Photo: Clipartmag.com

April 28, 2023

- JP Morgan takes over First Republic Bank.

- European and UK markets closed for May Day.

- US dollar consolidating Friday’s losses and opens firmer in quiet trading.

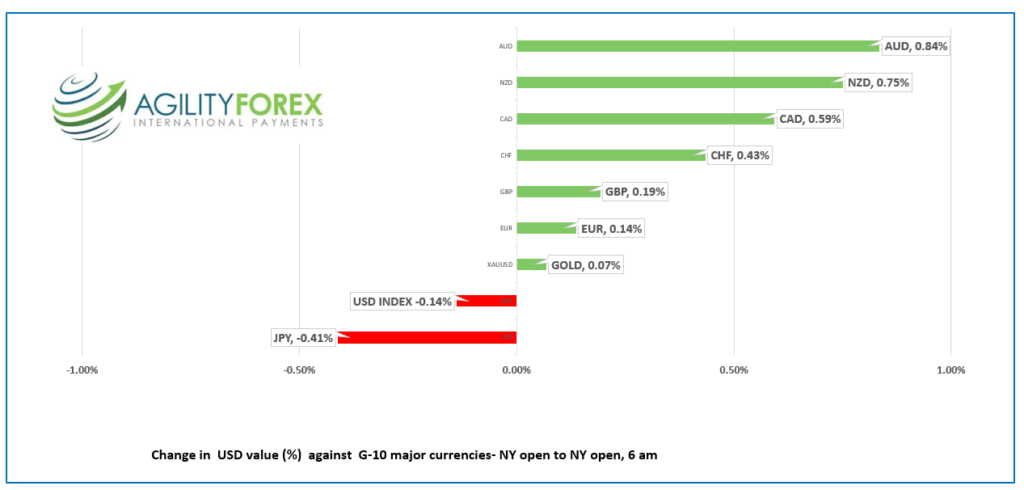

FX at a glance

Source: IFXA Ltd/RP

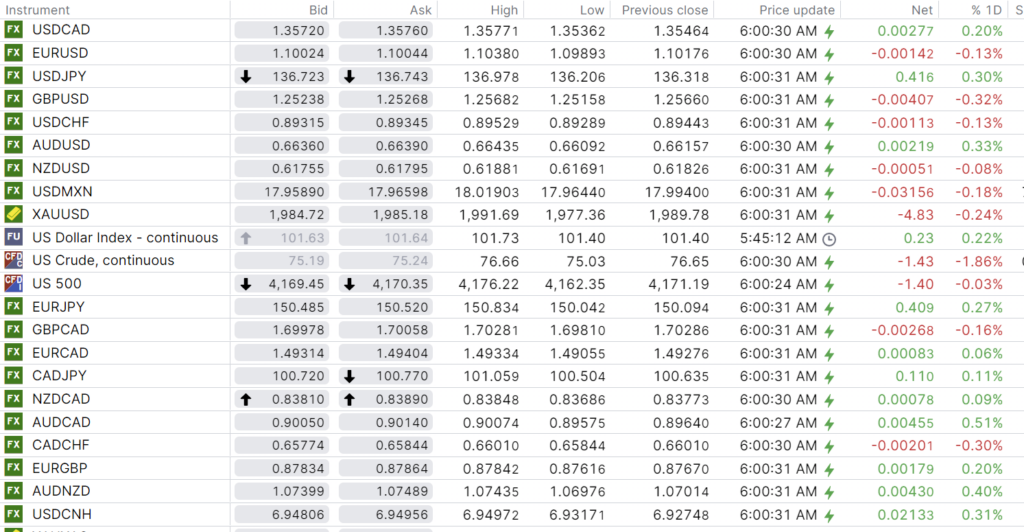

USDCAD Snapshot: open 1.3572-76, overnight range 1.3536-1.3577, close 1.3546

USDCAD threatened to break above major resistance in the 1.3660 area on Friday, but instead dropped sharply after risk sentiment turned positive. The S&P 500 index rallied, and the US dollar retreated against the G-10 majors, taking USDCAD along for the rise.

USDCAD is also retreating on hopes the Fed pauses after the next rate hike, which erodes the CAD/US interest rate differential.

The PSAC strike ended after the government agreed to a 12.6% wage bump, and a $2,500 pension lump sum payment which may aggravate BoC worries about a wage-spiral inflation spike.

Oil prices have erased most of Friday’s gains and dropped from $76.66/b to $74.98/b in NY. Ongoing global growth concerns, technical selling, and China’s weaker than expected manufacturing PMI weighed on prices.

There are no Canadian data releases of note today.

USDCAD Technical Outlook

The USDCAD technicals flipped to bearish Friday. The USDCAD topside break didn’t last, and the subsequent retreat snapped the two-week uptrend line at 1.3560 but halted before testing support in the 1.3510 area.

