Source: Disney world

- China reaffirms strict Covid policy

- Traders on edge ahead of US Mid-term elections and CPI

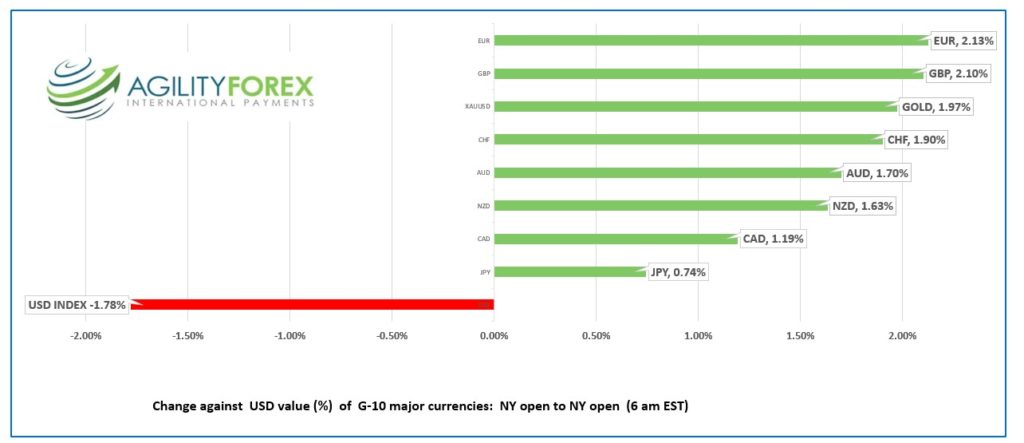

- US dollar down sharply from Friday open on improved risk sentiment

FX at a glance:

Source: IFXA Ltd/RP

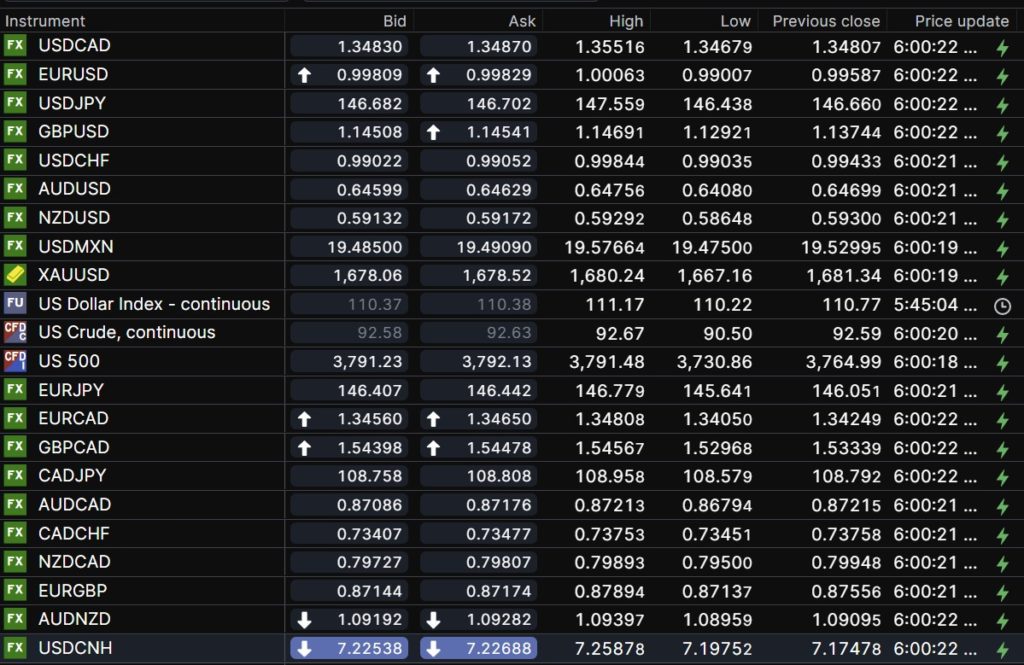

USDCAD Snapshot: open 1.3483-87, overnight range 1.3467-1.3552, close 1.3481

USDCAD got sideswiped by plunging antipodean currencies at the Asia open after a Chinese official denied Covid policies were easing. The rally reversed itself in Europe and USDCAD is consolidating its losses from Friday.

