March 21, 2024

- Swiss National Bank surprises with a 25 bp rate cut to1.5%.

- Bank of England leaves rates unchanged at 5.25%

- US dollar opens with large losses except against CHF.

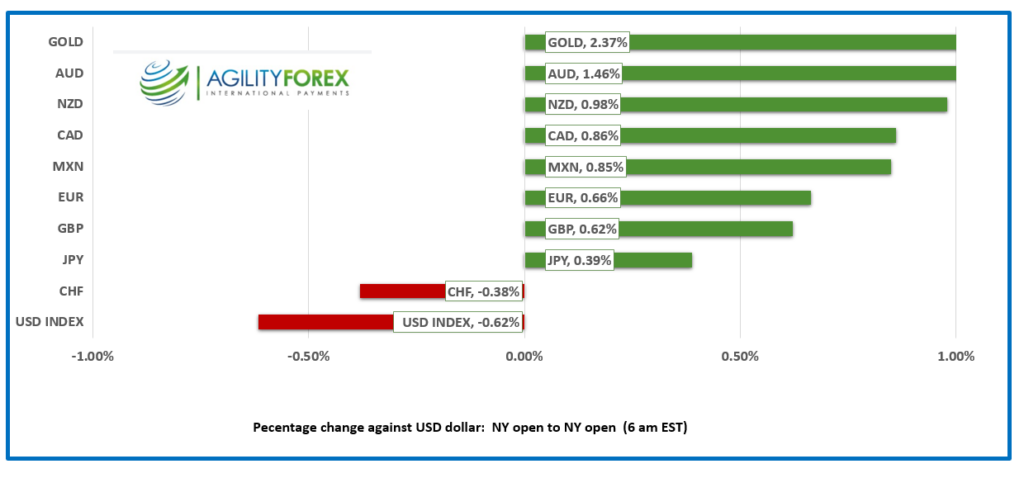

FX at a Glance

Source: IFXA/RP

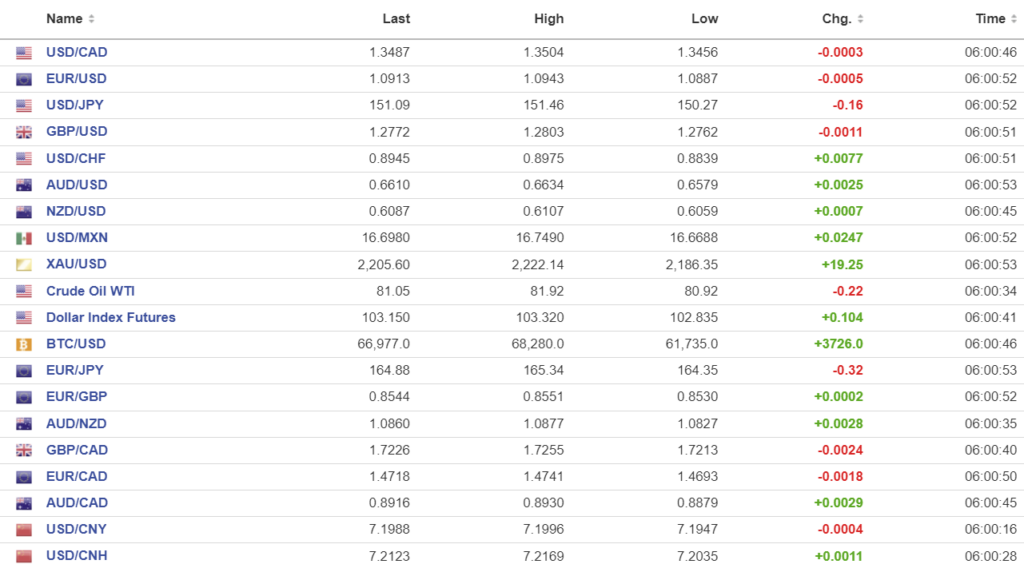

USDCAD Snapshot: open 1.3485-89, overnight range 1.3456-1.3513, close 1.3493

USDCAD dropped from a pre-FOMC peak of 1.3606 to a low of 1.3456 overnight. The unchanged Fed rate outlook narrowed the spread between CAD and US 10 year yields which weighed on the currency, as did steady WTI oil prices above $80.00/b. Prices ticked back to 1.3513 after US weekly jobless claims rose 210,000 suggesting the job market remains resilient. The Philadelphia Fed index came in at 3.2, easily topping the forecast for a 2.3 decline.

