Source: Pixabay

- Hawkish ECB comments underpin Euro

- Global equity indexes higher and ignore US 10-year Treasury yield

- US dollar consolidating yesterday’s losses

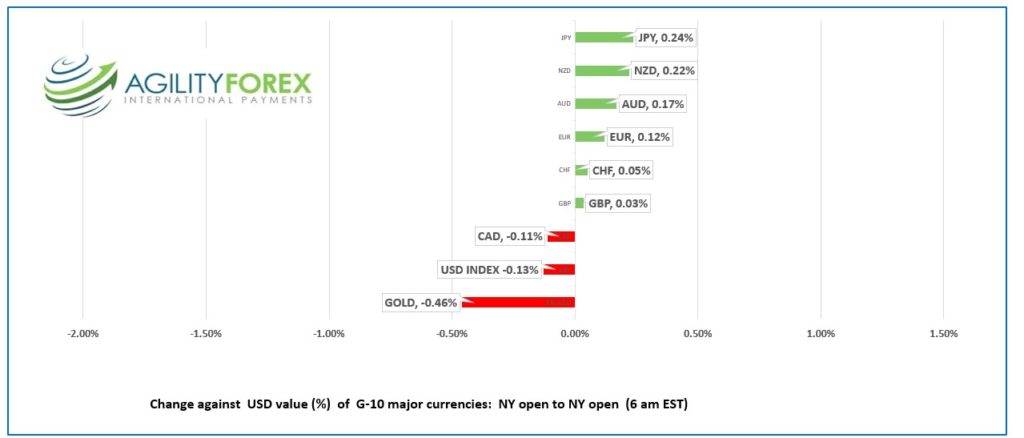

FX at a glance:

Source: IFXA Ltd/RP

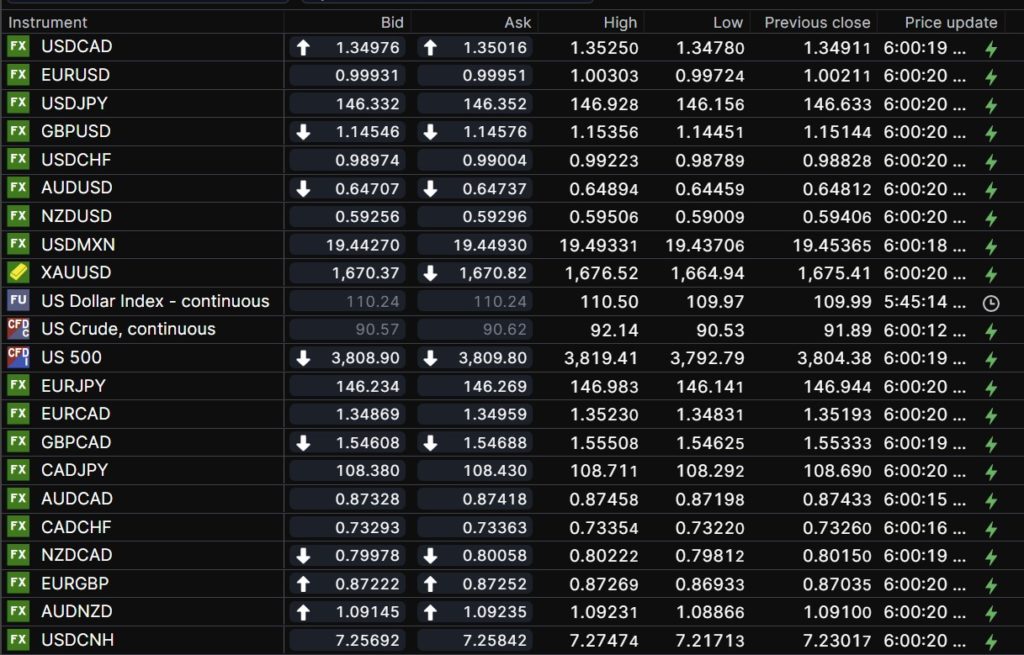

USDCAD Snapshot: open 1.3498-02, overnight range 1.3478-1.3525, close 1.3491

USDCAD continues to drift with the prevailing US sentiment and this morning that sentiment is slightly positive.

Traders are hoping that Biden administration loses control of the House, which would essentially put a stop to major legislation getting passed. Then the focus will shift to the 2024 election and the likely return of Donnie Trump.

WTI oil prices are consolidated recent gains in a $90.42-$92.14/barrel range. Prices are supported by persistent hopes that China plans to ease covid restrictions which will boost demand in the face of Russian oil sanctions and Opec production cuts. However, fears of slowing global growth are capping gains.

BoC Governor speaks Thursday about “The Evolution of Canadian Labour Markets.”

USDCAD Technical outlook

The intraday USDCAD technicals are unchanged from yesterday with a minor downtrend line at 1.3530 guiding prices lower towards support in the 1.3440-50 area. A break above 1.3530 targets 1.3580, then 1.3650. A break below 1.3440 gets interesting as it suggests steep losses to 1.3230 on a daily chart.

For today, USDCAD support is at 1.3440 and 1.3380. Resistance is at 1.3530 and 1.3580. Today’s range 1.3440-1.3540.

Chart: USDCAD hourly

Source: Saxo Bank

G-10 FX recap and outlook

It’s mid-term election day in America and global markets are taking a break to watch. In some states, the view will be closer to the trailer for Call of Duty, Modern Warfare complete with masked, armed guards in tactical gear, rather than voting day in the world’s most powerful democracy. “Vote for my candidate, or I will shoot you.”

