October 1, 2024

- Powell comments sink odds of 50 bp rate cut on November 7.

- US employment data key to FX direction today.

- US dollar recoups earlier losses.

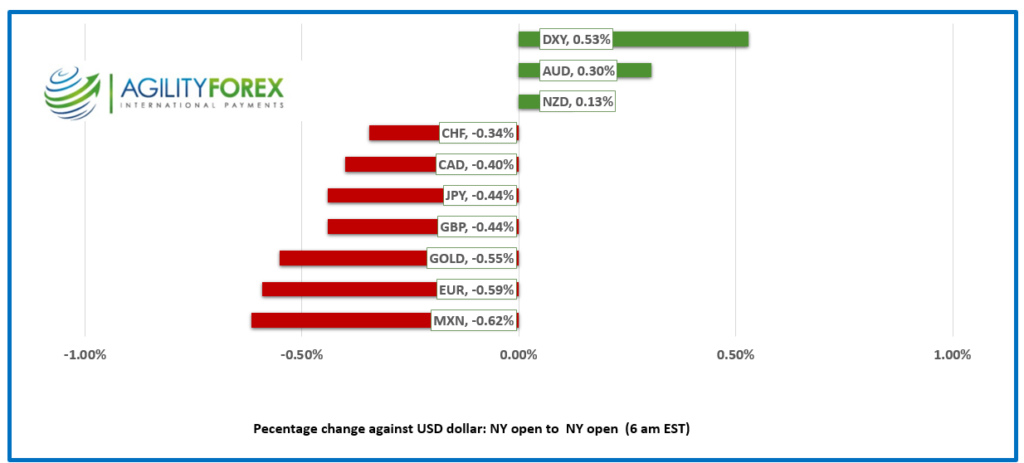

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3533, overnight range 1.3490-1.3540, previous close 1.3526

USDCAD traded with a bullish bias with traders ignoring last week’s China stimulus news which gave the other commodity currency bloc currencies (AUD, NZD) a bit of a boost. Friday’s GDP data which was a tad above consensus was ignored.

USDCAD is also underpinned by the downgraded risk of another 50 bp rate cut in November. The odds for a 50 bp cut dropped from 68% last week to 39.8% after Fed Chair Powell said he wasn’t in a hurry to trim rates.

WTI oil prices dropped to 66.34 from 68.43 in Asia and Europe but rebounded to 67.66. Opec’s promised production increase kicked in today and so far, Israel’s actions in Lebanon have not disrupted crude supplies.

Traders are focused on this week’s US employment data and hoping the data will provide fresh insight into the US rate outlook.

Today’s key data is the ISM Manufacturing PMI report (forecast 47.5, previous 47.2) ISM employment index (forecast 47 vs previous 46) and JOLTS Job openings . the Canadian calendar is empty.

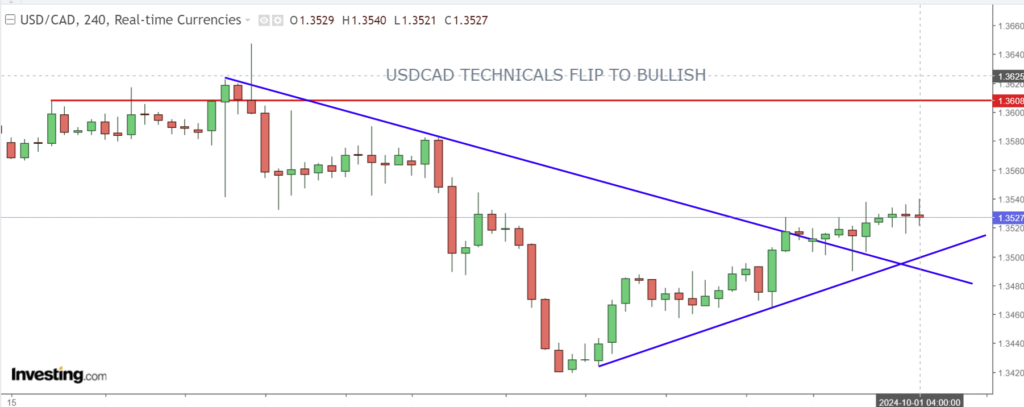

USDCAD technicals

The intraday USDCAD are bullish after the break above 1.3520 snapped a two-week downtrend line. The uptrend is intact above 1.3490 and is looking for a test of resistance at 1.3605.

Longer term, USDCAD gains may meet resistance in the form of the 200-day moving average 1.3596. but garner support from the year-to-date moving average at 1.3602

For today, USDCAD support is at 1.3505 and 1.3490. Resistance is at 1.3550 and 1.3590.

Today’s Range 1.3490-1.3560

Chart: USDCAD 4 hour

Source: Oanda.

Along Came Jones (Powell)

“And then along came Jones, tall thin Jones, slow walking Jones, slow talking Jones.” There was no dastardly villain threatening to saw “Sweet Sue” in half if he didn’t give her the deed to her ranch, but there was Fed Chair Jerome Powell saving US dollar bulls. He claimed that the Fed was in no hurry to cut rates as economic risks were two-sided. However, insider-trader and Atlanta Fed Governor Raphael Bostic said he was open to another 50 bp cut if the labor market showed weakness.

