January 18, 2024

- Middle East tensions are escalating,

- Weekly jobless claims fall by 13,000.

- US dollar opens mixed and consolidates yesterdays gains.

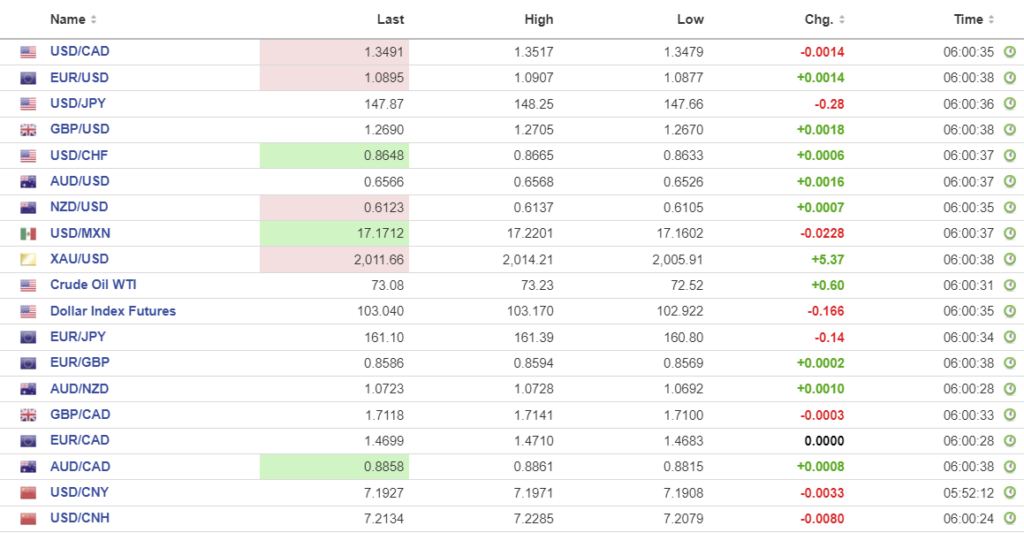

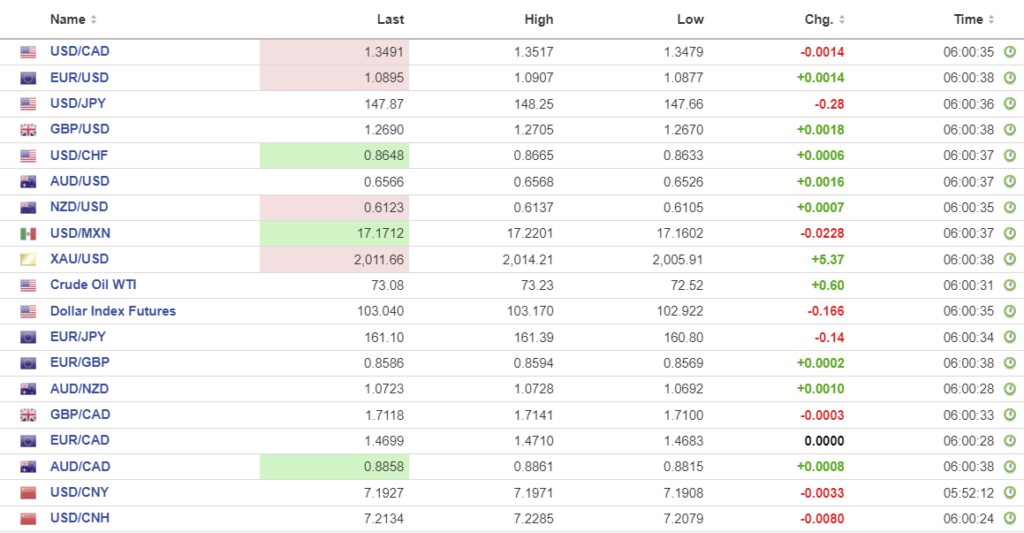

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3489-93, overnight range 1.3479-1.3526, close 1.3505.

USDCAD rallied to 1.3544 yesterday on the heels of robust US retail sales data. The report underscored the resilience of the US economy and put a damper of Fed rate cut expectations. Traders may see more of the same today when US weekly jobless claims, and housing data is released. If the data is robust the US dollar will catch another bid and lift USDCAD in the process.

USDCAD gains were slowed by rising oil prices after more Middle East countries fired missiles at each other. The Opec monthly oil report and the International Energy Agency (IEA) are predicting strong growth in demand for 2024 which has underpinned WTI prices. WTI traded higher in a $72.52-$73.39 range.

