May 1, 2024

- Hawkish outcome for FOMC expected.

- BoC Governor Macklem in from of Senate Standing Committee

- USD opens firm after quiet overnight session.

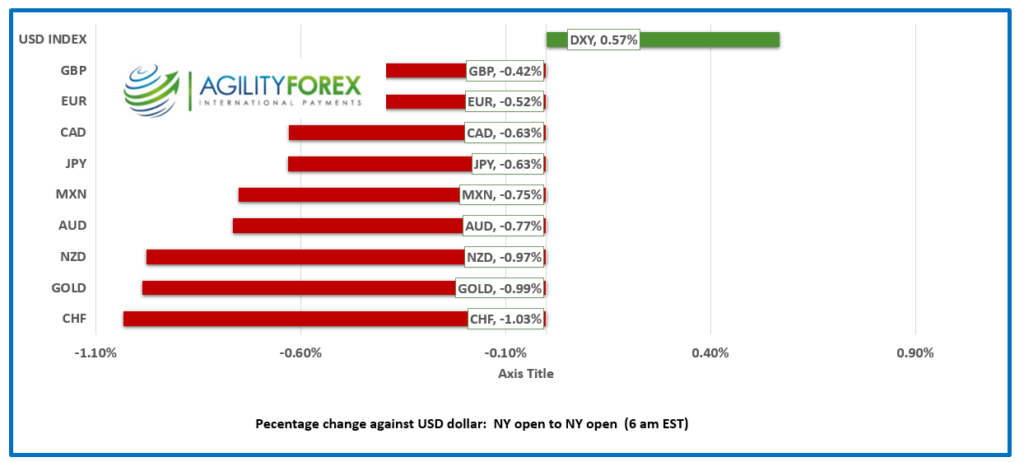

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3773, overnight range 1.3767-1.3784, close 1.3780.

USDCAD rallied in the wake of yesterday’s higher than expected US employment cost Index. The data suggested that the road to lower inflation was littered with speed bumps and would limit the number and size of Fed rate cuts in 2024. It was a broad-based US dollar rally which sank all the major G-10 currencies except for the Japanese yen.

USDCAD gains were also supported by March GDP data, which showed Canadian economic growth slowing, which may encourage the Bank of Canada to cut interest rates. We may hear more on that subject today when Governor Tiff Macklem testifies to the Senate Banking Committee at 2:15 pm EDT today.

Oil prices slumped on the heels of the surging US dollar. WTI dropped from 84.45 last Friday to 80.36 overnight. It’s a good day for oil producers in Canada; the Trans Mountain pipeline extension opens today and it will ship an additional 590,000 b/d from Alberta to the Pacific Coast. The pipeline is expected to shrink or even eliminate the discount on Western Canada Select (WCS) to WTI

USDCAD Technicals

The intraday USDCAD technicals are bullish following the break above 1.3740 yesterday and are looking for a move above 1.3790 to extend gains to 1.3860. A move below 1.3740 suggests a retest of support in the 1.3660 area.

USDCAD snapped a two-week downtrend with the break above 1.3680 yesterday and the subsequent rally above 1.3740 suggests further gains to 1.3850.

For today, USDCAD support is at 1.3730 and 1.3680. Resistance is at 1.3790 and 1.3850. Today range is 1.3730-1.3830.

Chart: USDCAD 1 day

Source: Investing.com

May Day-Fed Day

Markets are closed in many countries around the world for May Day or Labor Day celebrations. The US, Canada, and the UK are not among them. It is also Fed Day. Traders are bracing themselves for Fed Chair Powell to deliver a hawkish assessment for US interest rates after a spate of inflation reports suggested the downtrend in prices had stalled and looked to be reversing.

ADP and Jolts.

ADP employment rose by 192,000 compared to the forecast for a gain of 175,000. The Fed will be more interest in pay gains and ADP said “Pay gains for job-changers slowed in April Year-over-year pay gains for job-stayers were little changed in April at 5 percent. Pay growth for job[1]changers fell from 10.1 percent in March to 9.3 percent but remains higher than it was at the beginning of the year.

The Job Openings Labour Turnover Survey (JOLTS) is expected to show a drop to 8.69 million from 8.756 million last month. In addition, the ISM manufacturing PMI data is expected to dip to 50 from 50.3, and ISM Manufacturing Prices Paid drop to 55 from 55.8. All of the above suggests the FOMC will stick to their “wait and see” stance on interest rates.

EURUSD

EURUSD traded defensively in a 1.0649-1.0674 range. Volumes were very light as the major European markets were closed for Labor Day. The focus is on the Fed meeting today and a hawkish outcome will drive EURUSD to 1.0600.

GBPUSD

GBPUSD traded in a 1.2466-1.2500 range and is trading at 1.2485 in early NY. Soft April manufacturing PMI (actual 49.1) is also weighing on the currency pair. S&P Global wrote, “The UK manufacturing sector suffered a renewed downturn in April, as output and new orders contracted following short-lived rebounds in March. The sector is still besieged by weak market confidence, client destocking, and disruptions caused by the ongoing Red Sea crisis.”

