July 10, 2024

- Powell refuses to send rate cut timing signals.

- Markets on hold until Thursday’s US CPI

- US dollar opens slightly lower, but within well-defined ranges.

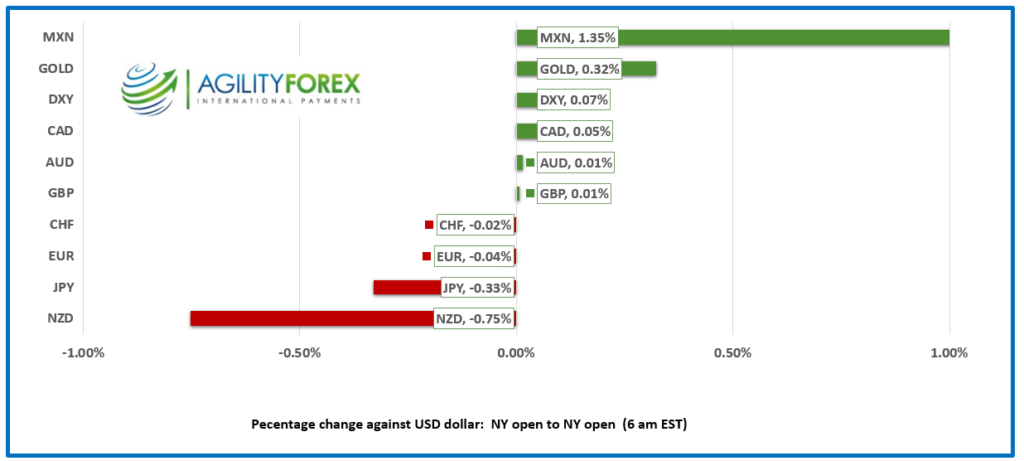

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3641, overnight range 1.3628-1.3643, previous close 1.3637

USDCAD is drifting aimlessly in a narrow band and the price action is virtually unchanged from yesterday. That is unlikely to change today due to the absence of actionable economic data from Canada or the US.

It is day 2 of Fed Chair Powell’s congressional testimony but he is expected to repeat yesterday’s comments.

Oil prices extended this week’s slide and they dropped to 80.81 from 81.83. The APIR report that US crude inventories fell by 1.9 million barrels last week was offset by Chinese inflation data suggesting weak Chinese economic growth which would also weigh on demand.

USDCAD Technicals

The intraday technicals remain unchanged. They are neutral with prices trapped between 1.3590 and 1.3660, which is unlikely to change until after tomorrow’s US inflation data.

The longer term outlook is unchanged. The price action below the 200-day moving average and the 38.2% Fibonacci retracement level of the January -April range provide a cluster of strong support levels. A decisive breech of this area targets 1.3510.

For today USDCAD support is at 1.3590 and 1.3550. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3590-1.3690

Chart: USDCAD 4 hour

Source: DailyFX

Subtly Optimist Powell Boosts Rate Cut Hope

Fed Chair Jerome Powell injected easing labor markets into the rate cut discussion as he reminded the Senate of the Fed’s dual mandate. He noted that “We’ve seen that the labor market has cooled really significantly across so many measures. It’s not a source of broad inflationary pressures for the economy now.” He said that he is well aware that the Fed has two-sided risks but he had no intention of sending any signals to the market on the timing of rate cuts.

Hack Attack

China has been caught with its hands in the fortune cookie jar, or more accurately the hard drives of other governments and private sector companies. Australia, the US, Japan, South Korea, Germany, New Zealand, and Canada said that the PRC Ministry of State Security conducted malicious cyber operations directed at public-facing infrastructure. China called it a smear campaign.

EURUSD

EURUSD was directionless in a 1.0811-1.0826 range. Support from Fed Chair Powell’s testimony was offset by ongoing concerns around French politics and the shape of the incoming government.

