Photo: hdclipart.com

April 12, 2023

- US Inflation data comes in as expected.

- Bank of Canada monetary policy meeting will be benign.

- US dollar opens mixed, trades in narrow bands overnight.

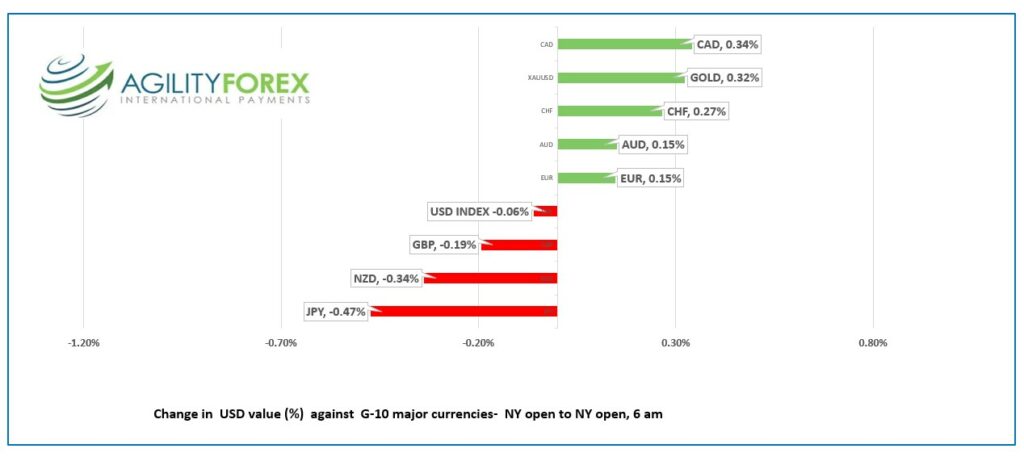

FX at a glance

Source: IFXA Ltd/RP

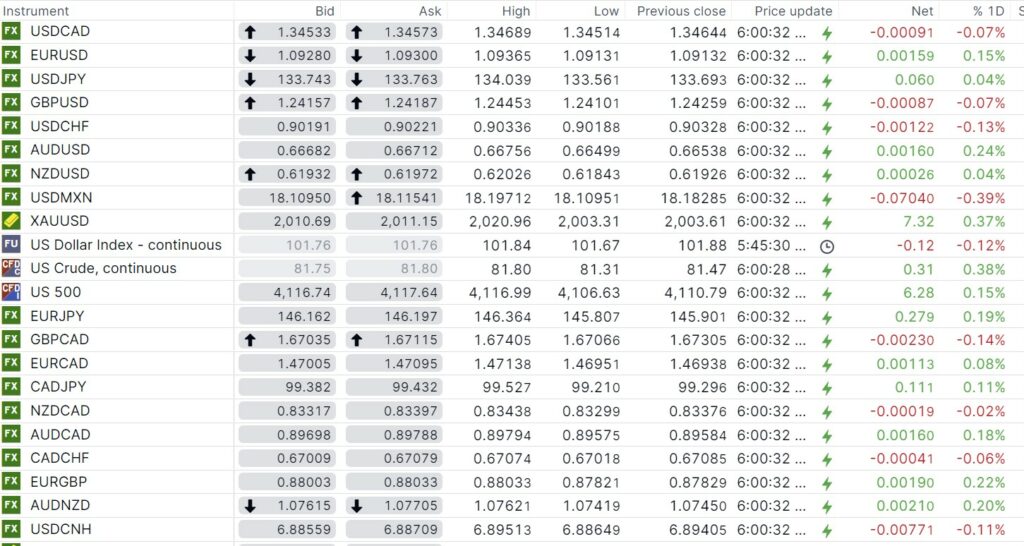

USDCAD Snapshot: open 1.3453-58, overnight range 1.3451-1.3469, close 1.3464

The Bank of Canada monetary policy meeting statement and quarterly Monetary Policy Report are due today. The policy statement is expected to be benign, and little changed from the March 8 statement. The changes will be seen in the MPR forecasts which should see an upside tweak to GDP growth while CPI estimates are close to unchanged.

USDCAD is seeing added selling pressure from WTI oil prices sticking above $80.00/barrel.

The Energy Information Administration (EIA) Short-term energy Outlook (STEO) report was released yesterday. The EIA said “We expect that world oil production and demand for petroleum products will be relatively balanced this year. The biggest risk to our April forecast is slower-than-expected economic growth.

The domestic economic calendar is empty.

USDCAD Technical Outlook

The intraday technicals are bearish below 1.3490, looking for a break below 1.3440 to extend losses to the 1.3390-1.3400 area. A break above 1.3490 suggests another test of the 1.3550-60 resistance area.

The downtrend from March 10 on a daily chart is intact while prices are below 1.3630 with a move below the 200-day moving average (1.3394) setting the stage for a test of 1.3230.

