Source: Pixabay

- China makes tiny cuts to 1 and 5 year Lending rate

- S&P 500 futures clawing back losses as Treasury yields slip

- US opens mixed after subdued overnight session

FX at a Glance

Source: IFXA Ltd/RP

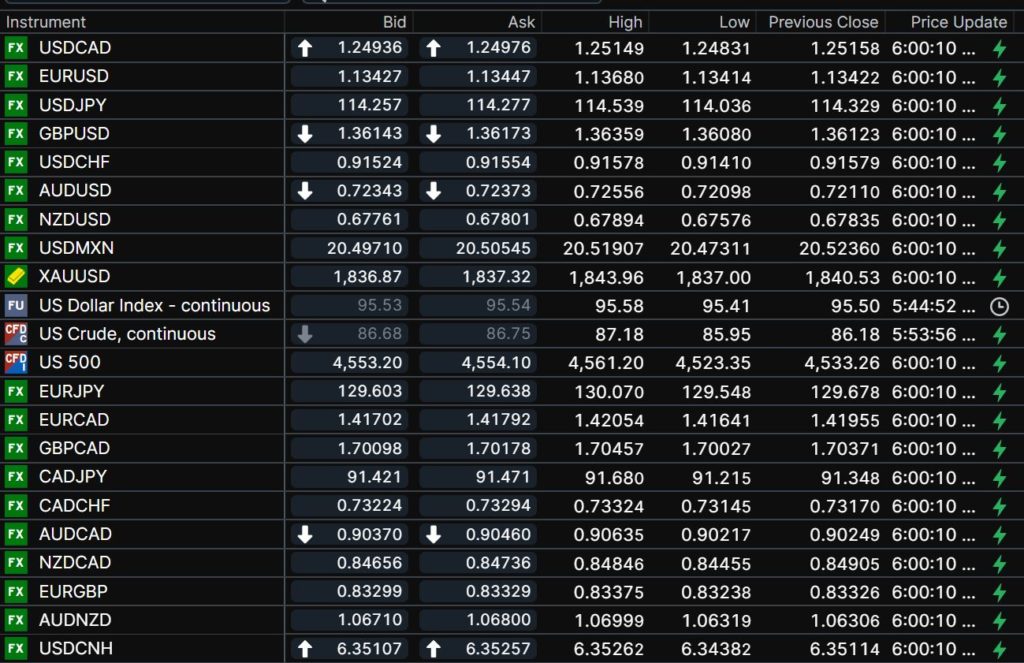

USDCAD Snapshot: Open 1.2494-98, Overnight Range-1.2483-1.2515, previous close 1.2516

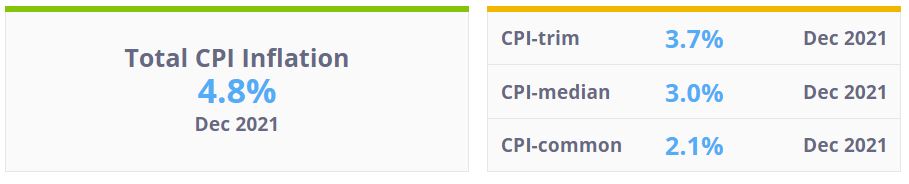

USDCAD is dancing to the WTI/S&P 500 tune. Domestic news and data are mostly background noise as evidenced by yesterday’s inflation report. Canada CPI rose at the fastest pace in 30 years, rising 4.8% y/y in December, a tick above the 4.7% forecast. The result was largely expected but because core measures are grinding higher, the Bank of Canada may raise rates next week.

USDCAD rallied on the news as many traders had sold the currency pair in anticipation of a sharply higher CPI result and were forced to cover. That rally stalled at 1.2515 because oil prices rallied, with WTI Rising to $87.81 from $85.81/barrel.

The Opec Monthly Oil Report was upbeat and stayed with its earlier prediction of robust oil demand in 2022. They admitted that although the risks from Omicron were not something to sneeze at, supply constraints have underpinned prices. WTI consolidated yesterday’s gains overnight.

