Photo: wikimedia commons

March 6, 2023

- Busy week with Powell testimony Tuesday, BoC decision Wed, Canada, and US jobs data Friday.

- Euro area Retail Sales and Investor Confidence survey weaker than expected.

- US dollar modestly higher from close-opens mixed compared to Friday morning.

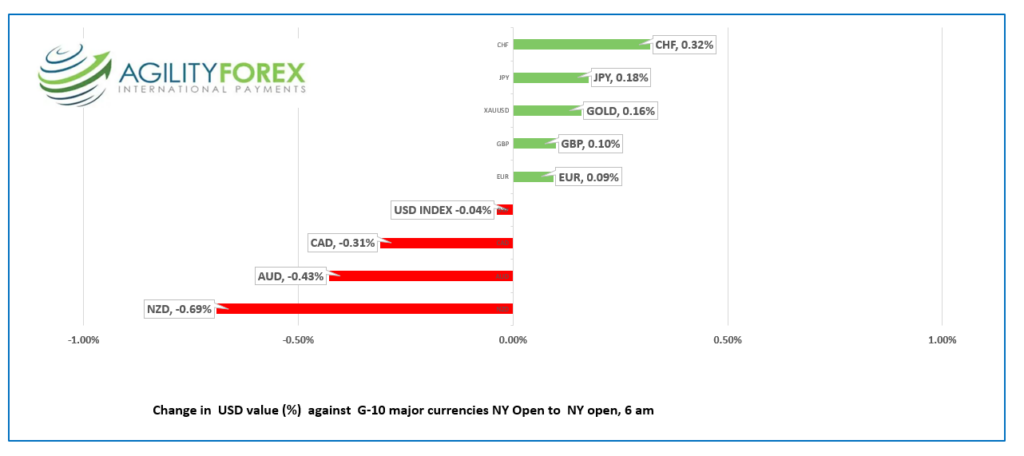

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3604, overnight range 1.3584-1.3627, close 1.3600

USDCAD continues to dance inside a narrow 1.3560-1.3660 range while trading with a modest bid in early NY.

The Bank of Canada will leave rates unchanged at tomorrow’s meeting. Governor Tiff Macklem said they would at last months meeting, and it is too soon for him to change his mind. There will not be a press conference either which suggests a rather uneventful statement.

Nevertheless, a dovish BoC in the face of a more aggressive Fed points to further gains for USDCAD.

WTI oil prices continued to see-saw in a $72.-$82.00/barrel range. Prices retreated from the peak following China’s latest GDP growth forecast but got some support after Saudi Arabia said it would raise prices for rude shipments to Asia.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3570, looking for a break above resistance in the 1.3680-1.3710 zone to extend gains to 1.3860. A break below 1.3570 targets 1.3540 then 1.3510.

The weekly USDCAD chart is bullish following the break of the downtrend line from October 2022 which has hung a target on the 1.4000 area.

For today, USDCAD support is at 1.3570 and 1.3530. Resistance is at 1.3660 and 1.3690.

Today’s range 1.3570-1.3660

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

In Greek mythology, Pandora opened a jar and unleased evils upon the world. The woke cohort got hold of the story sometime in the 16th century and the jar became a box, while the evils became blessings.

This week, Pandora’s box is now Pandora’s Calendar, and it contains a list of potential evils or blessings for financial markets. None of them are on tap today.

Chinese trade data, the RBA rate decision, and Fed Chair Jerome Powell’s testimony to Congress are on Tuesday. The Bank of Canada rate decision is center stage on Wednesday and Haruhiko Kuroda ends his 10-year governorship of the Bank of Japan on Friday. US and Canadian employment reports are also due Friday.

China announced a lower than expected 2023 GDP growth target of 5.0% at the Peoples National Congress. However, analysts suggest the target was chosen to help the new incoming policymakers achieve their policy goals.

Russian troops are in the process of gaining control of the Ukrainian city of Bakhmut which is a big deal if you are Ukrainian but a non-event for FX and equity markets-for now.