USDJPY

USDJPY continued to grind higher as prices slowly recover from what in all likelihood was BoJ intervention on April 29. Analysts are suggesting that the BoJ sold around 35 billion USDJPY. Rising US Treasury yields (10-year Treasury yield 4.69%) and a softer Manufacturing PMI report (actual 49.6, vs. previous 49.9) are fueling the overnight gains, which are also supported by expectations for a hawkish FOMC outcome today.

AUDUSD and NZDUSD

AUDUSD consolidated Tuesday’s losses in a 0.6465-0.6482 range, weighed down by robust US ECI data and a tepid Australian retail sales report. Judo Bank Manufacturing PMI (actual 49.6, forecast 49.9, March 49.9) S&P Global wrote, “Manufacturing activity improved sharply in April after a sustained period of cyclical weakness.”

NZDUSD drifted in a narrow 0.5875-0.5897 range following Tuesday’s post-US ECI losses. With the New Zealand labour report barely moving the needle. Q1 employment growth (-0.2 vs. forecast 0.3), unemployment rate 4.3% (forecast 4.2%).

USDMXN-Markets closed

USDMXN rallied Tuesday, and with Mexican markets close, prices traded narrowly in 17.0699-17.1670 range. Mexican Q1 GDP rose 1.6% y/y vs. 2.5% y/y previously. Some analysts suggest that despite the slowing growth, other recent data gives Banxico room to delay future rate cuts.

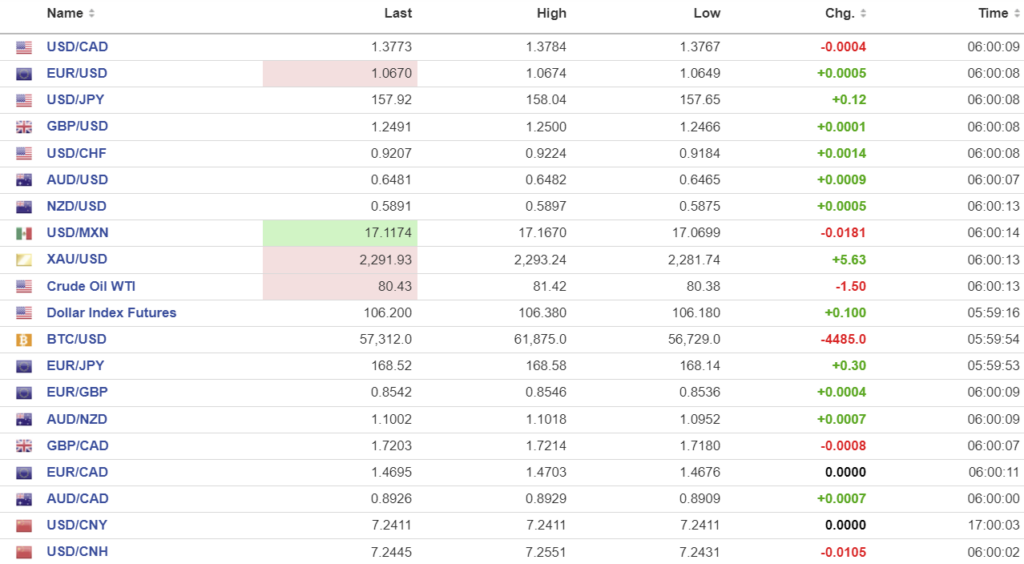

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

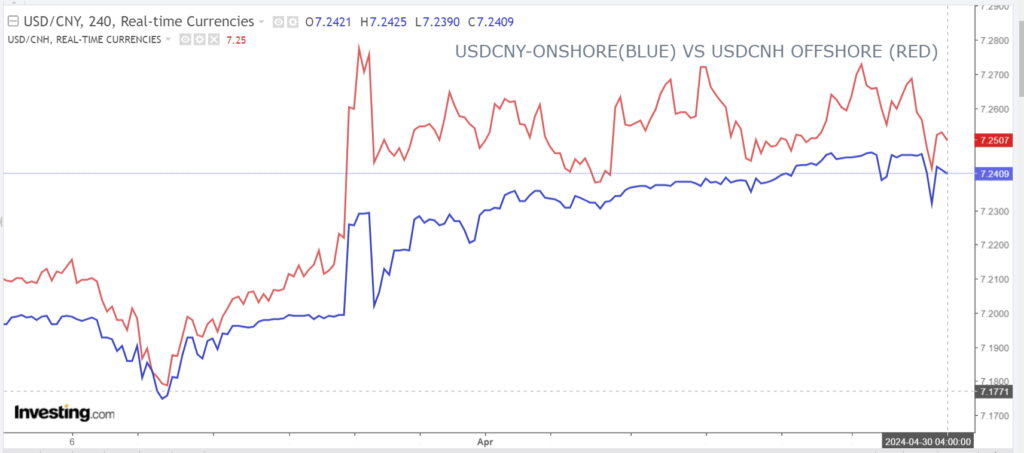

China Snapshot`

PBoC fix: 7.1063 (prev. 7.1066)

Chinese markets closed.

Shanghai Shenzhen CSI 300 fell 0.54% to 3604.39.

Chart: USDCNY and USDCNH 4 hour-as of April 30

Source: Investing.com