Photo: wannapik.com

March 16, 2023

- Swiss National Bank throws life-saving ring to Credit Suisse.

- US data shows resilient economy.

- US dollar opens higher compared to Wed, but dips overnight.

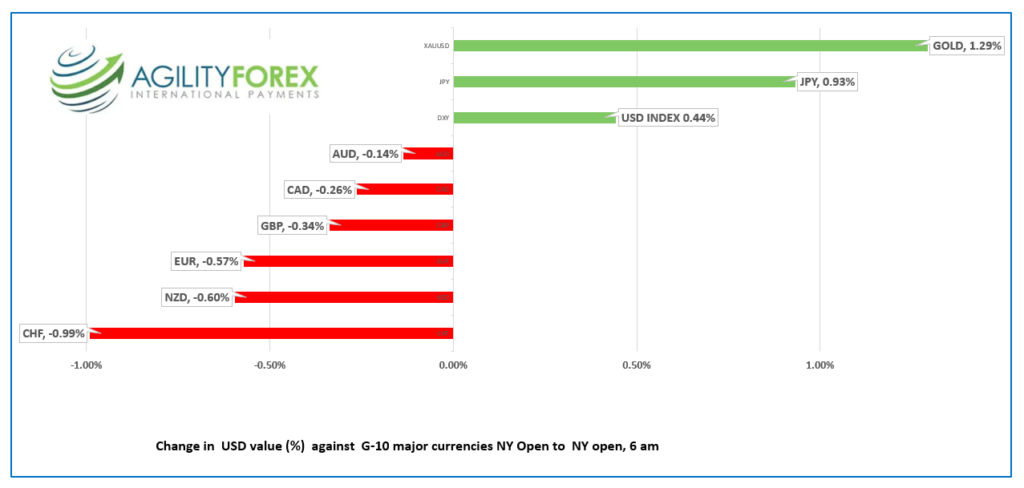

FX at a glance

Source: IFXA Ltd/RP

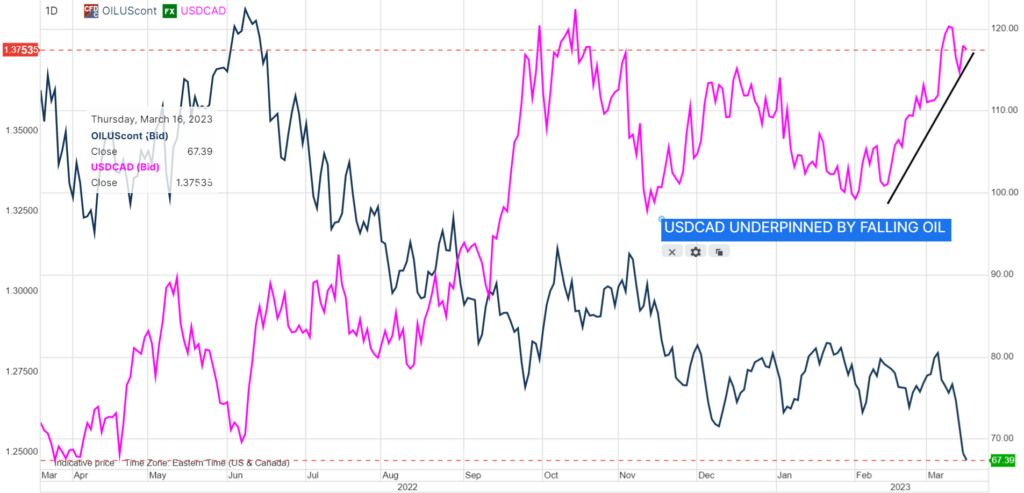

USDCAD Snapshot: open 1.3748-52, overnight range 1.3724-1.3769, close 1.3768

USDCAD consolidated yesterday’s gains in a 1.3724-1.3769 range with prices flirting with the top in NY trading. Traders are content to follow broad US dollar moves as there is nothing going on domestically that has any bearing on FX.