USDCAD is being pressure by both higher WTI oil prices and narrowing CAD/US 10-year yield differentials following Friday’s Canadian and US employment data. Canada gained 108,300 jobs in September (forecast 10,000) while US NFP rose 261,000 (forecast 200,000).

Traders decided that the US numbers were not sufficient to force the Fed to raise rates by 75 bps in December. The Canadian data suggests the Canadian economy is stronger than expected.

WTI oil shrugged off most of Asia losses and traded in a $90.50-$92.67/b range. Traders are anticipating that China will eventually reopen, and that demand will increase, especially due to the onset of winter in the Northern hemisphere.

USDCAD trading may be extra-choppy ahead of the US elections.

USDCAD Technical outlook

The intraday USDCAD technicals turned bearish Friday with the move below 1.3680 followed by the breach of support at below 1.3580. A minor downtrend line at 1.3580 is guarded by resistance at 1.3550. Prices are trading just above the uptrend line from August and previous support at 1.3450. A decisive break below 1.3450 targets 1.3210.

For today, USDCAD support is at 1.3440 and 1.3380. Resistance is at 1.3510 and 1.3560. Today’s range 1.3460-1.3560.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Mr Toads Wild Ride is anything but, when compared to overnight markets. The US dollar rose and sank, bonds dropped, and equity markets flip-flopped after traders re-evaluated their outlooks.

Friday, traders decided that the US nonfarm payrolls report was mixed (NFP rose 261,000, forecast 200,000, unemployment rate 3.7% vs 3.5% in September) and that the rumours that China would ease its strict Covid protocols were true. The US dollar plunged, Wall Street equities rallied, and the S&P 500 index finished 1.36% higher. Bond traders were more subdued. The US 10-year yield traded in a 4.142-4.205% range Friday morning then settled around 4.15% for the rest of the day.

Things looked a tad different in the early Asia hours. Saturday, a spokesman from China’s National Administration of Disease Control and Prevention reaffirmed not change to China’s Covid policies. He said” Practice has proved that our pandemic prevention and control policy and a series of strategic measures are completely correct, and the most economical and effective.”

The US dollar gapped higher and equity markets plunged. Europeans were wearing rose-coloured glasses when they entered the fray. They decided things were looking up. Thy determined that the Fed will raise rates less aggressively, the ECB will be more aggressive then expected, and that China’s Covid policies are likely to become less restrictive in the future.

European bourses are trading with a mixed tone. The German Dax is up 0.85% thanks to better-than-expected German Industrial Production data while the UK FTSE 100 is 0.19% lower. S&P 500 futures are up 0.57% while DJIA futures have gained 0.53%. Gold is trading at $1,680.10, up 0.20% from Friday’s close while the US 10-year Treasury yield sits at 4.138%.

There are two major events for markets this week-US elections and inflation. Tuesday’s US midterm vote will start roiling markets in Asia and European markets on Wednesday. A divided Congress is seen as good for equities as policymakers cannot accomplish much to screw up markets. If so, the US dollar should retreat and equities rally, and some of that view is reflected in today’s trading.

Thursday, US October CPI is expected at 8.0% y/y while Core inflation is forecast at 6.5% y/y.

EURUSD gapped lower at the Asia open then rallied from 0.9901 to 1.0006 before easing in early NY trading. Improved risk sentiment, the prospect of more aggressive ECB rate hikes, and German Industrial production rising 2.6% compared to the forecast of a 0.5% gain supported the rally. The EURUSD technicals are bullish above 0.9750 looking for a break above 1.0090 to target 1.0210.