USDCAD appears to be in happy its comfort zone of 1.3200-1.3600 although speculation that the BoC cuts rates by 25 bps in June is limiting USDCAD downside.

WTI oil prices are near the bottom of the $80.92-$81.92 /b range, supported by broad US dollar weakness and a surprise 1.95 million barrel drawdown in US crude inventories last week.

Up coming US data will dictate USDCAD moves as it should provide clues to “data-dependent” Fed rate decisions.

USDCAD Technicals

Thee intraday USDCAD technicals flipped to bearish with the break below 1.3560 and 1.3510. The bearish sentiment remains intact while prices are below the 1.3530-1.3550 area and looking for a break below the 1.3440-60 zone to target 1.3360,

Longer term, the uptrend line from January 1 is intact while prices are above 1.3460.

For today, USDCAD support is at 1.3460 and 1.34100. Resistance is at 1.3520 and 1.3560. Today’s range is 1.3460-1.3530.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX

If traders were lemmings, the bottom of the cliff would be a gory mess. The herd eagerly bought into speculation that the Fed would only cut rates twice in 2024 and that drove the US dollar index (DXY) to a 3.4% gain from the start of the year to just before yesterday’s FOMC meeting. The Fed left their rate outlook unchanged (3 rate cuts in 2024) and the DXY plunged as traders scrambled to reverse their bets. “Plop, Plop, Fizz Fizz, oh what a relief it is.”

Gold traders cheered and they lifted XAUUSD from $2148.85 yesterday to $2222.14 overnight. Equity traders were not to be outdone. The S&P 500 index closed up 0.89% for 2.52% month-to-date gain.

Asian equity indexes closed with strong gains led by a 2.03% rise in Japan’s Nikkei 225 index while Australia’s ASX 200 gained 1.12%. European bourses are in the green with the UK FTSE 100 gaining 0.93%.SPX futures are up 0.35% while the US 10-year Treasury yield inched down to 4.233% from 4.271% yesterday.

EURUSD spiked following the FOMC meeting and is consolidating the gains in a 1.0887-1.0943 range. The single currency managed to hang on to gains despite disappointing Manufacturing PMI (actual 45.7 vs forecast 47, previous 46.5) and a surprise 25 bp rate cut by the Swiss National Bank. The SNB statement said the rate cut was needed to combat the dampening effect on the economy exacerbated by a weak franc. News that Norway’s Norges Bank left its benchmark rate at a 16 year high of 4.5% took some of the sting out of the SNB move.

GBPUSD is sinking, falling from 1.2803 to 1.2726 after the Bank of England left rates unchanged and issued a dovish statement. That’s because the vote was unanimous. Previously two committee members dissented. Markets have fully priced in three rate cuts in 2024.

USDJPY is trading erratically in a 150.27-151.46 range with traders seemingly confused between the Fed interest rate outlook and the BoJ’s dovish rate hike. The BoJ may be disappointed that it’s first rate hike in 17 years failed to boost the currency which may motivate them to intervene in FX markets.

AUDUSD is trading firmer in a 0.65679-0.6634 range with prices getting a boost from robust economic data. Australia gained 116,500 new jobs in February (forecast 40,000) and the unemployment rate slipped to 3.7% from 4.1%. The results mean the RBA will be reluctant to cut rates in the near term.

NZDUSD eased to 0.6058 after peaking at 0.6107 due to weaker than expected Q4 GDP data (actual -0.3% y/y, forecast 0.1%, Q3 -0.6%) which meant New Zealand finished 2023 in a recession. ASB economists suggest that the GDP data increases the risk of OCR cuts by year end.

USDMXN traded lower in a 16.6688-16.7490 range. Banxico is expected to leave rates unchanged at 11.25% this afternoon but traders are leery as the central bank has a history of surprising markets.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0942 vs exp. 7.1792 (prev. 7.0968).

Shanghai Shenzhen CSI 300 fell 0.12% to 3581.09.

PBoC said it had room to cut bank’s reserve requirement ratio (RRR) which helped reinforce speculation of further stimulus in the pipeline.

A US Admiral claims that China’s massive military and nuclear build-up puts it on track to invade Taiwan by 2027.

Chart: USDCNY and USDCNH daily

Source: Investing.com