Source: the accidentallocavore

- Bank of England hikes 75 bps to 3.0%

- Hawkish Fed lifts 10-year Treasury yield to 4.197%, Stocks sink

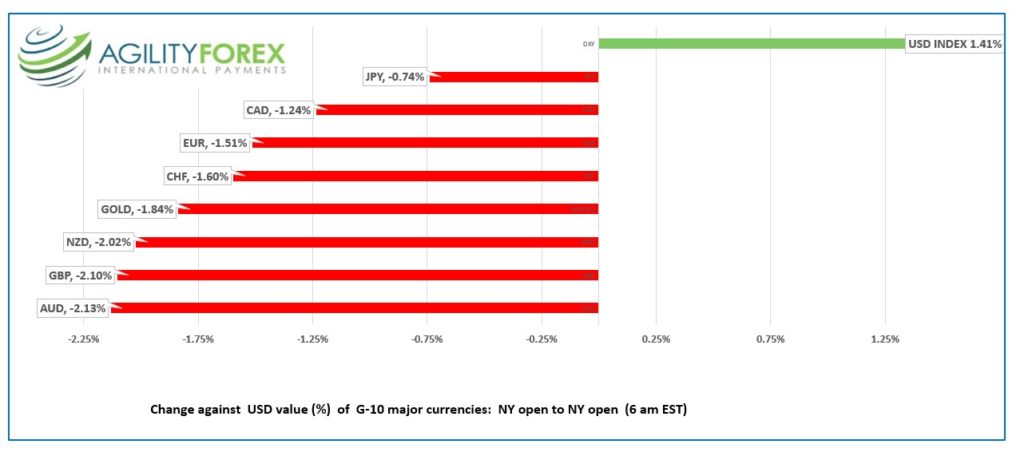

- US dollar opens bid across the board.

FX at a glance:

Source: IFXA Ltd/RP

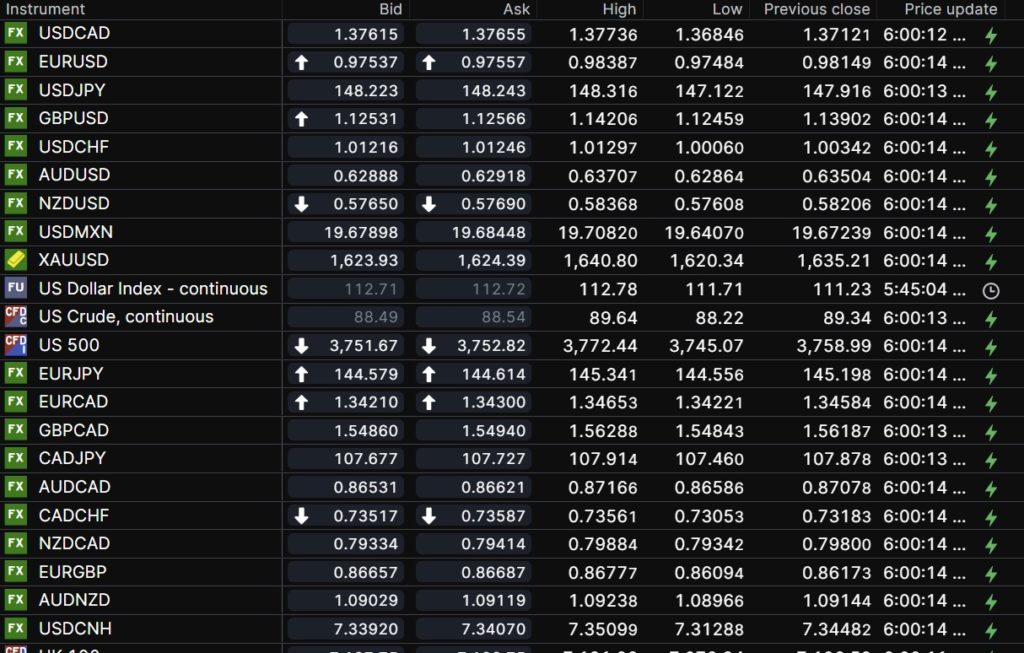

USDCAD Snapshot: open 1.3662-66, overnight range 1.3685-1.3796, close 1.3712

USDCAD dropped to 1.3549 from 1.3632 when the FOMC statement was released then soared to 1.3712 at the close, before accelerating higher overnight.

Traders and analysts listened to Powell’s press conference and decided that the Fed was far more hawkish than the statement implied and reacted accordingly.

USDCAD gains are underpinned by widening Can/US interest rate differentials as the Canadian 10-year government bond is 81.6 bps below the US 10-year T yield.

USDCAD may be facing some headwinds from steady to firm WTI oil prices which are trading at $88.64/b despite the broad US dollar strength.

Finance Minister Freeland delivers a fiscal update at 1:00 pm PT. She will talk fiscal responsibility while spending money.

Canadian Building Permits fell 17.5% in September compared to a 12% gain in August. Canada’s trade surplus widened to 1.14 billion a tad lower then expected.

USDCAD Technical outlook

The intraday USDCAD technicals flipped to bullish with the break above the 1.3650 and are looking to extend gains to 1.3810 then 1.3860. A drop below 1.3620 will negate the upward pressure and turn the focus to 1.3550.

Longer term, the latest price action is merely noise inside the 1.3550-1.3970 range that has controlled price action since September 22.

For today, USDCAD support is at 1.3720 and 1.3670. Resistance is at 1.3810 and 1.3850. Today’s range 1.3720-1.3820

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

FUBAR was one word to describe yesterday’s FOMC statement and Fed Chair Powell’s press conference. Markets reacted to the FOMC statement as if it were dovish due to this paragraph.

