Photo: Hallmark

February 14, 2023

- CPI headline and core higher than forecast.

- UK employment data supports BoE rate hike.

- US dollar opens soft, grinds out small gains post-CPI.

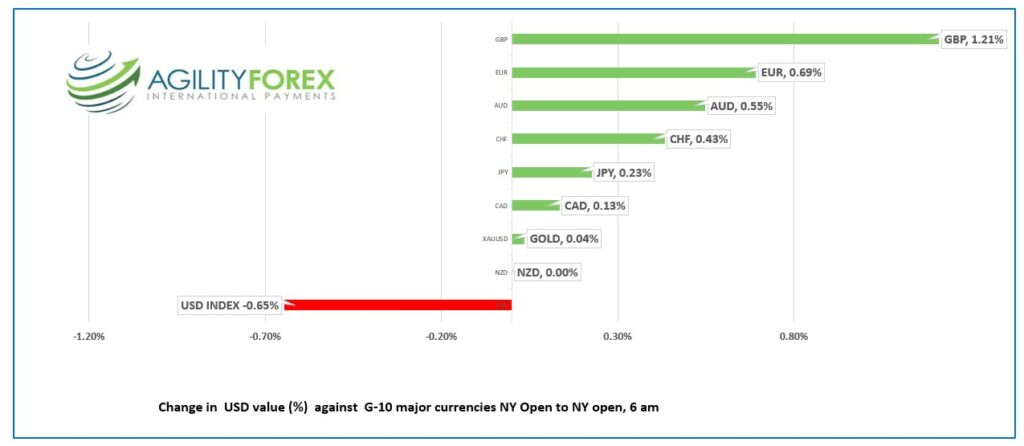

FX at a glance

Source: IFXA Ltd/RP

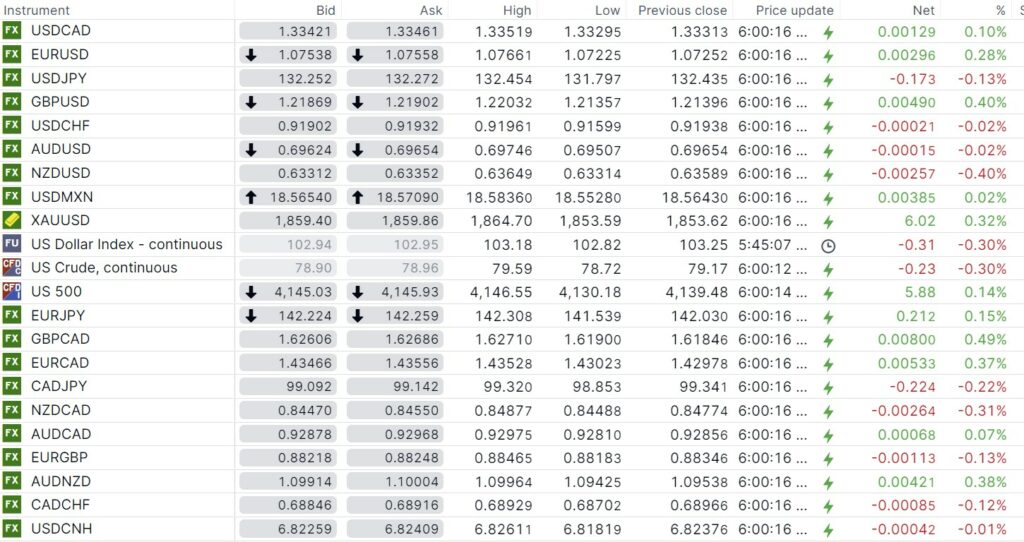

USDCAD Snapshot: open 1.3342-46, overnight range 1.3276-1.3352, close 1.3331

USDCAD churned in a 1.3320-1.3340 overnight then dipped to 1.3276 in the wake of the US inflation report, before bouncing to 1.3320.

USDCAD is tracking the S&P 500 index with gains driving the currency pair lower, while deriving additional support from Friday’s block-buster jobs data.

The Canadian jobs data may be the catalyst for the Bank of Canada interest rate outlook to shift from “pause” to “play” but traders are more focused on what today’s US CPI report means for Fed interest rates.

WTI oil retreated from yesterday’s $80.53 peak to $78.62/b overnight. The dip was entirely due to US dollar weakness as prices remain supported by Russian production cuts and anticipated increasing demand from China.

There are no domestic economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3420 looking for a break support to test the June uptrend line in the 1.3270-80 area. That level was seen briefly in the wake of the CPI data, but prices quickly bounced to 1.3320.

The weekly chart suggests that a decisive breach below 1.3230 targets 1.2998, the 50% Fibonacci retracement of the June 2021-October 2022 range.

For today, USDCAD support is at 1.3290 and 1.3270. Resistance is at 1.3370 and 1.3420.

