Source: Freepik

- Traders licking wounds after Tuesday’s rout

- US Aug PPI dips to 8.7% (July 9.8%)

- US dollar soared yesterday, consolidated overnight

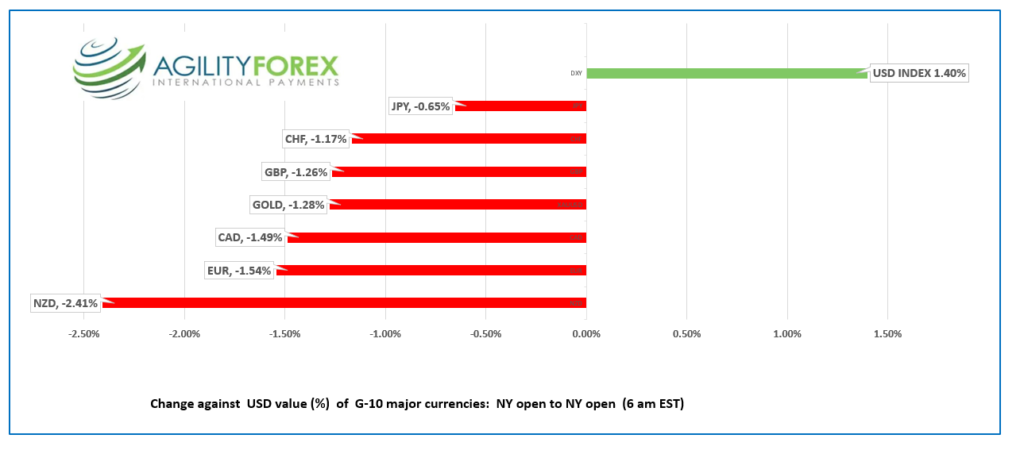

FX at a glance:

Source: IFXA Ltd/RP

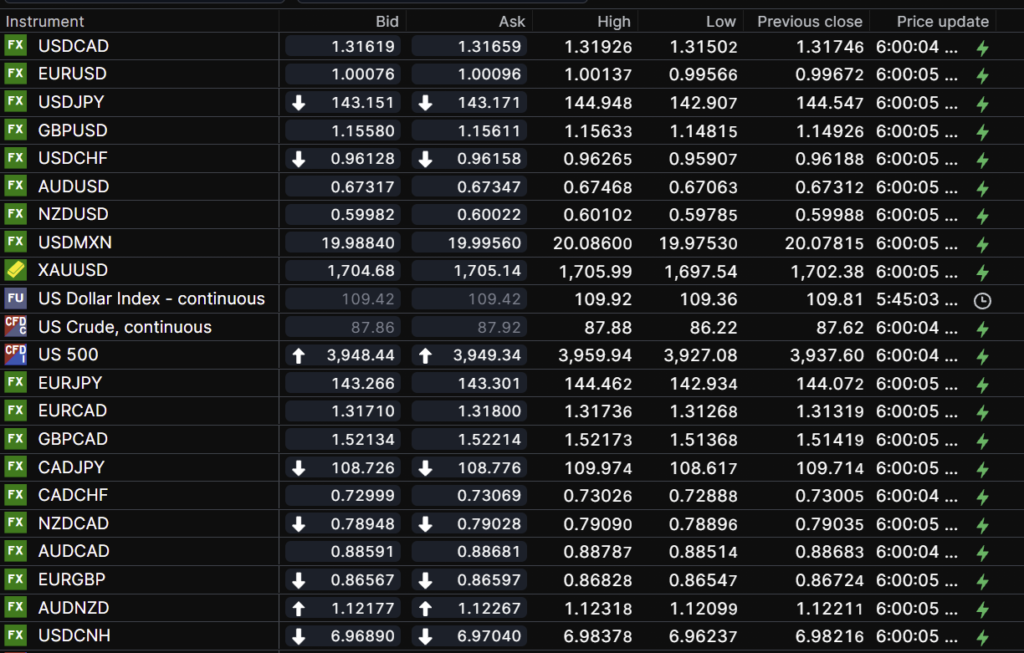

USDCAD Snapshot: open 1.3162-66, overnight range 1.3150-1.3204, close 1.3175

USDCAD peaked at support early yesterday before being punted to major resistance after the US inflation data. The rally was exacerbated by positioning as many traders convinced themselves that the Fed hiking rates to slightly above neutral, was all that was needed to tame inflation. They also ignored the inflation lessons from the 1978 inflation crisis.

WTI oil snapped a week-long uptrend when prices dropped below $87.70/b, yesterday, then consolidated in a $86.22-$87.97/b range overnight. Prices received marginal support after API reported US crude inventories rose 6.03 million barrels in the week ending September 9.

Opec is unhappy with current oil prices. The greedy cartel claims the latest price pressures are because of “erroneous signals” saying that the paper and physical markets have become disconnected. Some traders view the comments as a signal Opec will reduce production to boost prices.

Canada Manufacturing Sales for July fell 0.9% as expected and well below the -0.1% drop in June.

USDCAD Technical outlook

The intraday USDCAD are bullish following the break above 1.3030 yesterday which snapped ta week-long downtrend. The subsequent move above the 1.3090 level opened the door to further gains to the 2022 peak of 1.3203. A decisive move above 1.3220 targets 1.3420. A retreat below 1.3090 suggests further 1.3000-1.3200 consolidation.

