Photo: hdclipart.com

April 3, 2023

- Opec cuts production by 1.0 million barrels/day.

- Recent data supports market view of Fed rate cuts before year-end.

- US dollar mixed compared to Friday open-CAD outperforms.

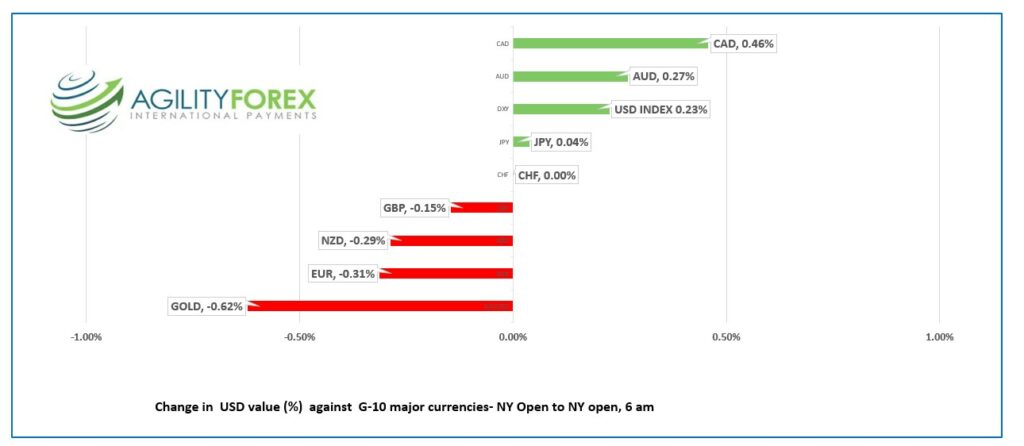

FX at a glance

Source: IFXA Ltd/RP

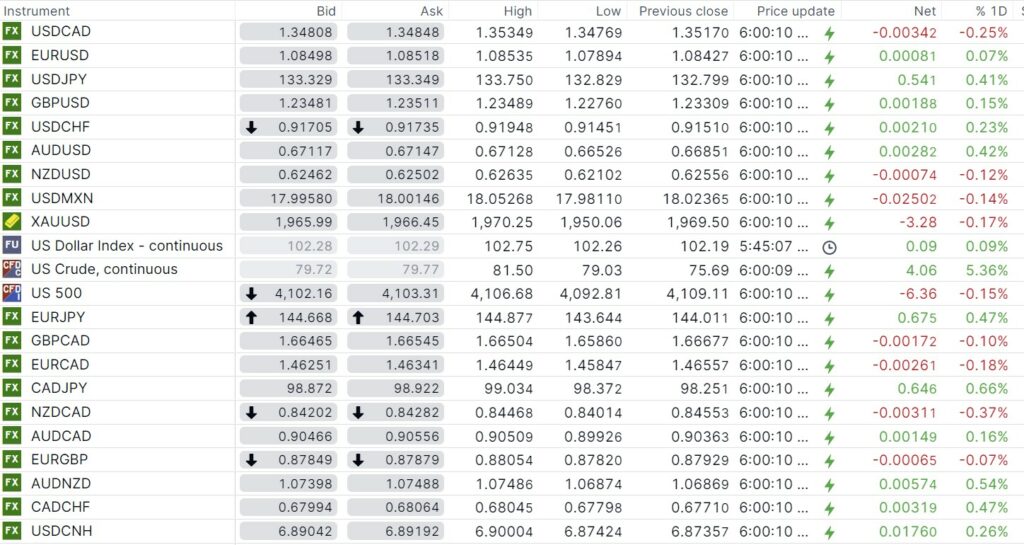

USDCAD Snapshot: open 1.3480-85, overnight range 1.3461-1.3535, close 1.3517

USDCAD extended its week-long slide overnight thanks to news Opec is cutting production by 1 million barrels/day.

The Cartel was obviously unhappy when WTI hit $70.00/b in March and are loathe to forgo cash benefits from the Western sanctions on Russia for invading Ukraine.

WTI oil prices gapped higher on the news, jumping from Friday’s NY close of $75.69/b to $81.50/b in early Asian trading. The WTI technicals suggest that the break above the year-long downtrend sets the stage for further gains to $94.00, representing the 50% Fibonacci retracement of the June 22-Apr. 23 range. Nevertheless, nature and markets abhor a vacuum meaning the gap from Friday’s close will be filled.

The March Labour Force survey (LFS) is released on Thursday, a day earlier than the usual Friday data drop because of the Good Friday holiday in Canada (US markets are open and NFP will be released as scheduled). The consensus forecast is for a loss of 4,200 jobs although Scotia Bank economists are forecasting a gain of 40,000.

USDCAD losses late last week were largely due to month-end and quarter end rebalancing flows and therefore the selling pressure will wane. It is hard to ignore the inflationary risks from higher oil prices which may cause those looking for early Fed rate cuts, to re-evaluate the view.

USDCAD Technical Outlook

The intraday technicals are bearish with the downtrend from last Monday intact while prices are below 1.3540, looking for a break of support in the 1.3440-60 area to extend gains to 1.3410. A break above 1.3540 will negate the downtrend and target 1.3570.

