January 24, 2024

- PBoC pre-announces 0.5% RRR cut, effective Feb. 5.

- Bank of Canada monetary policy meeting and MPR today.

- US dollar trading with negative bias.

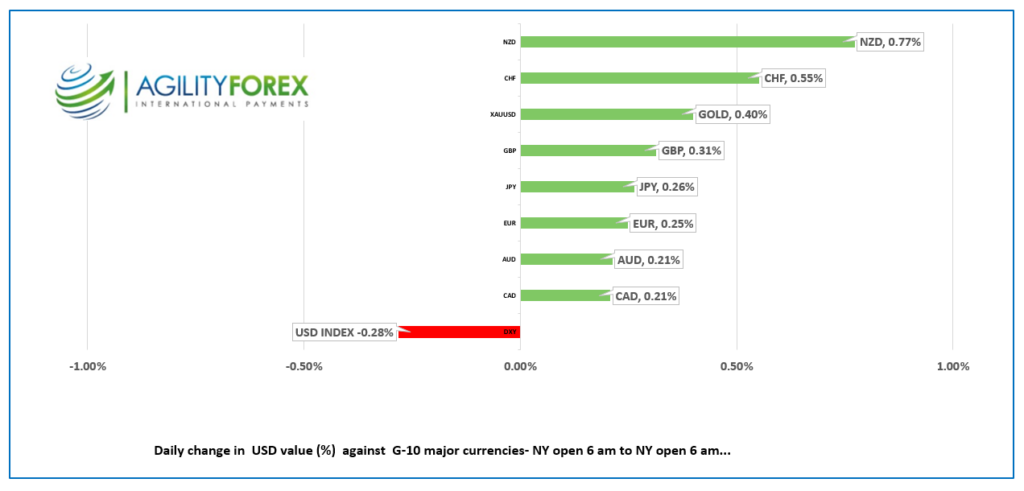

FX at a glance

Source: IFXA

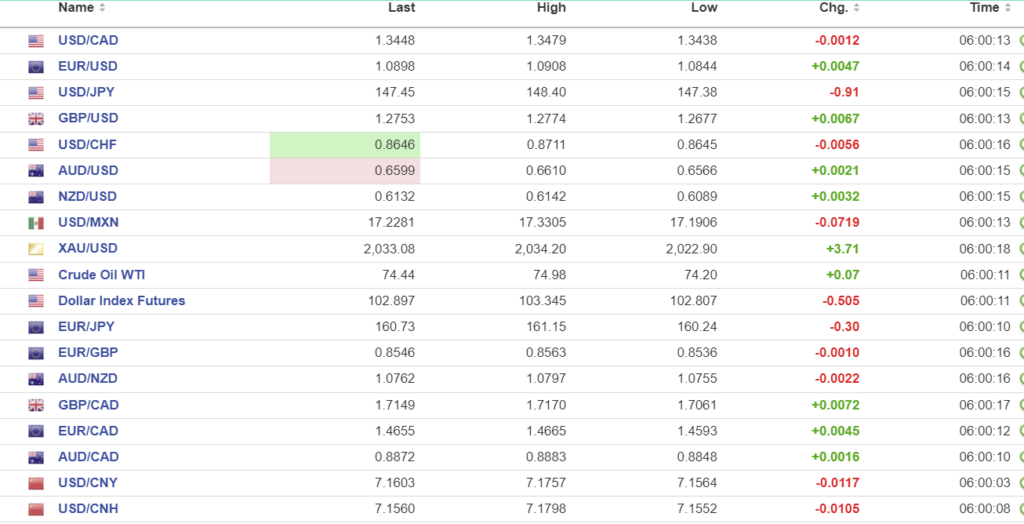

USDCAD Snapshot: open 1.3446-50, overnight range 1.3436-1.3479, close 1.3461.

USDCAD is chopping about inside the overnight range but lacking conviction ahead of today’s Bank of Canada quarterly Monetary Policy Report (MPR) and interest rate statement. USDCAD may be seeing a bit of negative pressure in anticipation of hawkish comments from Governor Macklem. However, they should be ignored as it is extremely unlikely that he will raise rates. Analysts will be more interested in the MPR to see what the BoC expects for growth inflation and employment in the next year.

Rising oil prices may be acting as a drag on USDCAD gains. WTI traded in a $74.12-$74.98 range with the peak seen in Asia. The weekly API crude stocks report showed inventories falling by 6.674 million barrels.

USDCAD Technicals:

The USDCAD technicals are bearish. USDCAD snapped its July uptrend at the end of November when it broke below 1.3660. The downtrend from that day continues to guide prices lower as long as they are below 1.3540. A break below 1.3405 will negate the intraday uptrend and set the stage for further losses to 1.3340, then 1.3260. A decisive breach above 1.3540 targets the November peak of 1.3900.