GBPUSD soared from a low of 1.1292 to 1.1476 before easing to 1.1446 in NY. The currency pair is almost fully recovered from the surprisingly dovish Bank of England monetary policy meeting last week and its negative economic outlook. The intraday GBPUSD technicals are bullish above 1.1290 looking for a break above 1.1480 to target 1.1570.

USDJPY is trading near the bottom of its 146.44-147.56 range due to broad US dollar weakness. News the BoJ offered to buy an unlimited amount of 5- and 10-year JGB’s and the fear of USDJPY intervention weighed on the currency pair.

AUDUSD gapped lower in Asia, opening at 0.6407 after closing at 0.6470 in NY on Friday. The sell-off was due to news China did not plan to ease its Covid policy anytime soon. Goldman Sachs upgraded their RBA Cash rate forecast to 4.1% from 3.6%.

NZDUSD mirrored AUDUSD moves and traded in a 0.5865-0.5929 band.

There are no US economic reports today but there are plenty of Fed speakers. (Collins, Barker, and Mester).

FX open, high, low, previous close as of 6:00 am ET4.205%

Source: Saxo Bank

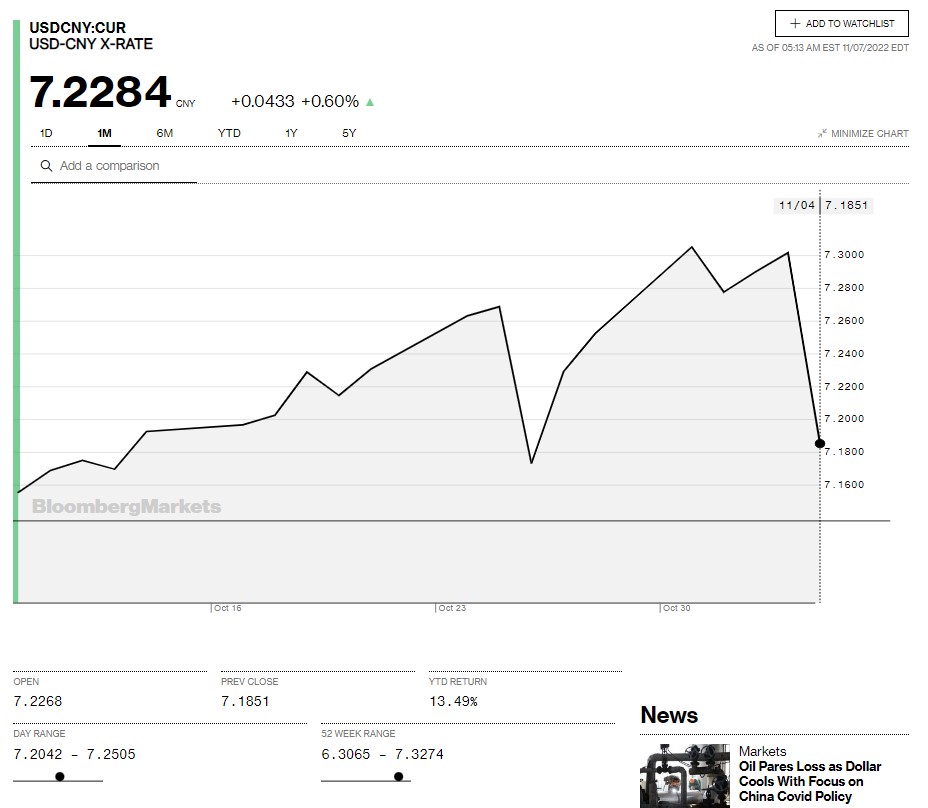

China Snapshot

Today’s Bank of China Fix: 7.2292, previous 7.2555

Shanghai Shenzhen CSI 300 rose 0.22% to 3775.30

October Trade Surplus widened to $85.15 b vs Sept 84.74 b-Forecast $95.95 b.

Chart: USDCNY 1 month

Source: Saxo Bank