Source: MGM

- Chinese protests force XI to talk of covid-zero relief

- Hawkish-fed speak keeps dollar bears at bay

- US dollar opens higher compared to Monday, but well below its best levels

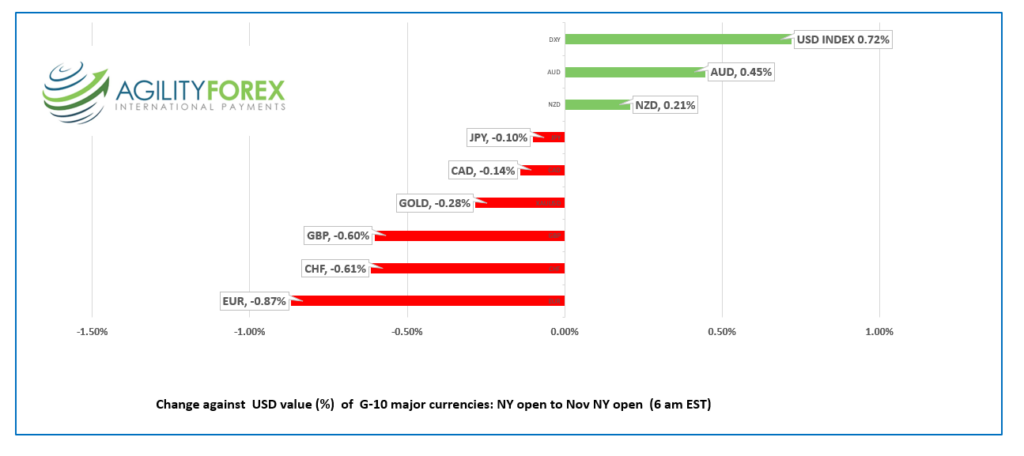

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3452-56, overnight range 1.3411-1.3523, close 1.3496

USDCAD is bid. Prices rallied from 1.3410 to 1.3500 yesterday then dropped to 1.3410 in Europe. USDCAD has been on a one-way street higher since, reaching 1.3523. The rally is a bit of an anomaly as none of the major G-10 currencies moved in a similar fashion.

RBC is buying HSBC for $13.5 billion, which may help explain USDCAD demand today.

WTO oil fell to $73.50/barrel yesterday then rallied to $79.15/b in NY today. Prices are supported by hopes that China eases covid restrictions and concerns ahead of the Opec meeting at the end of the week.

Canada Q3 GDP surprised to the upside, rising 0.7% q/q compared to 0.4% q/q gain expected. Statistics Canada wrote its the fifth consecutive quarterly increase. “Growth in exports, non-residential structures, and business investment in inventories were moderated by declines in housing investment and household spending.”

USDCAD remained bid after the data.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish following the break above 1.3490 and are looking for a break above 1.3550 to extend gains to 1.3660. A break below 1.3490 suggests more 1.3410-1.3550 consolidation.

Longer term, USDCAD has bounced between 1.3210 and 1.3960 since September 12, but maintains a bullish bias while prices are above 1.3080.

For today, USDCAD support is at 1.3490 and 1.3450. Resistance is at 1.3530 and 1.3570

Today’s range 1.3470-1.3570

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Chinese Covid Zero protestors scored a victory, sort of. Visions of a pitch-fork wielding mob storming the Presidential palace in the Imperial City apparently spooked wannabe Emperor Xi Jinping and he ordered a massive police presence into the streets. Then he threw the masses a bone, via the China Global Times. The editor tweeted “China may walk out of the shadow of COVID-19 sooner than expected.”

That tweet went a long way in offsetting the risk aversion sentiment that permeated financial markets on Monday after some Fed officials regurgitated their “higher rates for longer” outlooks.

The news powered the Hong Kong Hang Seng index to a 5.24% gain and lifted the Shanghai Shenzhen CSI 300 index by 3.0%. Australia’s ASX 200 index came late to the party and only managed a 0.33% gain. Weak data weighed on Japan’s Nikkei 225 index which fell 0.48%.

The positive equity sentiment carried over into Europe. The major indexes are trading in the green led by the UK FTSE100 which has risen 0.72% today. S&P 500 futures are a tad more cautious but managed to climb 0.14% overnight.

China unrest and Fed policymaker comments fuelled yesterday’s US dollar rally.

St Louis Fed President Bullard and New York Fed President Williams reminded markets that the hawks were not hooded. Mr Bullard said financial markets were underestimating the risk that the Fed may need to be more aggressive in hiking rates. Mr William noted that inflation risks were still to the upside and more rate hikes were needed to restore the balance in the economy.

Financial markets are likely to be whippy today due month end portfolio rebalancing flows, concerns around the content of Fed Chair Jerome Powell’s speech on Wednesday, and positioning into Friday’s nonfarm payrolls data.

Mr Powell adopted a bullish tone in his post-FOMC press conference which suggests his remarks will likely endorse the higher rates for longer narrative.

EURUSD climbed from 1.0340 to 1.0495 Monday morning, then erased the gains in the afternoon to close at 1.0340. Prices drifted in a 1.0335-1.0395 range overnight. Traders ignored German CPI data which showed inflation at 10.0% which was a tad lower than the 10.3% in October. The EURUSD technicals are bullish above 1.0310.

GBPUSD has chopped about in a 1.1955-1.2063 range. Gains may be limited after BoE policymaker Catherine Mann suggested rates could fall next year. She said, “there will be a peak that will serve to temper medium-term inflation expectations, and at that point, we have the opportunity to pull back from that peak.”