Good-bye Imports

International Longshoremen’s Association members launched a strike affecting dozens of ports from Texas to Maine. These terminals are responsible for about ½ of the USA’s import and export volumes. The Union is asking for a 77% wage increase over six years, which is totally reasonable in a 2.5% inflation environment—said no one. A prolonged action would result in shortages and higher prices.

Equities are Mostly Positive

Japan’s Topix rallied 1.69%, but that performance paled in the face of the 8.48% surge in the Shanghai Shenzhen CSI 300 index. Aussie traders were not as fortunate as the ASX 200 shed 0.74%. European bourses are higher, led by the UK FTSE 100 rising 0.34%. The French CAC-40 index is down 0.20%. S&P 500 futures are flat, and the US 10-year Treasury yield is at the bottom of its 3.742-3.797% range.

EURUSD

EURUSD traded poorly, dropping from 1.1209 Monday to 1.1085 in NY today. EURUSD sentiment soured due to a myriad of reasons, including dovish comments by ECB President Christine Lagarde hinting at faster rate cuts while Fed Chair Powell slammed the brakes on aggressive Fed easing speculation. Today’s weaker-than-expected Core-HICP data (actual 1.8% vs forecast 1.9%) and yesterday’s German inflation (actual 1.6% y/y vs 1.9% previously) supported Ms. Lagarde’s view.

GBPUSD

GBPUSD traded negatively in a 1.3326-1.3423 range since yesterday, but the September uptrend line remains intact while prices are above 1.3300. GBPUSD suffered from Powell’s comments that suggested a slower pace of rate cuts. Prices are also suffering from angst over potential unfriendly-to-business policies of the new government.

USDJPY

USDJPY churned in a 142.37-144.54 range since Monday thanks to Japanese politics, a downgraded risk of BoJ rate cuts, and dovish comments from Fed Chair Powell. The new Japanese Prime Minister Shigeru Ishiba called an election for October 27. The BoJ Summary of Opinions suggested policymakers plan to leave rates unchanged for longer than expected.

AUDUSD and NZDUSD

AUDUSD has bounced in a 0.6898-0.6942 range since Friday’s close with traders digesting Powell’s dovish comments and the recent announcements of massive fiscal and monetary stimulus from China. Prices got additional support after August Retail Sales rose 0.7% m/m, well above the 0.4% forecast. NZDUSD is in the middle of its 0.6305-0.6350 band, supported by an improved business confidence survey.

USDMXN

USDMXN traded in a 19.6425-19.7190 range and is at 19.6875 in early NY. Prices bounced off the post-Powell comments low (19.5495) ahead of incoming President Claudia Sheinbaum’s inauguration today. Mexican markets are closed for the event.

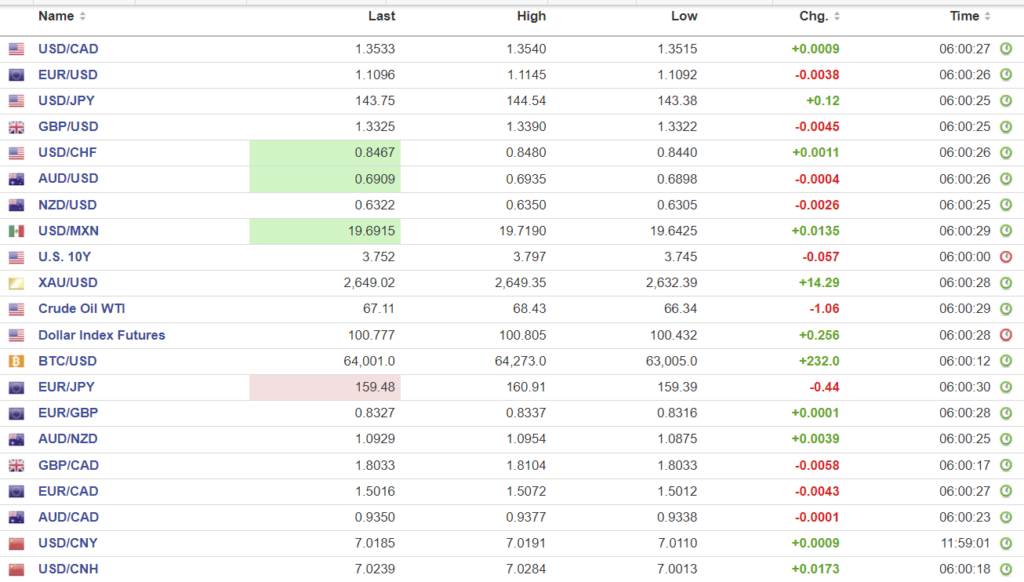

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0074 (prev. 7.0101)

Shanghai Shenzhen CS! 300 rose 8.48% to 4017.85 (as of September 30)

Chinese markets closed next week for Golden Week.

PBoC cut 7-day Repo Rate to 1.5% from 1.7%

Caixin September Manufacturing PMI 49.3 (50.4 on August), Services PMI 50.3 (51.4 in August). The survey points to a slowing economy in September while consumer sentiment was negative but that was before the slew of stimulus packages.

Chart: USDCNY and USDCNH

Source: Investing.com