Markets are anticipating that Republicans regain control of the House of Representatives and according to a WSJ article, “the S&P 500 since 1970 has returned 0.4% on average the day of midterm elections, according to Dow Jones Market Data. The index has ended the Election Day trading session higher 69% of the time during the past 13 midterms.”

That sentiment propelled the S&P 500 index 0.96% higher yesterday and boosted S&P futures by 0.20% overnight. Traders conveniently ignored the surge in the US 10-year yield from 3.93% November 1 to 4.207% this morning, perhaps in the belief that US rates are very close to their peak. They may get a rude awakening with October inflation report on Thursday.

EURUSD retreated modestly overnight, falling from 1.0030 to 0.9972 before climbing to 1.0000 in NY. ECB policymaker Luis de Guindos said rates will continue to rise and quantitative tightening will be discussed in December. Eurozone retail sales were better than expected, only falling 0.6% m/m instead of 1.3% as forecast. The intraday EURUSD technicals are bullish above 0.9950 looking for a break above 1.0090 to target 1.0200.

GBPUSD traded with a negative bias in a 1.1445-1.1536 range and is close to the session low in NY. BoE Chief Economist Huw Pill said policymakers are “not inflation nutters,” but need to control the surge in prices to stop the spread in inflation. Others would suggest that being “inflation nutters” is why they exist.

USDJPY traded in a 146.16-146.92 band, peaking in Asia, and finding the floor in NY. Bloomberg reports that Japan’s holdings of foreign securities fell $43.9 billion in October, which is almost exactly what the Ministry of Finance spend on FX intervention.

AUDUSD dipsy-doodled in a 0.6446-.06489 range. Price rose, the fell in Asia then rebounded from the overnight low to the NY close. The slide was triggered by weak consumer sentiment and business confidence reports, which supports the RBA view of a slower pace of rate hikes.

NZDUSD traded in a 0.5901-0.5951 range. The RBNZ quarterly Survey of Expectations showed that expectations for inflation in two years time, rose to 3.62% from 3.07% three months earlier. The RBNZ inflation target is 2.0%. Westpac Bank economists are predicting a 75 bp hike in the OCR on November 23.

FX trading may be choppy but rangebound with the election sidelining many traders. Essentially, it’s a nothing day.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

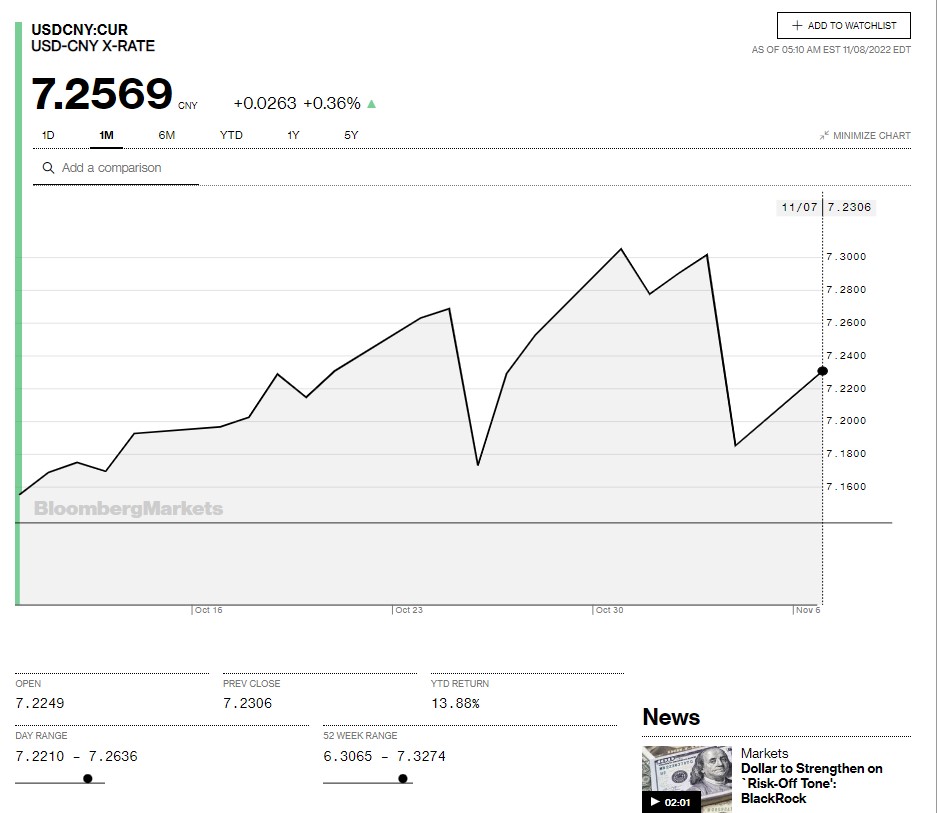

China Snapshot

Today’s Bank of China Fix: 7.2150, previous 7.2292

Shanghai Shenzhen CSI 300 fell 0.69% to 3749.33

China’s Guangzhou area experienced a rise in Covid cases and nationally the number of new Covid cases rose to 7,475 from 5,496 one day earlier. For Xi Jinping, the rise means he will not allow an early end to strict covid protocols.

The German Economic Ministry recommended to cabinet that China’s planned takeover of chip manufacturer Elmo’s should be blocked.

Chart: USDCNY 1 month

Source: Saxo Bank