Source: freepik

- Americans still counting mid-term votes

- Risk on euphoria fading

- US dollar claws back some of Tuesday’s losses, opens mixed

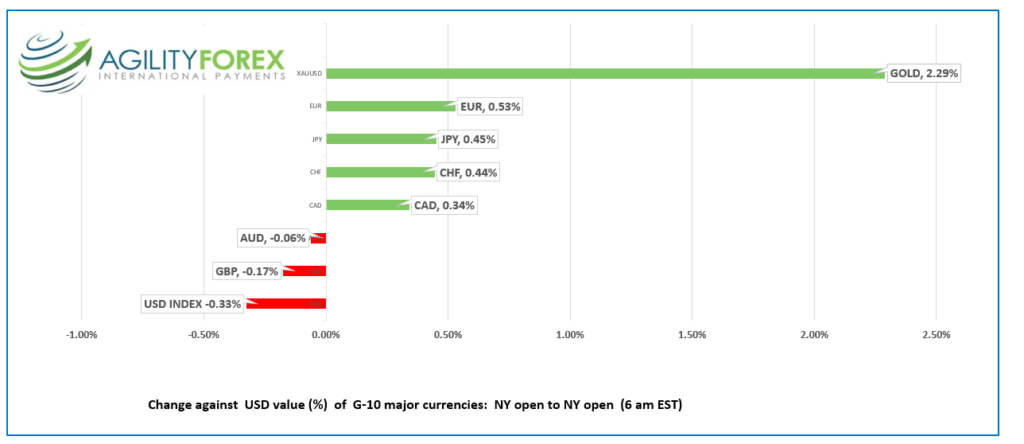

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3452-56, overnight range 1.3415-1.3461, close 1.3427

Expectations for a quiet FX session yesterday went out the window in a hurry. US dollars were dumped and USDCAD went along for the ride. And what a ride it was.

The S&P 500 soared nearly 2.0% (low -to top) during Tuesday’s session and that led to a stop-loss fueled drop in USDCAD which knocked prices through support at 1.3440, before finding a floor at 1.3389. The S&P 500 retreated to close with a 0.56% gain, and USDCAD rallied to close at 1.3427.

The USDCAD retreat occurred even as WTI oil prices extended losses from Monday, skidding to $88.12 overnight. In addition, CAD/US 10-year yield spreads widened in favour of the US. Furthermore, the BoC delivered a dovish hike, contrasting with Fed Chair Powell’s hawkish US rate outlook. Meanwhile, the US 10-year Treasury yield is still a lofty 4.14%. None of the above supports a weaker USDCAD.

WTI oil prices are trading defensively after the API reported crude inventories rose 5.61 million barrels last week and because of rising Covid cases in China.

The Canadian data calendar is empty.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3480, looking for a break below 1.3380 to extend losses to 1.3190. A break above 1.3480 targets 1.3550 and a break above this level suggest a short-term floor at 1.3380 and opens the door to further gains to 1.3640.

The 1.3380 level is the 38.2% Fibonacci retracement level of the 2022 range which if broken suggests further losses to 1.3190 (50% retracement), then 1.3015 (61.8% retracement).

For today, USDCAD support is at 1.3405 and 1.3380. Resistance is at 1.3480 and 1.3530. Today’s range 1.3390-1.3480

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FX traders dumped dollars aggressively yesterday, driving the greenback to key support levels against the major G-10 currencies. The sell-off began to fade in the late afternoon, and there was no follow-through selling overnight.

Its all about the results of the US mid-term elections and so far, predictions for a stock market rally and the end of the US dollar bull market, look premature.

The US mid-term election results (so far) will disappoint both parties, but they will both claim a win.

Source: WSJ

Elsewhere, Asian equity indexes closed in the red except for Australia’s ASX 200 which posted at 0.56% gain. European equity indexes are trading with a negative bias as are DJIA and S&P 500 futures. Oil and gold prices are lower than where they closed Tuesday.

EURUSD traded in a 1.0034-1.0073 overnight after failing to break above major resistance in the 1.0095-1.0100 area yesterday. Its hard to believe the rally is sustainable in the face of the ongoing Russia and Ukraine war, the looming energy crisis with the onset of winter, and the hawkish Fed rate outlook. Nevertheless, the EURUSD technicals are bullish above 0.9770.

GBPUSD gave back all of yesterdays gains and dropped from 1.1566 in Asia to 1.1421 in early NY. The UK is in the throes of a recession suggesting and traders will remain cautious ahead of the upcoming November 17 budget. The intraday technicals are bullish above 1.1400 and the October uptrend line is at 1.1190. GBPUSD has strong resistance at 116.50.

USDJPY chopped about in a 145.18-145.90 range. Downside pressure from broad US dollar selling and the fear of BoJ intervention more than offset the steady 10-year US Treasury yield.

AUDUSD traded sideways in a 0.6477-0.6521 range until mid-morning in Europe when prices dropped to 0.6460. The drop was blamed on profit-taking as traders await the final US election results and renewed concerns about slow China growth. RBA Deputy Governor Michelle Bulloch said “further increases in rates will be required” to cool inflation.

NZDUSD traded in a 0.5893-0.5973 range with prices weighed down by renewed US dollar demand.