GBPUSD

GBPUSD is spinning its wheels but at the top of its 1.2783-1.2812 range in NY trading. Powell’s slightly dovish outlook for US rates is underpinning prices in quiet trading ahead of a slew of UK economic data being released on Thursday. That includes May GDP, Industrial Production, Manufacturing Production, and Trade, just ahead of the US June inflation data.

USDJPY

USDJPY climbed from 161.26 to 161.62 in an uneventful session. Producer prices rose 0.2% in June compared to the forecast for a 0.4% increase and 0.7% in May. Any negative sentiment from the monthly data was negated by the annual PPI which was 2.9% compared to 2.6% previously.

AUDUSD and NZDUSD

AUDUSD traded uneventfully in a 0.6732-0.6751 range as support from hopes the Fed cuts rates sooner rather than later were offset by concerns about China’s sluggish economic growth.

NZDUSD suffered, falling from 0.6133 to 0.6065 after the RBNZ announced it identified as a dove. The central bank surprised no one when it left the Overnight Cash Rate (OCR) unchanged at 5.5% but raised a lot of eyebrows when it ditched its hawkish bias. They are more confident that inflation will be on target in the second half of the year and they dropped references about further rate cuts. ASB economists expect a rate cut before Christmas.

USDMXN

USDMXN dropped from 18.0590 yesterday to 17.7786 today following the one-two punch from inflation and Jerome Powell. Mexican inflation was hotter than expected while Mr. Powell hinted that rate cuts may be on the horizon.

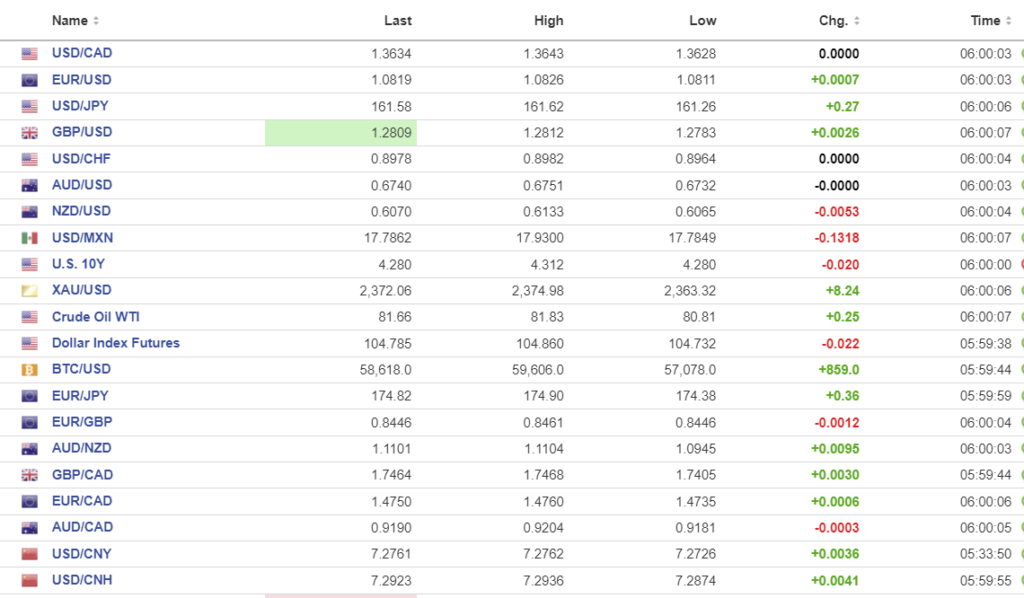

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1342 vs exp. 7.2711 (prev. 7.1310).

Sanghai Shenzhen CSI 300 fell 0.32% to 3426.97.

China June CPI 0.2% y/y vs forecast 0.4%, PPI -0.8% y/y vs -1.4% in May.

Analysts suggest the soft inflation data is further evidence of weak domestic demand which has not recovered despite numerous fiscal stimulus programs.

Chart: USDCNY and USDCNH

Source: Investing.com