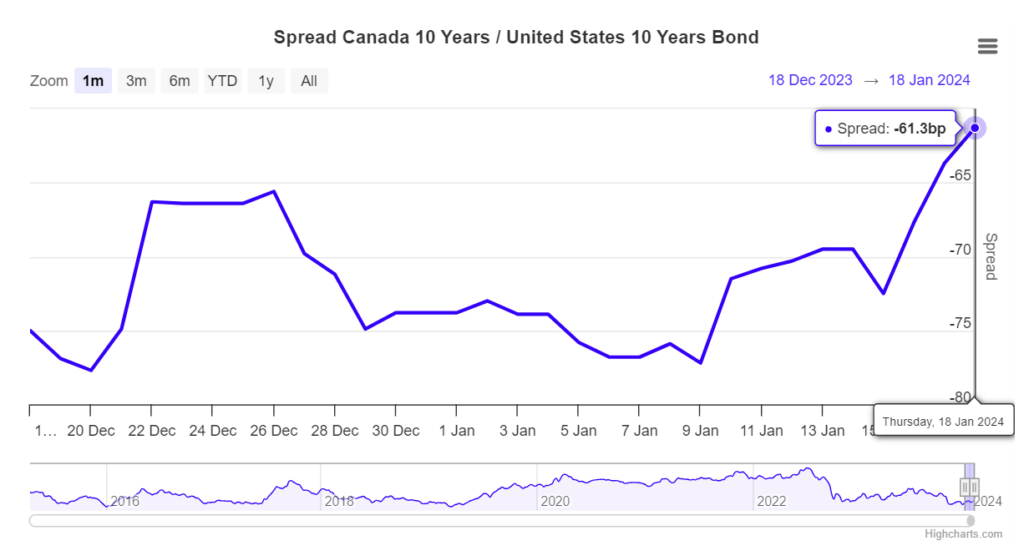

USDCAD is also supported by widening CAD/US 10 year interest rate differentials which favour the US dollar.

Source. Worldgovernmentbonds.com

USDCAD Technicals:

The intraday USDCAD technicals are mildly bearish after the move below 1.3505 on an hourly chart snapped this weeks uptrend. A break below 1.3470 targets 1.3430. The four hour chart shows the January uptrend alive and well while prices are above 1.3380.

Longer term, USDCAD needs to decisively breach the 1.3535 area which is the 50% Fibonacci retracement level of the November-January range of 1.3175-1.3890. Overbought RSI studies suggest that prices will consolidate in a 1.3440-1.3550 range.

For today, USDCAD support is at 1.3470 and 1.3440. Resistance is at 1.3550 and 1.3590. Todays range 1.3460-1.3550

Chart: USDCAD daily

Source: DailyFX

G-10 FX recap

Today’s weekly jobless claims data proved to be another nail in the coffin for early rate Fed rate cuts. Weekly jobless claims dropped by 13,000 which gives the Fed more reason to leaves steady for longer. Bond traders agreed and lifted the US 10-year Treasury yield to 4.11% from 4.08%, pre-data. Equity traders have a different view. S&P 500 futures rose 0.40% perhaps because they see the direction for interest rates as being more important than the timing of a cut.

The fear that the Israel/Hamas war would suck other nations into the conflict is becoming a reality. Iran’s Supreme Leader Ali Khamenei’s is rabidly anti-Israel and is actively funding numerous terrorist groups in the region. Actions from those groups has led to Jordan firing missiles into Syria, Pakistan retaliating against Iran after Khamenei’s troops fired missiles into Pakistan, and the US and UK bombing Yemen. The winds of war are now a category 1 storm.

Financial markets are mostly ignoring the Middle East developments and are more concerned about Fed monetary policy than bombings in Baghdad and the like. And on that note, Fed policymakers are suggesting rates will go longer but not soon and not quickly.

EURUSD traded in a 1.0877-1.0907 range., then dropped to 1.0853 after the US data. The “steady for longer” US rate theme is weighing on prices.

GBPUSD dropped from 1.2705 to 1.2651 after today’s weekly jobless claims news reinforced the robust US economic growth story.

USDJPY traded defensively overnight, but the US data has it back at the top of its 147.66-148.25 range. The rebound in the 10-year Treasury yield to yesterday’s 4.12% level fueled the move. Japan November Industrial Production fell 1.4% (previous 5.3% y/y) and Capacity Utilization was 0.3% compared to 1.5% in October.

AUDUSD traded in a 0.6526-0.6565 range weighed down by a soft employment report. Australia lost 65,100 (s.a.) jobs in December (forecast 17,600, November 72,600) and that took another rate hike off the table while raising the odds for a rate cut in the second half of 2024.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

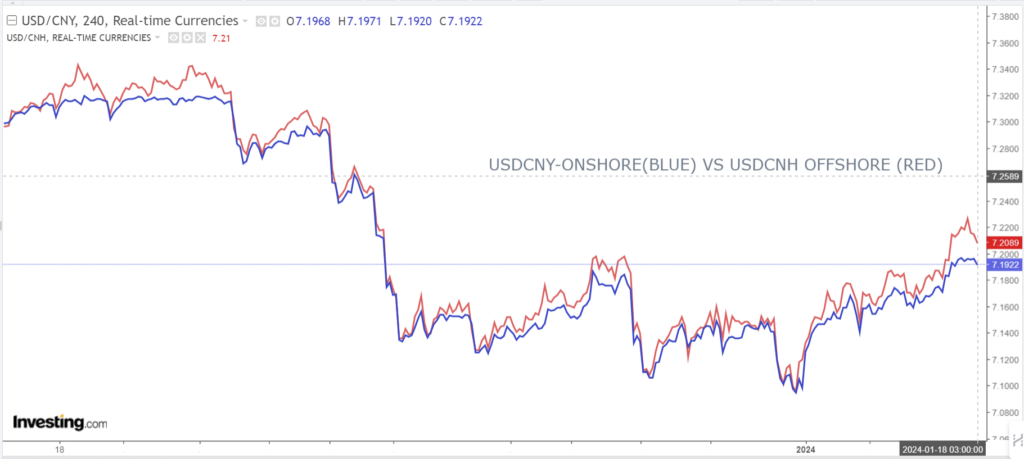

China Snapshot

PBoC fix: today 7.1174, expected 7.1976, previous 7.1168.

Shanghai Shenzhen CSI 300 rose 1.41% to 3274.73.

Are Chinese authorities intervening in equity markets? A Bloomberg article suggests that is the case. A surge in some major exchange traded funds suggests the guiding hand of Beijing.

US and Chinese Treasury officials are meeting in Beijing.

Chart: USDCNY and USDCNH 4hour

Source: Investing.com