March 7, 2024

- ECB leaves rates unchanged, lowers inflation forecast

- Day 2 for Powell testimony.

- US dollar opens lower and is consolidating Wednesday’s losses..

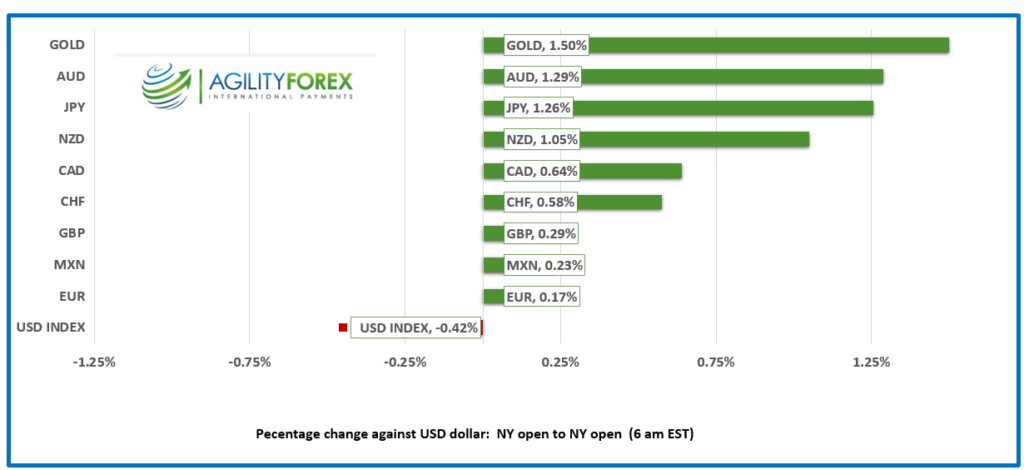

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3499-03, overnight range 1.3497-1.3526, close 1.3515

USDCAD is gnawing at support in the 1.3495-1.3505 area thanks to selling pressure following Fed Chair Powell’s remarks and soft employment data yesterday. The Bank of Canada monetary policy meeting was expected to be a non-event, and it was. Policymakers are concerned that “underlying inflation pressures persist” and therefore unlikely to cut Canadian rates until the end of the summer.

WTI oil prices drifted lower in a $78.33-$79.37 range, unable to sustain gains after the Energy Information Administration reported gasoline inventories fell by 4.46 million barrels last week. WTI is seeing lingering support from last Sunday’s announcement by Opec, that production cuts would be extended to the end of June.

Canada posted a small trade surplus in January (actual $0.5 billion vs December-$0.86 billion. Building Permits rose 13.5%.

USDCAD Technicals

USDCAD clearly rejected gains above 1.3605 and snapped the minor uptrend line (1.3540) yesterday. It is in the process of grinding through support levels between 1.3480 and 1.3500, which if successful will extend losses to the 1.3440-60 zone. 1.3440 is the 38.2% Fibonacci retracement level of the 2024 range. A decisive break above 1.3540 would negate the negative bias.

Longer term, a sustained move below 1.3480, suggests further losses to support in the 1.3340-60 area.

For today, USDCAD support is at 1.3480 and 1.3440. Resistance is at 1.3530 and 1.3560. Today’s range is 1.3460-1.3530

Chart: USDCAD daily

Source: Daily FX

G-10 FX

The Fed is in no hurry to cut rates, and neither is the Bank of Canada. They are content to bide their time to ensure that the downtrend in inflation is sustainable. Mr. Powell said as much in his testimony to Congress: “The committee does not expect that it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%.” That wasn’t anything new, but traders were relieved when Mr. Powell failed to mention anything about increasing rates. Powell is up to bat again today in front of the Senate.

With US rates having peaked and ADP and JOLTS job openings data suggesting the labor market was beginning to normalize, traders decided to sell US dollars. However, that may have just been weak, pre-Powell positions being unwound rather than the start of a new US dollar downtrend.

President Joe Biden holds a pep rally tonight, disguised as a State of the Union address and for most of the politicians, it will be the only exercise they get—rise, clap, sit, repeat.