There are no top tier US data releases today, leaving the focus on election results.

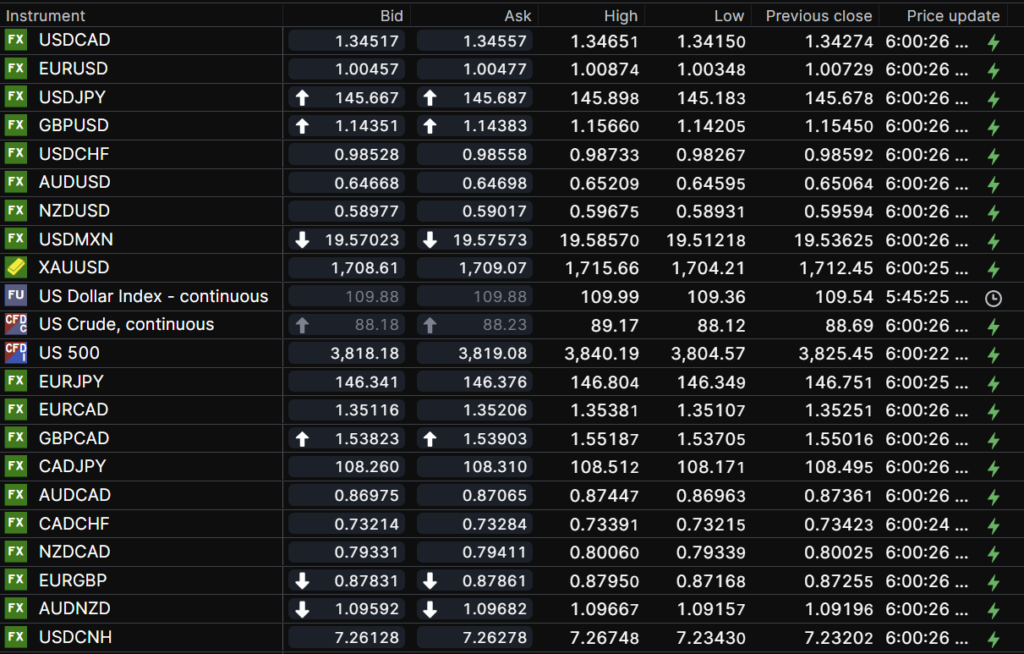

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

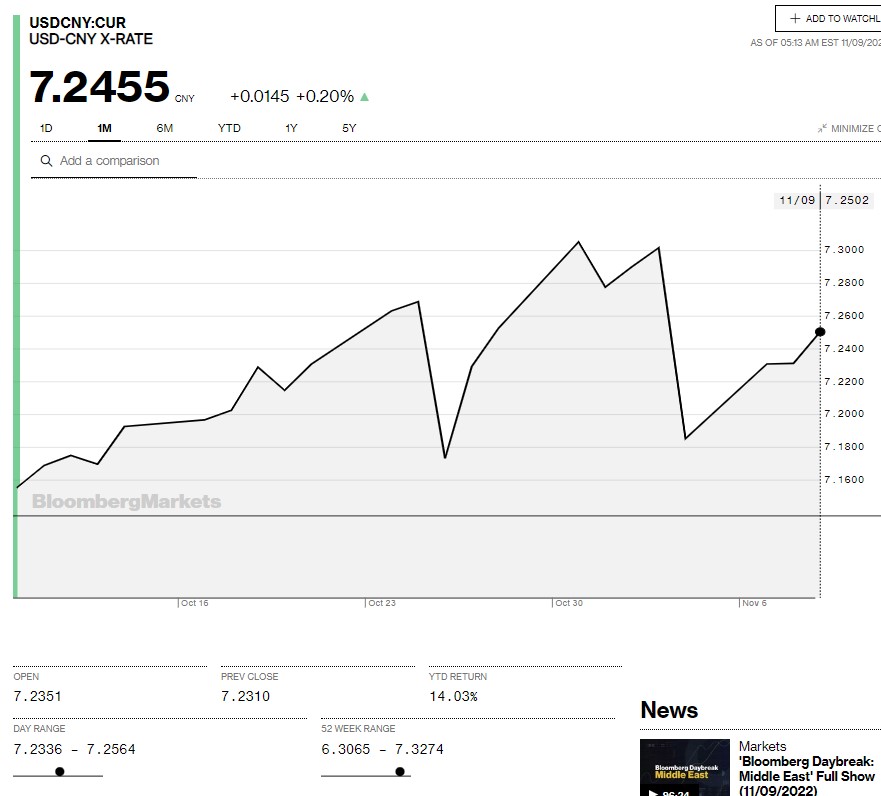

China Snapshot

Today’s Bank of China Fix: 7.2189, previous 7.2150

Shanghai Shenzhen CSI 300 fell 0.94% to 3714.27

October CPI 2.1% y/y, forecast 2.4%, September 2.8%

October PPI -1.3% y/y, forecast -1.5%, September 0.9% y/y

China Covid case rise again, offsetting positive sentiment from reports China State Planner asked banks to ramp up lending for manufacturing infrastructure.

Chart: USDCNY 1 month

Source: Saxo Bank