Today’s range 1.3290-1.3370

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

It’s Valentine’s Day. To many, it means candle-lit dinners at expensive restaurants, chocolates and the promise of whoopee! To others, it’s a day of heartbreak, restaurant reservation snafus and the day when Chicago mobster Al Capone removed his competition.

Traders anticipated another soft-Core CPI print. They didn’t get. January Core CPI Headline CPI rose 5.6% y/y compared to the consensus forecast of 5.5% although it was a tick lower that the 5.7% in December. Headline CPI had a similar result It rose 6.4% y/y (forecast 6.2%, December 6.5% y/y).

The results will support bullish and bearish views for US rates and continue to leave FX and equity market direction somewhat confused.

Fed Vice Chair Lael Brainard is moving to the Whitehouse to become Director of the National Economic Council. That removes a dovish-leaning voice from the FOMC.

Asia equity indexes closed higher led by a 0.64% gain in Japan’s Nikkei 225 index. European bourses are positive but off their best levels after the U inflation report. S&P 500 futures are 0.08% higher. The US 10-year Treasury yield is 3.688% as of 6:00 am PT.

EURUSD traded sideways in Asia then rallied from 1.0723 to 1.0804 in the wake of the CPI release before easing back to 1.0780. EURUSD is underpinned by EU Q4 GDP rising 0.1% q/q as expected, and employment rising 0.4%.

GBPUSD traded with a bid in a 1.2136-1.2207 range then spiked to 1.2269, post-CPI before dropping to 1.2212. Prices were also boosted by data showing UK wages rose 6.7% (3month y/y) in December, well above the forecast and previous result of 6.5%. The rise in wages gives the BoE another reason to raise rates.

USDJPY traded in a 131.51-132.92 range with the high just before the US CPI data and the low seen in the aftermath. The Japanese government confirmed the nomination of Kazua Ueda to be Bank of Japan governor.

AUDUSD drifted in a 0.6951-0.7028 range. Due to broad US dollar weakness, post CPI. RBA Governor Philip Lowe is catching flax for meeting privately with banks while ignoring the public. He probably doesn’t care as his term ends in September.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

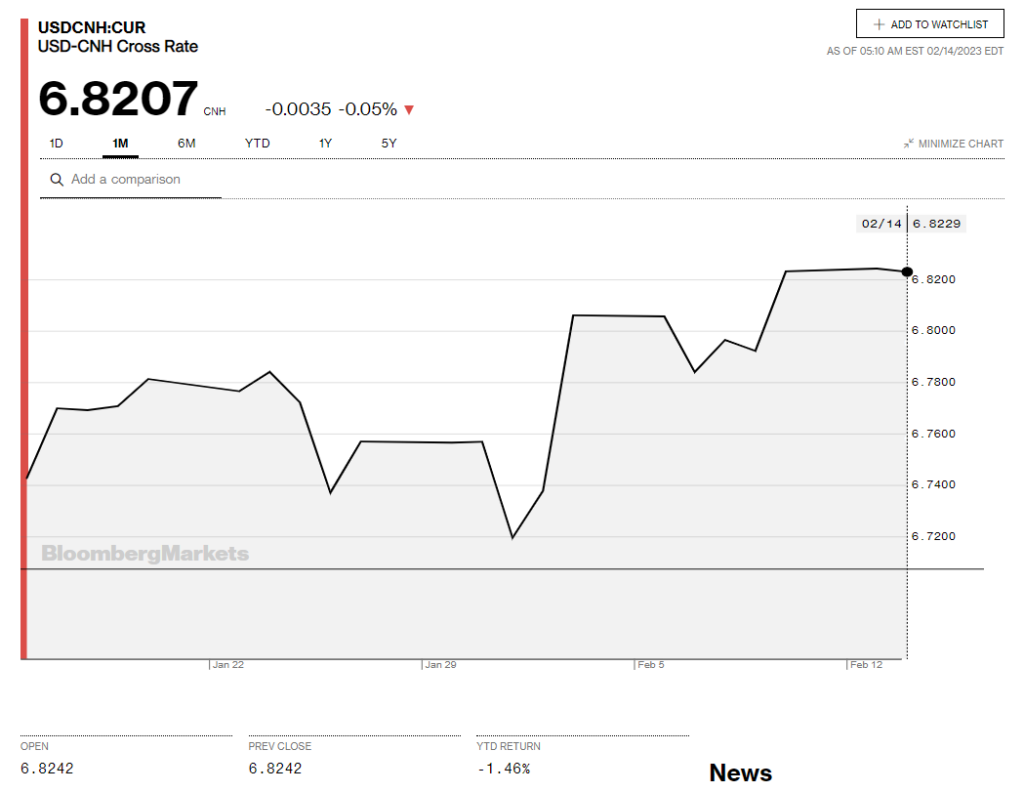

China Snapshot

Bank of China Fix: 6.8136, Previous: 6.8151

Shanghai Shenzhen CSI 300 rose 0.04% to 4145.29.

Chart: USDCNY 1 month

Source: Bloomberg