For today, USDCAD support is at 1.3430 and 1.3390. Resistance is at 1.3510 and 1.3550.

Today’s range 1.3400-1.3500

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FX markets didn’t get a lot of joy from today’s US inflation data. Headline CPI fell to 5.0 y/y from 6.0% last month while the more important Core-CPI data rose 0.4% m/m and 5.6% y/y as expected. The results did nothing to dissuade the Fed from raising rates another 25 bps on May 3.

Traders continue to expect that the Fed will be cutting interest rates as early as September even though the data doesn’t support such a move.

Fed officials continue to muddy the waters. Cleveland Fed President Neal Kashkari suggested that inflation a larger concerns than possible economic woes from banking stress. Other FOMC officials argue for at least one more rate hike is needed before pausing, while none of them advocate cutting rates.

The interest rate debate will get more fuel when the minutes from the March 22 FOMC meeting are released, this afternoon.

EURUSD traded in a 1.0913-1.0937 range, with traders positioning for a soft US CPI report that knocks the greenback lower and drives EURUSD through resistance above 1.1000. A drop below 1.8650 would negate the upward pressure and target 1.0670.

GBPUSD traded quietly in a 1.2410-1.2445 range. Traders are cautious after ING economists suggested that the risk that the Bank of England pauses hiking rates in May is under-priced by markets. The GBPUSD uptrend since the beginning of March is intact while prices are above 1.2370. A move below that level will extend losses to 1.2230.

USDJPY bounced inside a 133.56-134.04 range. The lingering concern that the BoJ may phase out its ultra-easy monetary policy and soft US treasury yields are reinforcing resistance in the 1.0420 area. March PPI rose 7.2% y/y compared to the forecast of 7.1% (previous 8.3%).

AUDUSD traded narrowly in a 0.6650-0.6676 range supported by general US dollar weakness and speculation that the RBA will hike rates by 25 bps at the next meeting

NZDUSD traded quietly in a 0.6184-0.6203 range. Electronic card retail sales rose 0.7% m/m and 15.5% y/y in March, which supports the case for another 25 bp rate hike on May 24.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

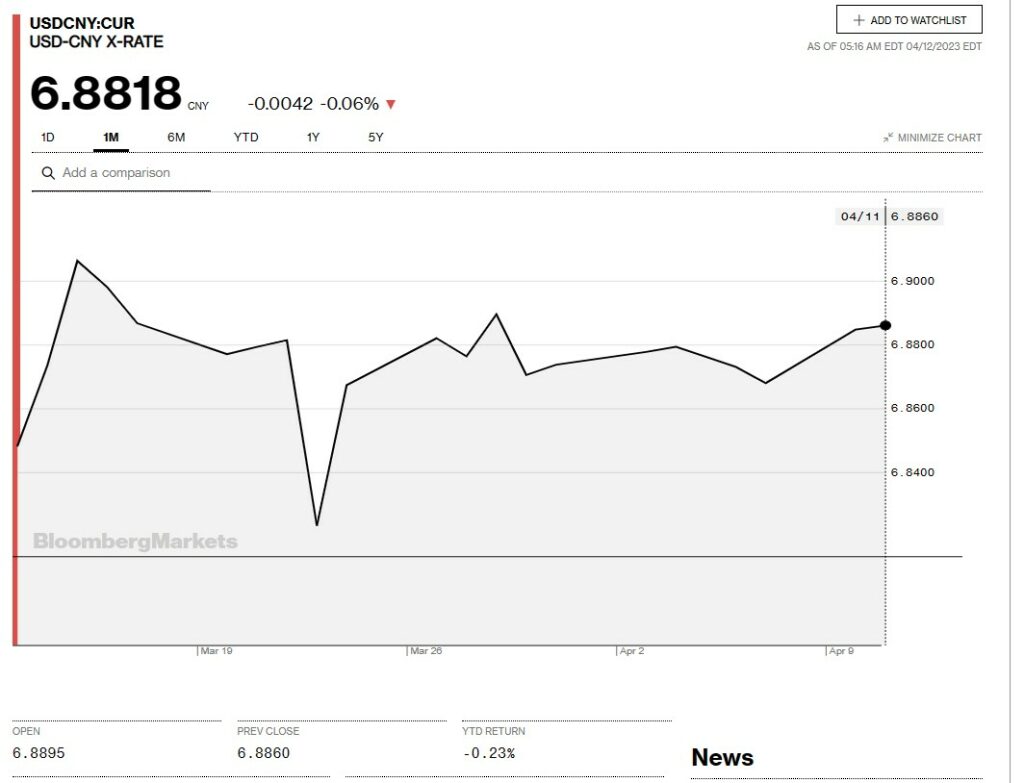

China Snapshot

Bank of China Fix: 6.8854, Previous: 6.8882

Shanghai Shenzhen CSI 300 fell 0.07% to 4097.29.

Chart: USDCNY 1 month

Source: Bloomberg