Oil prices are exacerbating USDCAD strength. WTI dropped through $72.70/b, the bottom of the range that had limited losses since January and then accelerated down to $67.15/b today. The drop was exacerbated by rising US crude inventories, broad US dollar strength, and fear of slowing demand if the Banking woes continue.

Expect more choppy price action in a 1.3660-1.3860 range until next week’s FOMC meeting.

USDCAD Technical Outlook

The intraday USDCAD technicals are unchanged from yesterday. They are bullish above 1.3700, looking for a break above 1.3790 to extend gains to 1.3860. A downside break targets 1.3660 then 1.3610.

For today, USDCAD support is at 1.3700 and 1.3660. Resistance is at 1.3790 and 1.3850

Today’s range 1.3710-1.3810

Chart: USDCAD and WTI oil daily

Source: Saxo Bank

G-10 FX recap and outlook

When the going gets tough, tap a central bank. That’s the survival template for the global banking system that uses taxpayer funds to mask incompetence, fraud, and greed by private sector banking and financial institutions.

The head gnome of Zurich (Swiss National Bank) pledged $54 billion to support Credit Suisse claiming it “meets the capital and liquidity requirements imposed on systemically important banks.” A Credit Suisse press release spun the bail-out as the Credit Suisse Group taking “decisive action to pre-emptively strengthen liquidity and announces public tender offers for debt securities.”

The news came too late for Asian equity traders with a 1.46% drop in Australia’s ASX 200 index leading the pack lower. European equity indexes rallied on the back of the Credit Suisse bail-out. The UK FTSE 100 is up 0.96% while the German Dax rose 0.54%. The S&P 500 futures are unchanged.

The US 10 year Treasury yield is 3.49% The US 2-year Treasury yield rebound from yesterday’s low of 3.745% reached 4.02% in early NY before sliding to 3.438%.. Traders are no longer panicked but continue to hyperventilate.

The debate about next weeks Fed rate decision is adding to market volatility. It is a 50/50 choice between unchanged and a 25 bp bump. The debate did not get any easier today.

If the Fed was truly data dependent, today’s stronger than expected data combined with the fairly hot inflation reports would almost guarantee a 50 bp hike next week.

That won’t happen. Financials markets are too jittery to withstand and 50 bp hike while sticky inflation and Fed credibility almost guarantees a 25 bp bump.

Geopolitical tensions are another layer of uncertainty. The pudgy, little lunatic in North Korea continues to throw missiles around to show is displeasure at, well anything. Honduras, one of the countries former President Trump describe with naughty language, is establishing diplomatic ties with China. Chinese diplomats are jet-setting to Russia, Ukraine, and the Middle East in an ongoing passive-aggressive push to undermine the US.

EURUSD rallied from 1.0574-1.0635 due to the Credit Suisse funding announcement. Traders are awaiting the ECB press conference to see how President Christine Lagarde dances around inflation risks, banking concerns against the backdrop of the Russia-Ukraine war. The fun starts at 8: 15 am EDT).

GBPUSD continues to trade defensively after falling from 1.2180 yesterday. Prices chopped about in a 1.2033-1.2112 range and have slid to 1.2036 in NY trading. Traders are relieved that the UK budget avoid a Kwasi Kwarteng-style reaction and shifted their focus back to the global banking sector.

USDJPY continued the slide that started March 8 when it traded at 137.80. The plunge in the US 10-year Treasury yield combined with safe-haven demand for yen due to global banking sector worries drove USDJPY from an overnight peak of 133.50 to 132.50. Weaker than expected Japanese Industrial Production and Capacity Utilization data was not a factor.

AUDUSD rallied from 0.6613 to 0.6661, supported by a robust employment report. Australia added 64,600 new jobs in February (forecast 50,000) while the unemployment rate fell to 3.5%. The results suggest a 25 bp rate hike next month.

Today’s US data includes Philadelphia Fed Manufacturing Index, weekly jobless claims, building permits, and wholesale sales.

