 1.3490-1.3505 suggests further 1.3420-1.3560 consolidation.

However, the failure to extend losses below support in the 1.3410-1.3420 area and the subsequent rally above 1.3460 suggests a slightly bullish bias.

The 100 day (1.3525) and 200 day (1.3480) moving averages will revert to resistance.

For today, USDCAD support is at 1.3430 and 1.3410. Resistance is at 1.3505 and 1.3530. Today’s range is 1.3440-1.3530.

Chart: USDCAD daily

Source: Daily FX

G-10 FX

It will be a very quiet trading session do to a lack of data and the shift to daylight saving time.

Friday’s US nonfarm payrolls data appeared robust, but significant revisions suggested otherwise. Analysts believe the data is moving in the right direction, yet not sufficiently for the Fed to commence rate cuts soon. Attention is now on Tuesday’s US Core Inflation report, with forecasts at 0.3% versus the previous 0.4% month-over-month, indicating today’s trading session might be subdued.

The Middle Eastern front is far from calm. Efforts to negotiate a ceasefire for Ramadan faltered, partly due to Hamas’s attack on Israeli women and children during the Jewish holiday of Shmini Atzeret. The adage “What’s good for the goose is good for the gander” seems applicable here. Traders seem more focused on domestic politics than geopolitical events, particularly regarding the next US presidential occupant.

Global equity indexes are in the red. Australia’s ASX 200 index fell1.82% while Japan’s Nikkei 225 index lost 2.19%. European bourses are in negative territory with a 0.68% drop in the German DAX leading the others lower. SP 500 futures are down 0.42%. The US 10-year Treasury yield is steady at 4.08%.

EURUSD is steady in 1.0933-1.0949 range, with prices supported by the dovish Fed outlook. ECB policymakers appear to be favouring a June rate cut as indicated by Governing council member Peter Kazmir. He said “Only in June, with new forecast at hand, will the level of confidence reach the threshold.”

GBP/USD is trading quietly in a 1.2831-1.2866 band with markets awaiting Tuesday UK employment data. Analysts are focused on the wage component for clues as to the timing of a BoE rate cut.

USD/JPY is trading with a negative bias in a 146.49-148.17 range do to rising concerns that the BoJ is on the verge on ending its negative rates policy. Japan Q4 GDP was a better than the previous result but below expectations (actual Q4 GDP 0.1% vs forecast 0.3%, previous -0.1%). The result support calls for an April rate hike.

AUD/USD traded in a 0.6605-0.6629 range. Activity was muted partly because Australian markets were closed for a holiday and because of caution ahead of Tuesday’s US inflation numbers.

USDMXN oscillated within a 16.7822-16.84488 range after falling from 16.8816 just before the US employment report. Analysts anticipate a rate cut by Banxico on March 21.

There are no notable US or Canadian economic data releases today.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0969 vs exp. 7.1869 (prev. 7.0978.

Shanghai Shenzhen CSI 300 rose 1.25% to 3589.26.

February CPI rose 0.7% y/y (forecast 0.3%, January -0.8%), monthly CPI rose 1% (forecast 0.7%)

February PPI fell-2.7% y/y (forecast -2.5%, previous -2.5%).

Chart: USDCNY and USDCNH daily

Source: Investing.com