US initial jobless claims were a touch higher than expected (217,000 vs 215,000) which supports the argument that the labour market is normalizing.

EURUSD is uninspired in a 1.0873-1.0907 range. The ECB left interest rates unchanged but the staff projections for 2024 inflation were lowered to 2.3% (in December 2.7%) and 2025 to 2.0% (December 2.1%. The inflation forecast reduction were widely anticipated and leave the door open to a June rate cut. The ECB press conference is just starting.

GBPUSD is drifting in a 1.2723-1.2763 band. Broad-based US dollar selling pressure is underpinning prices. Yesterday’s UK budget was a non-event for traders as most of the big announcements were leaked. GBPUSD technical are bullish above 1.2640.

USDJPY traded negatively in a 147.59-149.40 range. Sellers emerged after another round of comments from BoJ officials raised speculation for a rate hike in April.

AUDUSD rose from 0.6561 to 0.6616 due to higher commodity prices, robust China trade data and US dollar weakness.

NZDUSD rose from 0.6126 to 0.6163 due to broad US dollar weakness and slightly better Manufacturing sales data and Chinese trade numbers.

USDMXN drifted lower in a 16.8488-16.8899 range due to general US dollar weakness. Headline CPI was 4.4% y/y and 0.9% m/m which lifted USDMXN from 16.8510 to 16.8713. Some economists expect that the Mexican and US elections will limit USDMXN downside. The USDMXN technicals are bearish below 17.0950, looking for a test of 16.7900.

Bitcoin (BTCUSD) traded indecisively in a 63,846-67,612 range. Bitcoin topped 69,000 on Tuesday then retreated and consolidated following Powell’s testimony and comments from other officials suggesting that rates will remain at current levels for longer than expected.

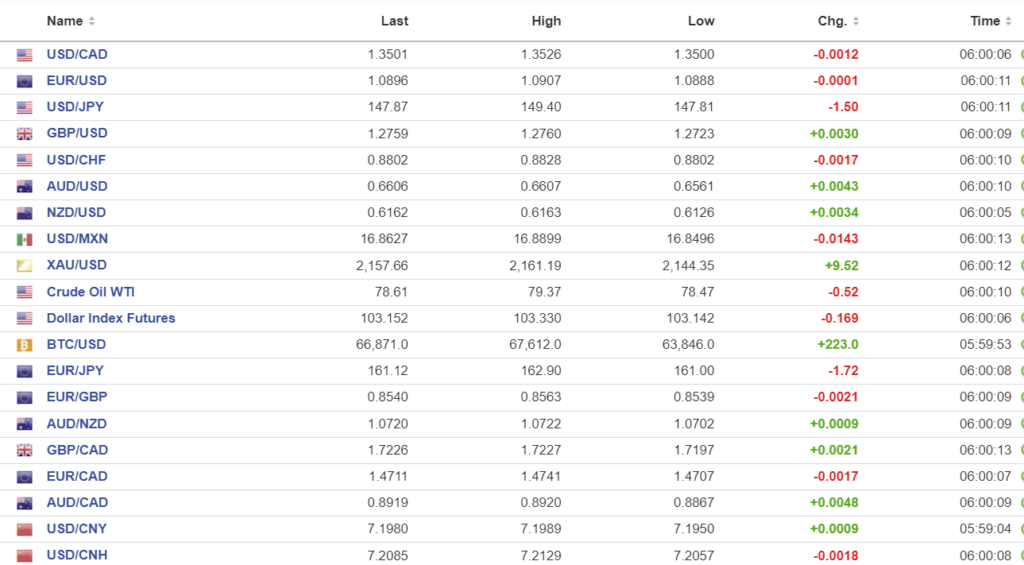

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1002 vs exp. 7.1898 (prev. 7.1016).

Shanghai Shenzhen CSI 300 fell 0.60% to 3529.72.

China’s Trade surplus surged in February, rising to $125.16 bio, easily topping the forecast of $103.7 bio and $75.34 billion in January.

China Foreign Minister Wang Yi complained that the US was imposing a “bewildering” level of trade curbs, which sounds even more riduclous in the wake of the China export data.

Chart: USDCNY and USDCNH daily

Source: Investing.com