USDJPY peaked at 139.35 in Asia overnight then dropped to 137.95 in NY. Prices are undermined by disappointing domestic data after the unemployment rate was unchanged at 2.6% (forecast 2.5%) while October Retail Trade rose 4.3% y/y rather than the 5.0% forecast. In addition, the soft US 10-year yield at 3.672% also weighed on prices.

AUDUSD climbed from 0.6642 to 0.6747 supported by anticipation of the Chinese economy reopening earlier than expected and by the broad US dollar weakness.

Today’s US data includes, September Case-Shiller Home Price Index, and Consumer Confidence.

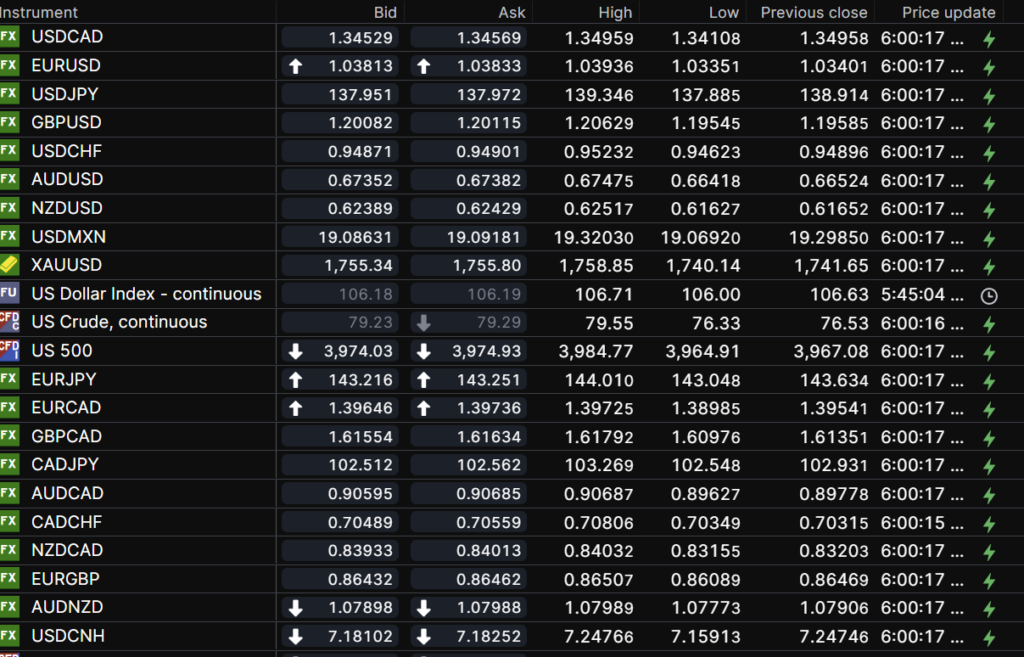

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

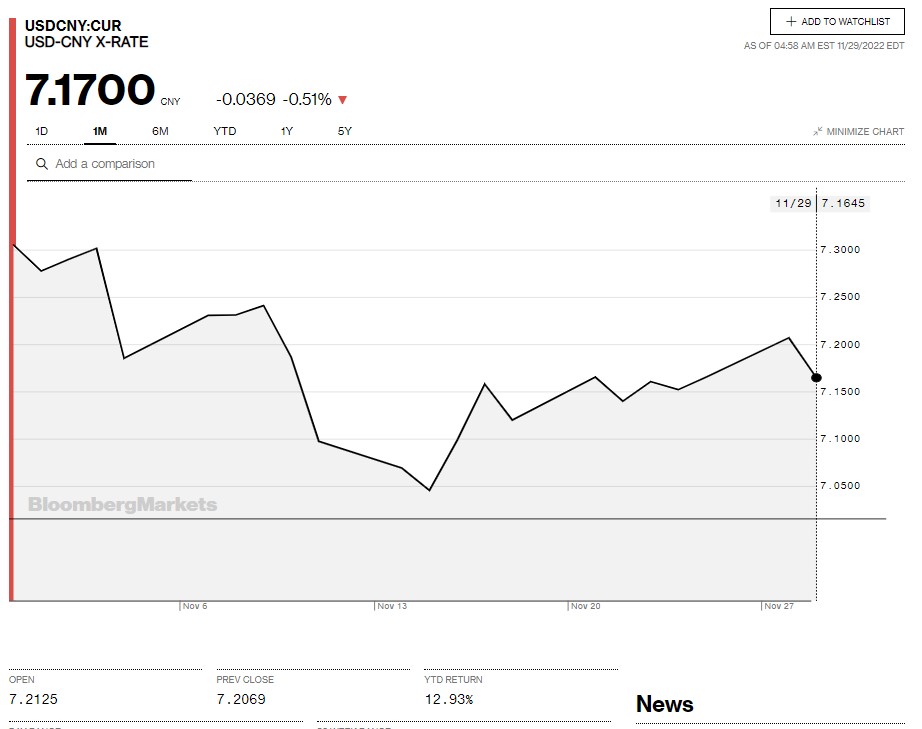

China Snapshot

Today’s Bank of China Fix: 7.1989, previous 7.1617

Shanghai Shenzhen CSI 300 rose 3.0% to 3848.42

Massive protests are prompting Chinese leaders to re-think the covid-zero policy. China Global Times Editor tweeted “China may walk out of the shadow of COVID-19 sooner than expected.”

Chart: USDCNY 1 month

Source: Bloomberg