October 16, 2024

- GBPUSD slumps after weak inflation numbers.

- Risk sentiment turns modestly negative.

- US dollar traded with a bullish bias overnight.

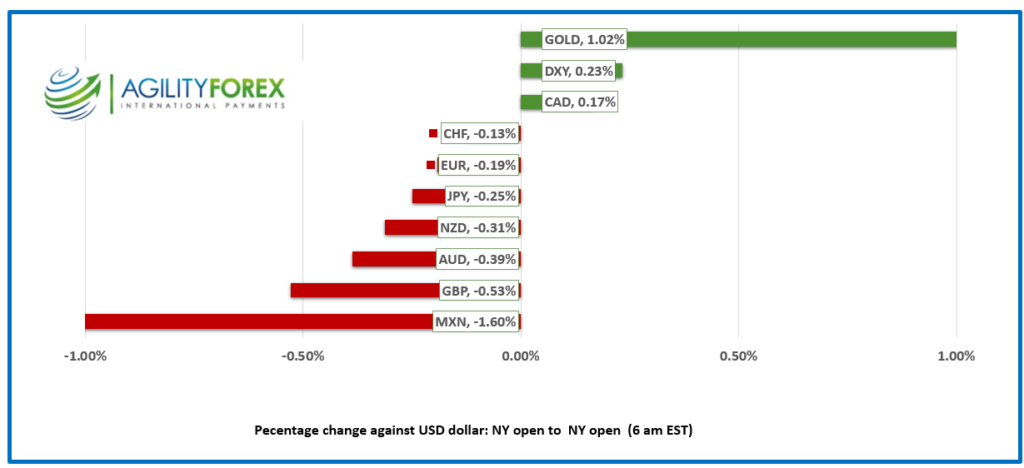

FX at a Glance

Source: IFXA/RP

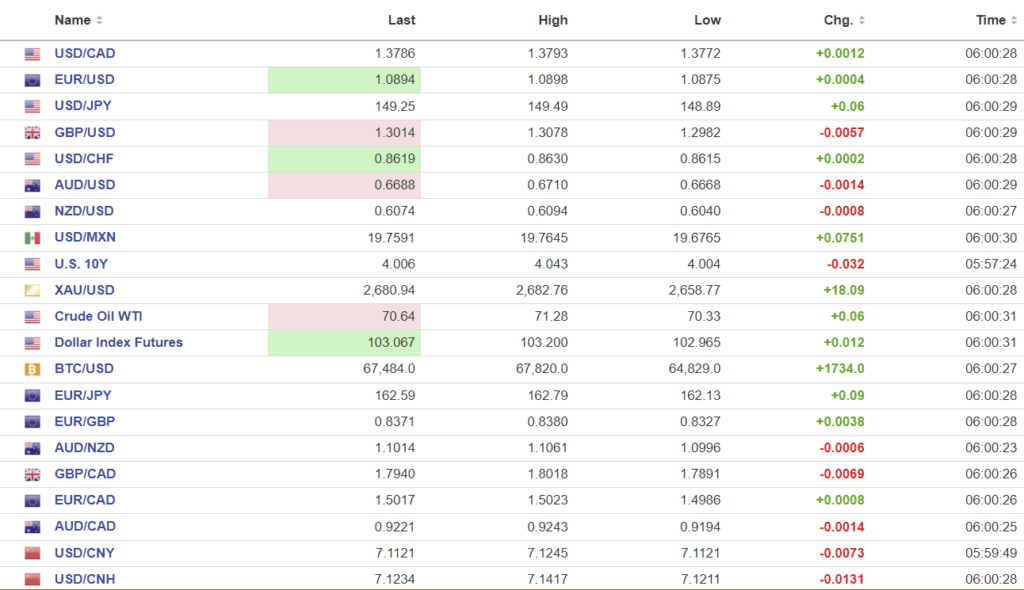

USDCAD open 1.3786, overnight range 1.3772-1.3793 close 1.3776

USDCAD is consolidating its recent gains in a 1.3772-1.3793 range. Yesterday’s soft inflation data combined with Friday’s weak employment report have traders anticipating two BoC 50 bp rate cuts by year end. The retreat from yesterday’s 1.3841 peak has more to do with profit-taking than a change in sentiment. USDCAD needs to ease its “overbought condition” before resuming its uptrend.

