By Michael O’Neill

“Thou Shalt Not Commit.” That is the most important takeaway from today’s Bank of Canada monetary policy statement and Monetary Policy Report (MPR). Policymakers left the benchmark bank rate unchanged at 5.0%, which surprised no one.

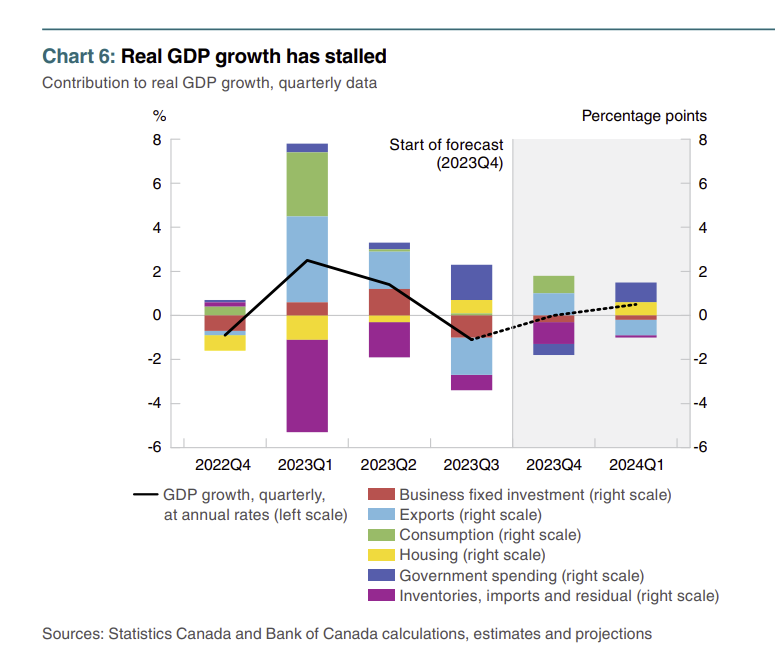

The quarterly projections in the MPR were tweaked. Inflation is expected to finish the year at 2.8%, which is a tad less than the 3.0% predicted in October, and it is not expected to return to the target until 2025. The economy is expected to stagnate in 2024 with GDP dipping to 0.8% from October’s prediction of 0.9%. The BoC doesn’t expect any economic growth in Q1 2024.

Source BoC MPR January 2024

On a bright note, policymakers think that rates have peaked. Mr. Macklem said, “Governing Council’s discussion about future policy is shifting from whether monetary policy is restrictive enough, to how long to maintain the current restrictive stance.”

Naturally, he qualified the comment by warning, “That doesn’t mean we have ruled out further policy rate increases. If new developments push inflation higher, we may still need to raise rates.”

Rate hikes are not going to happen. The MPR points out that although the global economy is slowing, it has been more robust than expected due to the surprising strength of the US economy. The BoC is very unlikely to raise rates in an environment where the domestic economy is flirting with a recession while the economy of its main trading partner booms.

Another reason for the BoC caution is that it doesn’t have a lot of faith in its economic forecasting tools. They are getting the blame for Governor Macklem’s 2020 pronouncement of low rates for a long time and for policymakers insisting that inflation increases were transient. Other central banks also suffered from a forecasting model malfunction. To be fair, the models couldn’t predict Russia’s invasion of Ukraine and the subsequent massive supply chain disruptions that ensued. Nor could they predict the wholesale shift from commuting to the office to a hybrid work-from-home model. Nevertheless, BoC policymakers have reawakened to the garbage in, garbage out concept and have embarked on a wholesale revamp of their existing models.

Although the Bank of Canada’s monetary policy outlook is significant for the Canadian economy, its impact is greatly overshadowed by the vastly greater influence of the US Federal Reserve’s policies on Canada and other G-10 economies. And the Fed meeting is on January 31.

Recent comments from Fed officials have finally convinced traders to push out expectations for the first rate cut to May 1, from March 20. The odds that rates will be lowered on March 20 have dropped from 75.6% a month ago to 40.5% today. Even so, traders are still expecting that Fed funds will be in the 3.75-4.25% range by December 18.

At the last FOMC meeting, policymakers predicted that core inflation (excluding food and energy) would be around 2.4% in 2024. They still expect to cut rates by 75 bps this year even if inflation has not hit the target but have pushed back against more aggressive rate reduction expectations.

Nevertheless, markets remain optimistic about the US rate trajectory and believe in the elusive Goldilocks scenario, which is when inflation falls, unemployment rises, but America avoids a recession. That scenario got a bit of support from the Global S&P PMI (preliminary) survey on January 24. Manufacturing, Services, and Composite PMI data were at a seven-month high, prompting its Chief Business Economist Chris Williamson to write, “An encouraging start to the year is indicated for the US economy by the flash PMI data, with companies reporting a marked acceleration of growth alongside a sharp cooling of inflation pressure.

Most important for Canadians is, “What does that mean for the Canadian dollar?”

The Canadian dollar weakened following the BoC MPR, which is counterintuitive if you believe Canadian rates may stay higher than US rates for the short term. Bond traders think so, as the spread between the Canadian and US 10-year government bonds narrowed, which would normally give the currency some support.

Not this time. The USDCAD rally from 1.3430 to 1.3505 following today’s MPR is partly due to bearish short-term positioning being unwound alongside Wall Street gains. In addition, traders appear to want US dollars based on American economic outperformance compared to Europe, the UK, and Canada. The long-term USDCAD technicals are bullish with the uptrend from May 2021 intact while prices are above 1.3220. A break above 1.3540 should see a retest of 1.3900.

In the end, “Thou Shalt Not Commit” is a viable strategy for every central banker struggling to cope with todays.