For today, USDCAD support is at 1.3410 and 1.3370. Resistance is at 1.3490 and 1.3550. Today’s range is 1.3410-1.3510.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

Risk sentiment has turned positive, at least for today. A slew of strong earnings reports from tech companies has given European equities and S&P 500 futures a lift. Netflix (NFLX: Nasdaq) is up over 10% in pre-market trading after the company added more subscribers than expected. In addition, the People’s Bank of China (PBoC) pre-announced that the Reserve Requirement Ratio (RRR) for large banks would be cut by 0.5% to 10.0% on February 5. Investors are hoping the central bank’s actions will jump-start the stagnant economy and boost global growth.

New Hampshire Republicans have pretty much anointed former President Donald Trump to be future President Trump. They have decided that the world does not have enough loud-mouth narcissists ruling countries. Republicans of all stripes are drooling over the opportunity to be named “most-favoured sycophant” while recently convicted allies are praying for pardons.

Asian equity indexes closed modestly higher except for Japan’s Nikkei 225 index. Talk of BoJ tightening helped push the index down 0.80%. Australia’s ASX was close to unchanged with investors seemingly unimpressed with the 3.56% rally in the Hong Kong Hang Seng sparked by the PBoC news.

European bourses have risen sharply, led by a 1.20% gain in the German Dax and supported by Wall Street earnings and Eurozone data. SP500 futures have risen 0.43%. The US 10-year Treasury yield inched down to 4.11% from 4.142% at yesterday’s close.

EURUSD firmed in a 1.0844-1.0908 range. German and Eurozone PMI data remain in contraction territory, but optimists see signs that the data is bottoming out. The HCOB press releases pointed out that cost pressures were increasing which supports a hawkish outcome at tomorrow’s ECB meeting.

GBPUSD caught a flash-PMI bid and rallied from 1.2677 to 1.2774 before retreating to 1.2744 in early NY. The higher than expected Manufacturing (actual 46.6 vs forecast 44.8), Composite (actual 52.5 vs forecast 562.2) and Services (actual 53.8 vs forecast 53.2). Supply chain disruptions from Red Sea strife has pushed up prices and gives the BoE reason to delay planned rate cuts.

USDJPY traded negatively, falling from 148.40 to 147.38 in early NY. The selling pressure stems from fresh concerns that the BoJ will begin tightening as early as the March 18 meeting and because of steady to firm US Treasury yields.

AUDUSD inched higher in a 0.6566-0.6610 range, buoyed by the latest PBoC stimulus and preliminary PMI data suggesting the Australian economy will achieve a soft landing.

NZDUSD climbed to 0.6142 from 0.6089 after inflation rose 4.7% in December which was as expected but still too high to allow the RBNZ to cut interest rates.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

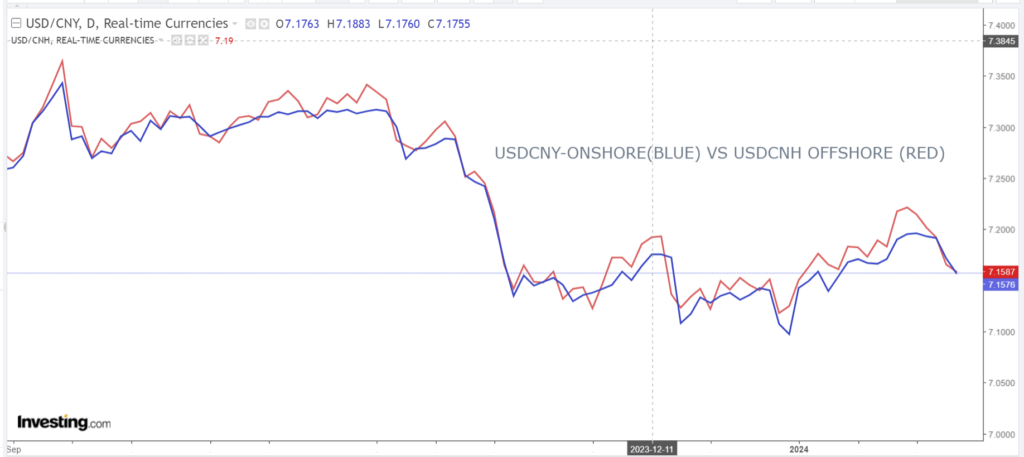

China Snapshot

PBoC fix: today 7.1053, expected 7.1825, previous 7.1117.

Shanghai Shenzhen CSI 300 rose 1.40% to 3277.11.

PBoC pre-announces a 0.5% cut in the Reserve Requirement Ration (RRR) for banks, from 10.5% to 10.0%, effective February 5.

Fun fact: (from John Authers, Bloomberg) Chinese and Hong Kong stocks in aggregate have erased more than $6 trillion in market value since their peak in 2021. That’s roughly equivalent to the entire market capitalization of Japan.

Chart: USDCNY and USDCNH daily

Source: Investing.com