For today, USDCAD support is at 1.3140 and 1.3090. Resistance is at 1.3210 and 1.3230. Today’s range: 1.3140-1.3220

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The market version of Goldilocks and the Dollar Bears ended with Goldilocks devouring the bears.

Yesterday’s hotter-than-expected US CPI report (actual 8.3% y/y vs forecast 8.1%, Core 0.6m/m vs forecast 0.3%) was a nasty intrusion on the “inflation has peaked” narrative, and those that drank that Kool-ade, are a tad worse for wear.

By the end of the day, the Dow Jones Industrial Average had dropped 1276 points while the S&P 500 index fell 4.32%. The 10-year Treasury yield soared from 3.30% pre-CPI to 3.458%, then consolidated the gains in a 3.404%-3.458% overnight.

The inflation results convinced analysts and economists the Fed would be raising the fed funds rate by 75 bps on September 21, while the odds for a 100 bp hike jumped from near zero to 31%.

Asian equity indexes joined the stampede lower, with a 2.78% plunge in Japan’s Nikkei 225 leading the pack. The Australian ASX 200 fell 2.58%.

European traders are less pessimistic. The major bourses are in the red but above the session lows. The UK FTSE 100 is the worst performer, losing 0.73%, partly due to the UK inflation data. Bottom pickers are at work in the US equity futures market. The S&P 500 futures have gained 0.28%, while DJIA futures are 0.17% higher.

The US Bureau of Labor Statistics reported “Producer Price Index declines 0.1% in August, goods fall 1.2%, services increase 0.4%.” The results had a negligible impact on markets.

EURUSD traded in a 0.9957-1.0023 range overnight. The single currency’s attempt to recoup yesterday’s losses stalled at 1.0023 and prices fell to 1.0000 when the 10-year Treasury yield ticked higher to 3.46% and drove S&P 500 futures from it overnight peak.

EU Commission President Ursula von der Leyen declared Russia’s invasion of Ukraine as a “war on our economy, a war on our values, and a war on our future.” She insisted sanction on Russia were “here to stay” and spoke of plans to tax excess energy company profits.

GBPUSD is attempting a rally after dropping from 1.1735 pre-US CPI to 1.1482 in Asia overnight.

GBPUSD rose after UK August CPI was lower than expected, rising 9.9% in July (forecast 10.2% y/y). However, the enthusiasm was tempered as PPI and Retail Price Index data were softer than forecast. The Bank of England is expected to hike rates by 50 bp next week.

USDJPY is in a tug of war between rising Treasury yields and Bank of Japan FX intervention risks. Prices peaked at 144.95 then dropped to 142.95 in NY due to more intervention threats from BoJ policymakers.

AUDUSD traded defensively in a 0.6706-0.6747 range while NZDUSD dropped from 0.6010 to 0.5979 and is the worst performing currency pair since Tuesday’s NY open.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

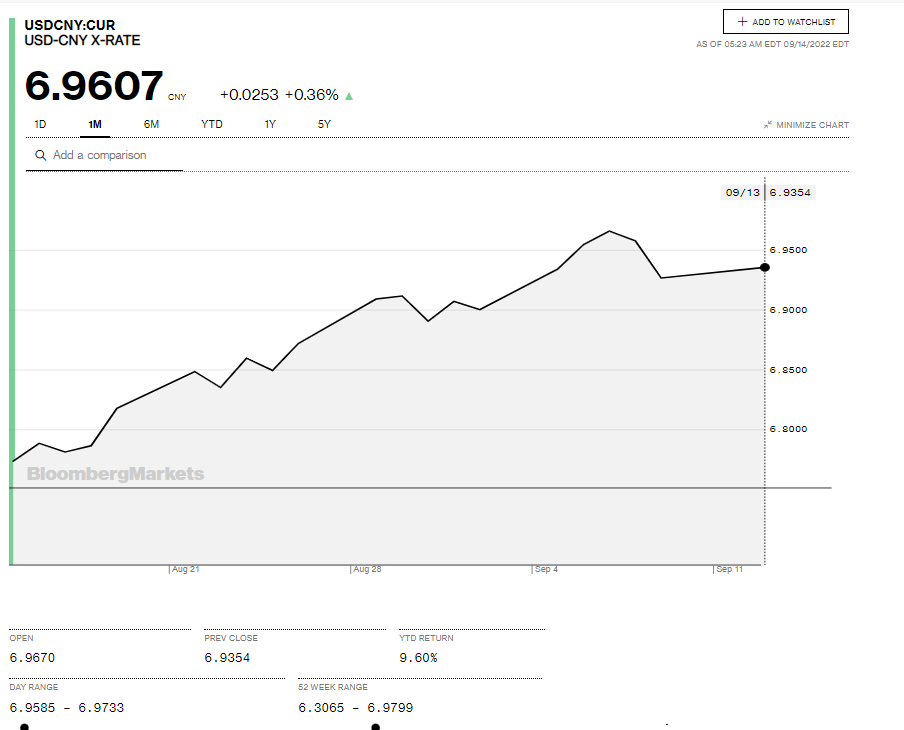

China Snapshot

Today’s Bank of China Fix: 6.9116, previous 6.8928

Shanghai Shenzhen CSI 300 fell 1.11% to 4,065.36

Chart: USDCNY 1 month

Source: Bloomberg