The daily USDCAD Fibonacci studies show the break below the 61.8% retracement level of the February/March range looking for a drop to the 76.4% level of 1.3417. In Addition, the move below the 100 day moving average at 1.3520 points to a visit to the 200 day moving average at 1.3376.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3520 and 1.3550.

Today’s range 1.3440-1.3520

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

It is going to be a short week for most of the G-10 countries as they shutdown for Good Friday. It is business as usual for the USA and it is also nonfarm payrolls day.

Opec may cause a short-term rethink for those expecting the first Fed interest rate cut in July. Higher oil prices and lower inflation are not compatible.

This weekend, Fed officials were doing their best to muddy the interest rate outlook. Fed Governor Lisa Cook and Governor Christopher Waller (both voters) delivered relatively dovish comments suggesting that tighter credit conditions and recent economic data point to lower inflation. But hedged themselves by saying things could change. All in all-, the comments were merely noise pollution.

Donnie Trump is visiting New York tomorrow. Normally, no one would care about the ex-president’s travel but this time he is arriving as a “perp,” to be arraigned for what is truly a “Trumped-up charge.”

Asian equity indexes shrugged off the Opec production cut, preferring to follow Wall Street’s lead and all the indexes closed with gains. European bourses shrugged off opening jitters and the UK FTSE 100’s rise of 0.82% is leading the others higher. S&P 500 futures are flat while the US 10-year Treasury yield is steady at 3.522%.

EURUSD traded in a 1.0789-1.0872 overnight after snapping a two-week rally when prices dropped below 1.0860 Friday. Prices have rebounded from the low following better than expected Eurozone Manufacturing PMI (actual 44.7, vs forecast 44.4), but need to extend above resistance at 1.0930 or risk another drop to 1.0790.

GBPUSD mirrored EURUSD moves, trading in a 1.2276-1.2367 range. UK Manufacturing PMI was a tick below the forecast at 47.8, but the results were ignored.

USDJPY rallied than sank, trading in a 132.83-133.75 range and it is sitting at 133.08 in NY. The Tankan Survey showed Large Manufacturers Sentiment index fell for the 5th quarter in a row. However, prices got a bit of a boost from a bit of US dollar demand following the Opec news.

AUDUSD rallied from 0.6653 to 0.6732 in NY buoyed by better than expected House Price data. The RBA monetary policy decision is tomorrow with economists evenly divided between unchanged and a 25 bps hike.

Today’s US data included ISM Manufactguring PMI.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

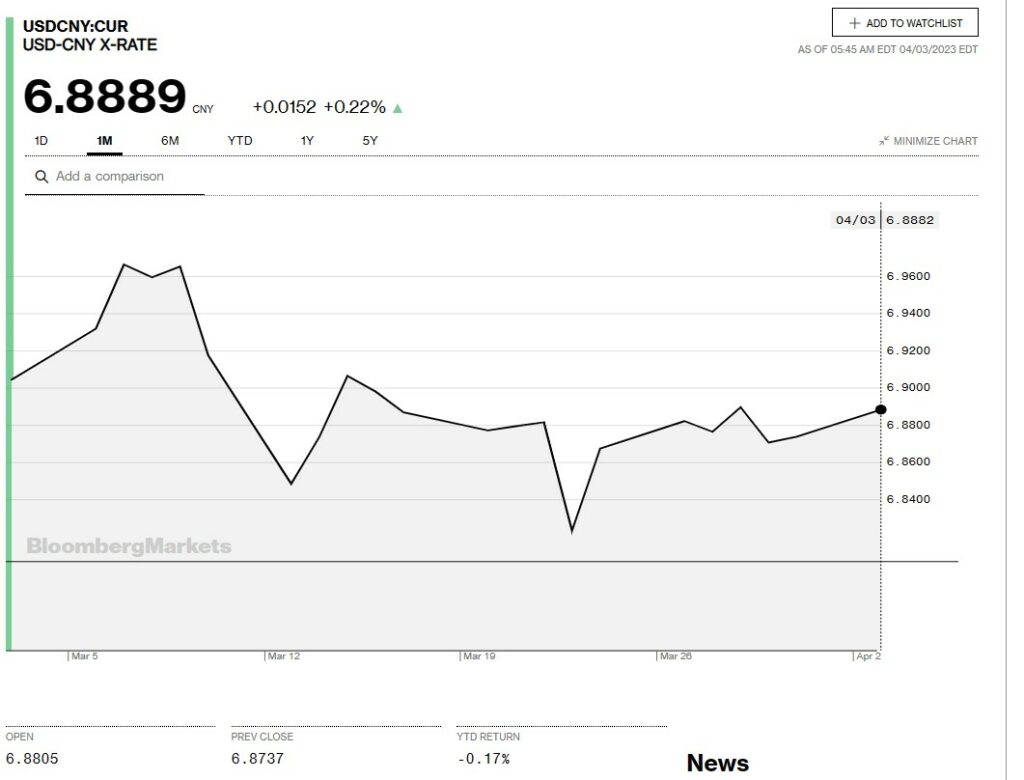

China Snapshot

Bank of China Fix: 6.805, Previous: 6.8717

Shanghai Shenzhen CSI 300 rose 0.98% to 4090.57.

March Caixin Manufacturing PMI 50.0 (forecast 51.7, previous 51.6)

Chart: USDCNH 1 month

Source: Bloomberg