The FOMC statement said “In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

That’s because when Deputy Chair Lael Brainard used “cumulative tightening in a speech October 10 analysts were convinced she was suggesting a slower pace of rate hikes. She said, “it takes time for cumulative tightening to transmit throughout the economy and to bring inflation down.”

The immediate result to the statement was that the dollar plunged stocks soared, and Treasury yields fell.

Fed Chair Jerome Powel kiboshed any notion that the Fed was dovish. He said “it is very premature to be thinking about or talking about pausing our rate hikes. We have a ways to go. We need ongoing rate hikes to get to that level of sufficiently restrictive.”

Markets reversed rapidly. The US dollar index (USDX) rallied from its FOMC statement low of 110.33 to close at 111.23, while the S&P 500 index dropped from a statement peak of 3894.44 to close at 3759.69.

The carnage continued overnight.

Asian equity indexes followed Wall Streets lead with the Hang Seng index dropping 3.08% and Australia’s ASX 200 losing 1.84%.

European bourses are all in the red with price action muddled by the Bank of England meeting and contradictory comments from ECB officials. S&P 500 and DJIA Futures are modestly lower. Gold and oil prices fell on the back of the surging US dollar.

US weekly jobless claims were a tad better than expected at 217,000 but unchanged (before revisions) from last week.

EURUSD extended Wednesday’s losses and dropped from 0.9839 to 0.9731 in NY. ECB President Christine Lagarde made a bit of a case for lagging Fed actions. She said the ECB could not merely mimic the Fed because conditions were different in the Euro area, comprised of 19 countries. She did admit being influenced by the consequences of Fed actions, particularly with the exchange rate.

Meanwhile Norway’s Norges Bank raised its benchmark rate 0.5% to 2.50%, the highest level since 2009. The Bank justified the move citing high economic activity, low unemployment, and rising inflation.

EURUSD technicals are bearish below 0.9910.

GBPUSD plunged to 1.1199 from an overnight peak of 1.1421 in the wake of the Bank of England’s 75 bp rate hike which lifted the benchmark rate to 3.0%, its highest level since 2008. Two members voted for a lower hike. One wanted to lift rates just 0.25% while the other opted for a 50 bp bump. The BoE justified the rate increase because inflation was too high. The GBPUSD uptrend line from the end of September is intact while prices are above 1.1190 but the shorter-term downtrend is intact below 1.1540. A downside break targets 1.1000.

USDJPY rallied from 147.12 to 148.42 due to broad US dollar strength, the hawkish comments from Powell, and the rise in the US 10-year Treasury yield to 4.197% this morning.

AUDUSD dropped from a Fed statement peak of 0.6483 to 0.6282 in NY. The contrasting interest rate outlooks between the RBA and the Fed are driving prices lower. Australia Services PMI rose to 49.3 from 49, but the news was ignored.

NZUSD traded in a 0.5757-0.5837 range overnight. RBNZ Governor Adrian Orr reiterated his “laser-like focus in getting inflation back to target.

ISM Services PMI is expected to have dipped to 55.5 from 56.7 in October.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

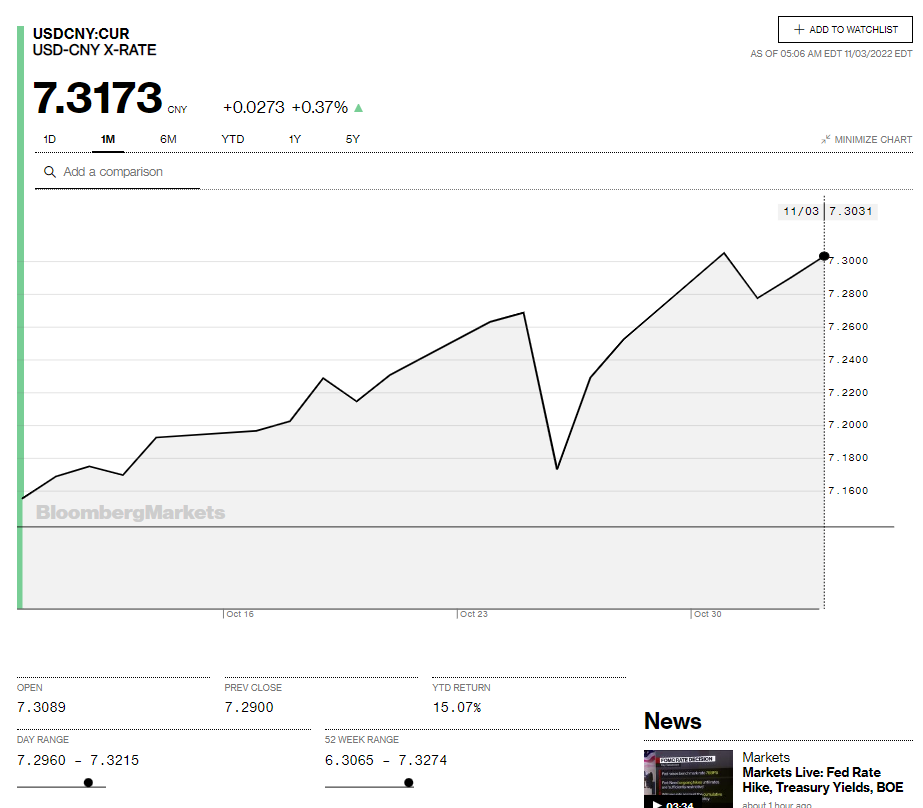

China Snapshot

Today’s Bank of China Fix: 7.2472, previous 7.2197

Shanghai Shenzhen CSI 300 fell 0.81% to 3647.90

Caixin October Services PMI 48.4, September 49.3

Hong Kong Monetary Authority hies base rates 75 bps, as expected

Chart: USDCNY 1 month

Source: Saxo Bank