The only domestic data on tap are Housing Starts and Manufacturing sales, neither of which will have any impact on FX.

USDCAD technicals

The intraday USDCAD flipped to bearish with the break below 1.3790 breaching the floor of the two-week uptrend channel. A decisive move below this level suggests further losses to the 1.3690 support area.

Longer term, the June 2021 uptrend is still intact while prices are above 1.3460.

For today, USDCAD support is at 1.3760 and 1.3730. Resistance is at 1.3810 and 1.3850

Today’s Range 1.3760-1.3830

Chart: USDCAD 4 hour

Source: Investing.com

If You Tell More Than One Person, It’s Not a Secret

Israel has been wreaking havoc on terrorist enclaves throughout Gaza and Lebanon since Iran facilitated the Hamas attack on Israeli women and children over a year ago. The Biden administration has complained vociferously about Israel not keeping the White House informed of their planned actions. The US was as surprised as Hezbollah when pagers and walkie-talkies exploded simultaneously. So, in the interest of appeasing a key ally, Israel decided to let the White House know their planned targets for the imminent retaliation raid on Iran. That was a mistake. The Israeli Prime Minister was gobsmacked to read a Washington Post headline: “Netanyahu tells U.S. Israel will strike Iranian military instead of oil or nuclear sites.” Hmmm, on to Plan B, then?

Oil Traders Caught Wrong-Footed

Oil traders quickly bailed on long crude positions on Monday and Tuesday, with WTI settling near the bottom of its 70.33-71.28 overnight range. The OPEC and IEA forecasts predicting an oil glut in 2025, combined with weak demand from China, more than offset OPEC’s announcement that the planned phase-out of 2.2 million barrels/day of production cuts, beginning October 1, would be extended until the end of December. Analysts are relieved because the oil price retreat served to alleviate inflation spike concerns and the risk of higher interest rates risks that may have resulted. The WTI technicals are bearish below 72.00, looking for a break below 69.70 to extend losses to 66.00.

Global Equities Under Pressure

Wall Street closed with losses, and Asian equity indexes did the same. Japan’s Topix lost 1.21%, mainly due to the slumping yen, while Australia’s ASX 200 lost 0.40%. European bourses are all negative except for the UK FTSE, which rose 0.57% after a weak inflation report boosted rate cut odds. S&P 500 futures are flat while the US 10-year Treasury yield.

EURUSD

EURUSD stayed within a tight 1.0875-1.0898 range, hitting its session low during Asian trading hours. With limited Eurozone economic data available, traders were focused on the upcoming ECB meeting, where a 25 basis point rate cut is estimated to have an 80% likelihood.

GBPUSD

GBPUSD fell sharply, dropping from 1.3078 to 1.2982 after a softer-than-anticipated UK inflation report increased the likelihood of rate cuts by the Bank of England, with markets expecting 25 basis point reductions at the next two meetings. Core CPI fell to 4.6% from 4.9%, and inflation in services dropped to 4.9% from 5.6%. Meanwhile, the Retail Prices Index rose by 2.7%, falling short of the projected 3.1% increase, and Producer Prices also came in below forecasts. If GBPUSD drops below 1.2870, it could signal further losses down to 1.2770.

USDJPY

USDJPY remained in a narrow range between 148.89 and 149.49. Gains were capped after Bank of Japan board member Seiji Adachi indicated that Japan’s interest rates should rise slowly. In the US, 10-year Treasury yields slipped from 4.15% on Monday to 4.01% today.

AUDUSD traded with a negative bias in a 0.6668-0.6710 band, as concerns about China’s economic outlook persisted. Meanwhile, NZDUSD dropped from 0.6090 to 0.6040 after New Zealand’s Q3 CPI increased by 0.6% quarter-on-quarter, falling short of the 0.7% forecast but exceeding the previous 0.4% figure. This data did little to change expectations for a 50 basis point rate cut from the Reserve Bank of New Zealand next month.

USDMXN

USDMXN rallied from 19.6765 to 19.7790, extending yesterday’s rally after the IMF revised Mexican GDP growth down to 1.3% in 2025 from 1.5% in 2024. The ongoing uncertainty around Mexico’s planned judicial reforms underpinned the gains.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1191, (prev. 7.0830)

Shanghai Shenzhen CSI 300 fell 0.63% to 3831.59

Chart: USDCNY and USDCNH

Source: Investing.com