It is the same story today. USDCAD moves will track S&P 500 index direction with firm oil prices acting as a drag on gains.

Technical view: The USDCAD technicals are bearish. Prices are consolidating losses in a 1.2450-1.24570 range with a minor downtrend line at 1.2570 guarding 1.2660, the December downtrend line. A break below 1.2440 suggests further losses to 1.2310. Only a move above 1.2660 will negate the downside pressure.

For today, USDCAD support is at 1.2450 and 1.2410. Resistance is at 1.2530 and 1.2570. Today’s Range 1.2470-1.2530

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

US weekly jobless claims were 20,000 higher than last week, rising to 231,000 from 211,000. The Philadelphia Fed Manufacturing Survey rose to 23.2 from 15.4). The news slightly underpinned Wall Street futures and undermined the US dollar.

There is a lot of too-ing and fro-ing in global markets, with bond, equity, and FX traders continuously adjusting positions ahead of next week’s FOMC meeting.

Yesterday’s spike in the US 10-year Treasury yield to 1.90% spooked equity traders and knocked Wall Street for a loop. By day’s end, the DJIA and S&P500 index closed down around 0.97%. The trend did not continue overnight and S&P 500 and DJIA futures are about 0.50% higher.

The 10-year Treasury yield is trading just above the bottom of its 1.83-1.869% overnight range

Asia equity indexes were choppy but closed with gains. Hong Kong’s Hang Seng index soared 3.42%, powered by the PBoC trimming 1 and 5 year Prime Loan trades (1-year Prime Lending rate to 3.7% from 3.8% and 5-year Prime Lending rate to 4.65% from 4.70%.

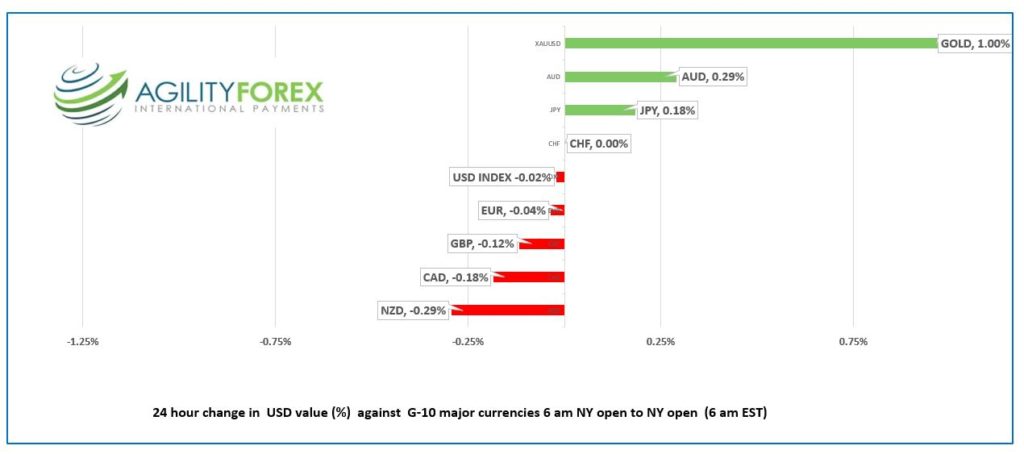

European bourses have flitted between gains and losses and are trading flat to modestly higher. Gold (XAUUSD) plowed through $1830.00 resistance, which had contained topside moves since December, thanks to inflation and geopolitical concerns.

EURUSD traded quietly in a 1.1334-1.1368 range. Eurozone inflation was confirmed at 5.0% y/y, and it had zero impact on trading. Concerns around Russia and Ukraine may limit EURUSD gains.

GBPUSD drifted in a 1.3608-1.3636 band, supported by yesterday’s inflation data which points to higher UK interest rates. Prices do not seem any worse for weather due to PM Johnson’s political problems, and Brexit concerns are on the back-burner.