The subsequent bounce back above 1.3560 implies a bit of 1.3510-1.3610 consolidation until the FOMC meeting.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3580 and 1.3610

Today’s range 1.3530-1.3610

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

JP Morgan answered the “Mayday” call from First Republic Bank. Actually, the call came from bank regulators who asked “will someone take this mess off our hands? We will make it worth your while.” And like a shark to chum, JPM raced in.

Morgan takes all of FRB’s deposits and loan, is buying most of the banks assets including $173 billion in loans. JPM gets $50 billion in funding from FDIC and the same agency will share losses. Sweet deal.

Most major European markets and those in the UK were closed for May Day.

The focus is on Wednesday’s FOMC meeting with the universally expected 25 bp rate bump expect to be the final hike for this cycle. The Fed is the headliner, but the bill includes the ECB, and the RBA.

EURUSD traded in a 1.0989-1.1038 range overnight. Prices are supported hopes for a dovish FOMC and hawkish ECB monetary policy meetings. Softer than expected Eurozone area inflation data has sparked a debate about the need for a 25 bps or 50 bp rate increases.

GBPUSD drifted in a 1.2516-1.2568 range with prices reacting to the prevailing risk sentiment. The UK is closed for May Day and traders may soon be distracted by the upcoming King Charles coronation.

USDJPY rose in a 136.21-136.98 band and is still in demand following the dovish Bank of Japan monetary policy meeting which suggested Japanese rates will be lower for longer.

AUDUSD climbed from 0.6609 to 0.6944 on speculation of a dovish FOMC meeting. Traders are looking ahead to tomorrow after the recent weaker than expected Australian inflation data led to new forecasts that the RBA will leave rates unchanged.

NZDUSD traded narrowly in a 0.6169-0.6188 range. The RBNZ financial stability report and employment data are due Tuesday.

US ISM Manufacturing PMI and Construction Spending data are ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

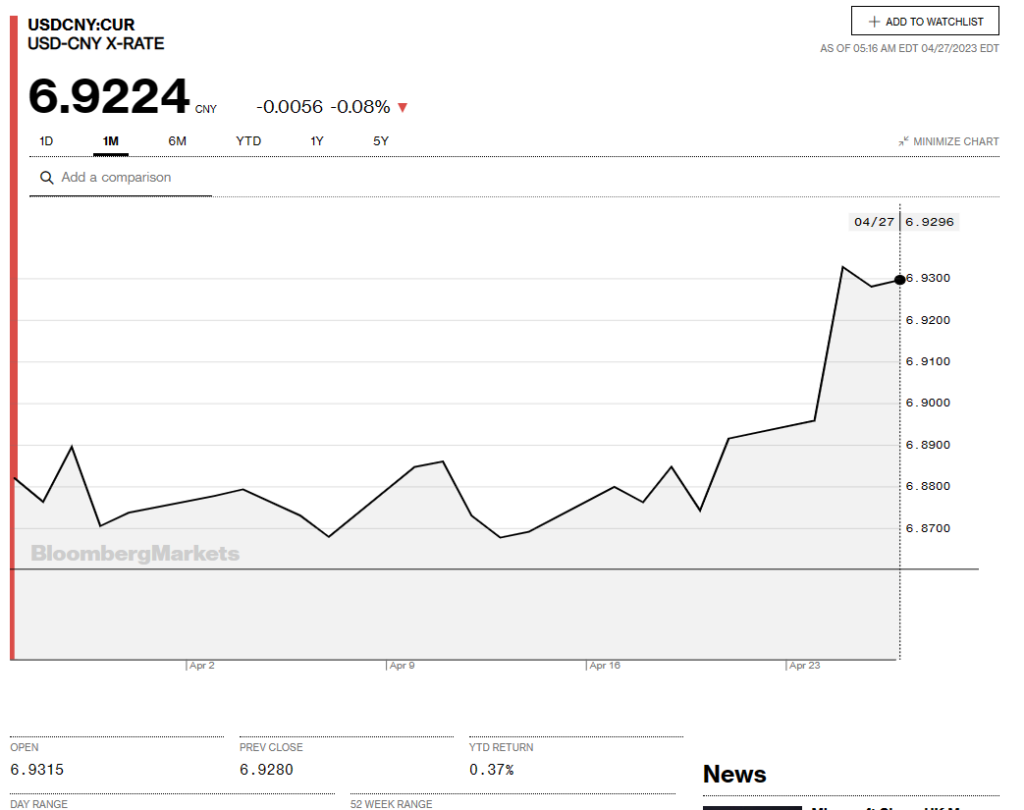

China Snapshot

Bank of China Fix: 6.9240, closed.

Shanghai Shenzhen CSI 300 closed: 4029.09.

China on National holiday from May 1-3.

NBS April Manufacturing PMI 49.2, forecast 51.4, March 51.9)

Non-Manufacturing PMI 56.4, forecast 50.4, March 58.2

Chart: USDCNY 1 month

Source: Bloomberg