Markets are tentative ahead of Powell’s speech. The major Asian equity indexes closed with gains with Japan’s Nikkei 225 index rising 1.11%. European bourses are posting small gains except for the UK FTSE 100 index which is down 0.35%. S&P 500 futures are modestly negative, having fallen 0.15%.

EURUSD rallied in Asia, rising from 1.0617 to 1.0656 in Europe, then dropped to 1.0635 in NY after weak economic data. The Sentix Investor Confidence survey was -11.1 (forecast -8.6, previous -8) and February Eurozone Retail Sales fell 2.3% y/y (forecast 1.9% y/y.

EURUSD was supported by hawkish comments from ECB Chief Economist Philip Lane who warned of further rate hikes beyond the expected 50 bp bump slated for March 16.

GBPUSD traded in a 1.1994-1.2047 range overnight and dipped to 1.2004 in early NY. The currency continues to suffer from BoE Governor Andrew Bailey’s dovish comments last week in the face of the hawkish outlook for the ECB and the Fed. The intraday GBPUSD technicals are bearish below 1.2080 and looking for a break of support at 1.1910 to extend losses to 1.1830.

USDJPY extended Thursday’s decline from 137.07 to 135.38 in Asia before recouping some losses and reaching 136.18 in NY. The retreat was due to the slide in the US 10-year Treasury yield from 4.072% Friday to 3.93% today, However, caution ahead of Powell’s congressional testimony is underpinning prices.

AUDUSD is trading at the bottom of its 0.6718-0.6768 range due to lower commodity prices following China’s tame GDP growth forecast. The RBA is widely expected to hike the OCR rate by 25 bps to 3.60%.

There is no US data of note.

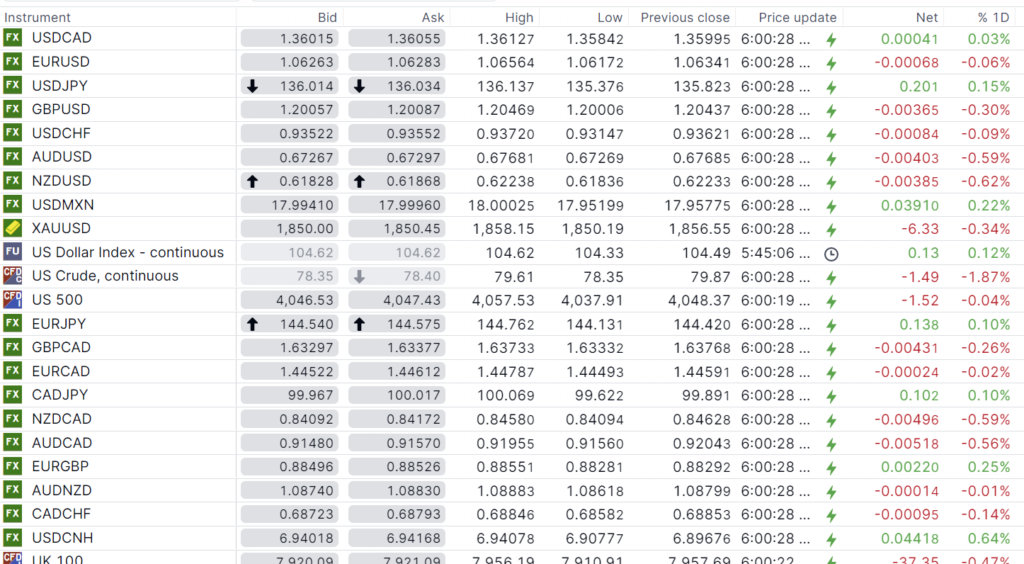

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Bank of China Fix: 6.8951, Previous: 6.9117

Shanghai Shenzhen CSI 300 fell 0.52% to 4109.01.

China sets lowest growth target in 25 years, aiming for GDP of 5.0% in 2023, and targets inflation around 3.0%. China plans to increase defence spending to 7.2% from 7.1%.

Chart: USDCNY 1 month

Source: Bloomberg