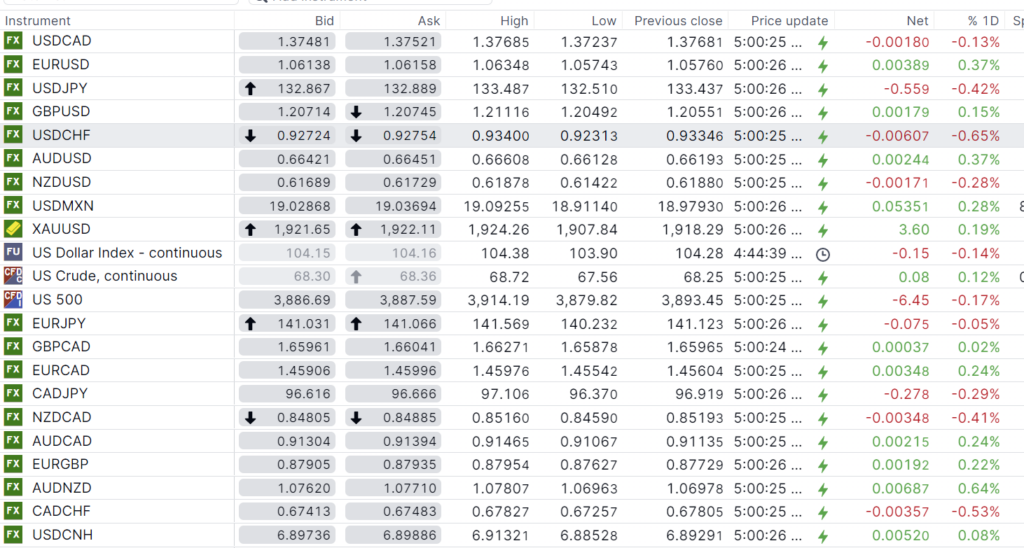

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

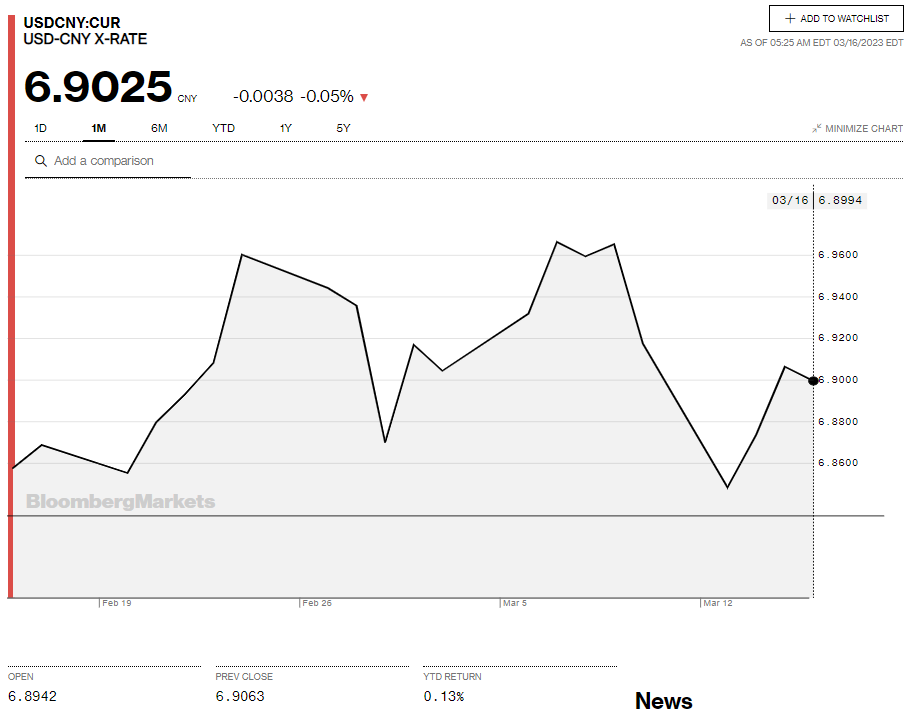

China Snapshot

Bank of China Fix: 6.9149, Previous: 6.8680

Shanghai Shenzhen CSI 300 fell 1.20% to 3939.15.

Chart: USDCNY 1 month

Source: Bloomberg