USDJPY traded defensively, falling to 114.04 from 114.54 due to softer Treasury yields. Japan posted its first trade deficit since 2019.

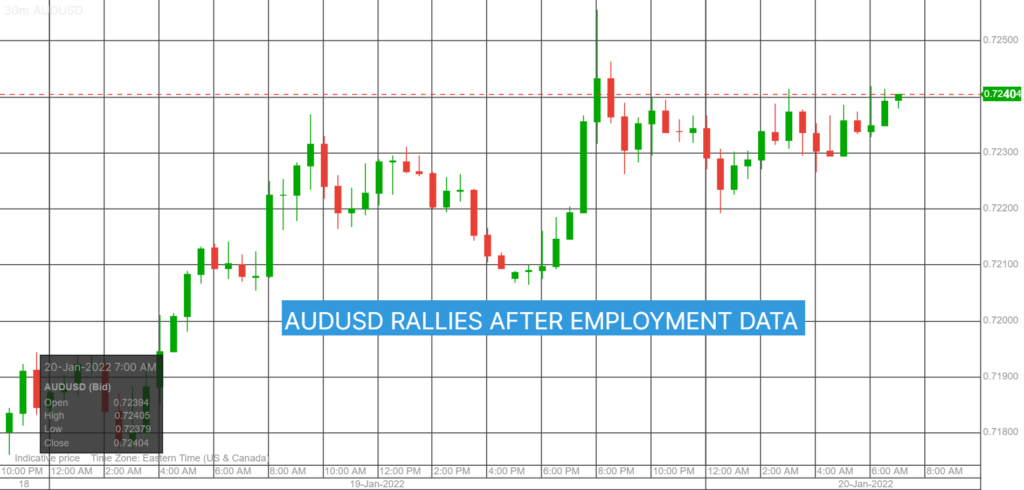

AUDUSD rallied to 0.7256 from 0.7210 on the back of rising interest rate expectations following a stellar employment report. Australia added 64,800 new jobs, and the unemployment rate dropped to 4.2%%, a level last seen in 2008. NZDUSD underperformed due to AUDNZD demand.

Chart of the Day: AUDUSD

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

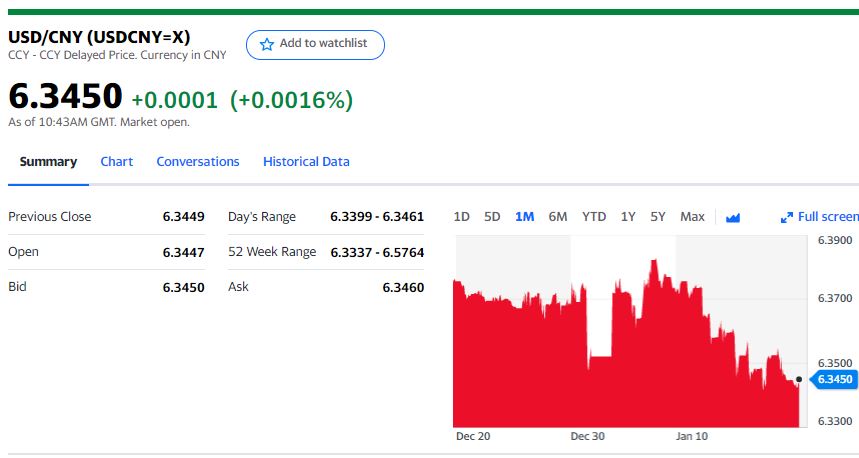

China Snapshot

Today’s Bank of China Fix 6.3485, previous 6.3624

Shanghai Shenzhen CSI 300 rose 0.90% to 4,823.51

PBoC trims 1-year Prime Lending rate to 3.7% from 3.8% and 5-year Prime Lending rate to 4.65% from 4.70%

Chart: USDCNY 1 month

Source: Yahoo Finance