- Canada October GDP rises 0.1% m/m

- US PCE rises 0.1% m/m; forecast 0.3% m/m

- US dollar opens mixed after quiet overnight session

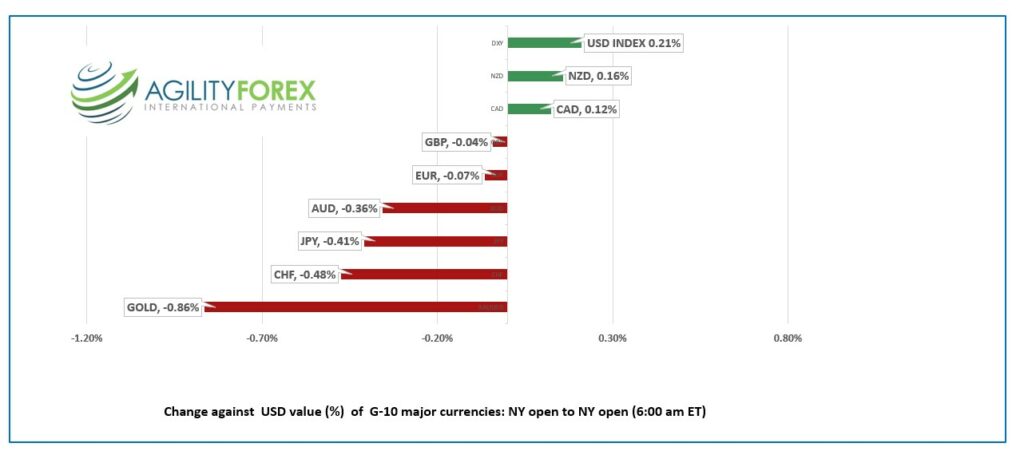

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3598-02, overnight range 1.3596-1.3657, close 1.3647

USDCAD traded with a negative bias overnight, sliding from 1.3657 in early Asia to 1.3596 just as NY opened today. The losses followed the increase in the S&P 500 futures which gained 0.45% before drifting lower in early NY trading.

Canada October GDP rose a mere 0.1%, down from September’s tepid 0.2% increase. Statistics Canada suggests that the November GDP result will be 0.1% as well. The economy is weak and supports the Bank of Canada’s suggestion for a pause in rate hikes.

WTI oil recovered yesterdays’ losses and gained 1.01% since Thursday’s close mainly due to Russia’s threat to cut oil production. Hmm, if sanctions of Russia crude imports and price caps for seaborne oil were effective, reduced Russian crude production shouldn’t be an issue.

USDCAD dipped to 1.3577 after the GDP data, but that was mainly due to a rebound in S&P 500 futures after weaker than expected US data.

USDCAD technical outlook.

The intraday technicals are bearish below 1.3630 looking for a move below 1.3580 to extend losses to the 1.3540-50 area. A break below 1.3540 sets the stage for a test of the August uptrend line at 1.3440. A move above 1.3630 argues for continued 1.3550-1.3750 consolidation.

For today, USDCAD support is at 1.3570 and 1.3540. Resistance is at 1.3640 and 1.3690

Today’s range 1.3550-1.3650

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

S&P 500 futures rallied following the modestly weaker than expected US economic data, but the move quickly faded. The Personal Consumption Expenditures (PCE) index ticked lower to 0.1% m/m compared to expectations for a 0.3% gain. Durable Goods Orders fell 2.1% m/m.

The impact of the data on markets is rather subdued thanks to “Bomb Cyclone.”

The massive winter storm also known as Snowpocalypse is ranging across a large swath of the US and Canada. In the past, such an event would severely curtail market activity as many market participants would struggle to get to the office. Not so much today.

The post-Covid world is a different kettle of fish. Employees embraced the work from home (WFH) concept so much so that the practice has created a new, passive holiday, Pretend-to Work-From Home-Day.

Employees will log-in as normal then do whatever strikes their fancy which usually does not involve toiling for their employer.

Yesterday, stronger than expected US Q3 GDP (actual 3.2% y/y vs forecast 2.9%) and lower than forecast weekly jobless claims (actual 216,000 vs forecast 222,000) raised fears of more aggressive Fed rate hikes. Wall Street stocks plunged with the S&P 500 falling 1.45%.

The theme carried over to Asia, but the major equity indexes managed to close higher than their worst levels. Japan’s Nikkei 225 index was the worst performing index losing 1.03%, partly due to higher-than-expected Japanese inflation.

European stocks are off their best levels and trading mixed. The German Dax index is up 0.27%, off its best level while the French CAC turned a minor gain into a modest loss.

S&P 500 futures bounced between gains and losses and are unchanged (as of 6:00 am PT). WTI oil is 1.50% higher but below this week’s high of $79.85/b.

EURUSD is in the middle of its 1.0588-1.0630 band. Traders ignored Eurozone data, but prices continue to be supported by ECB President Christine Lagarde’s hawkish monetary policy view.

GBPUSD retreated to 1.2044 following the US data and traded in a 1.2020-1.2089 range overnight, undermined by recession fears which are exacerbated by a rash of UK work stoppages. GBPUSD technicals are bearish below 1.2130.

USDJPY traded in a 132.17-132.80 overnight than popped to 133.01 after the US data dump, after found Japan CPI data was 3.8% y/y in November a tick higher than the October result. However, USDJPY gains may be hard to come by due to speculation of the BoJ will end its ultra-easy monetary early in 2023.

AUDUSD chopped in a 0.6662-0.6710 range with prices underpinned by higher commodity prices.

NOTE: The next Loonieviews is January 3, 2023.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

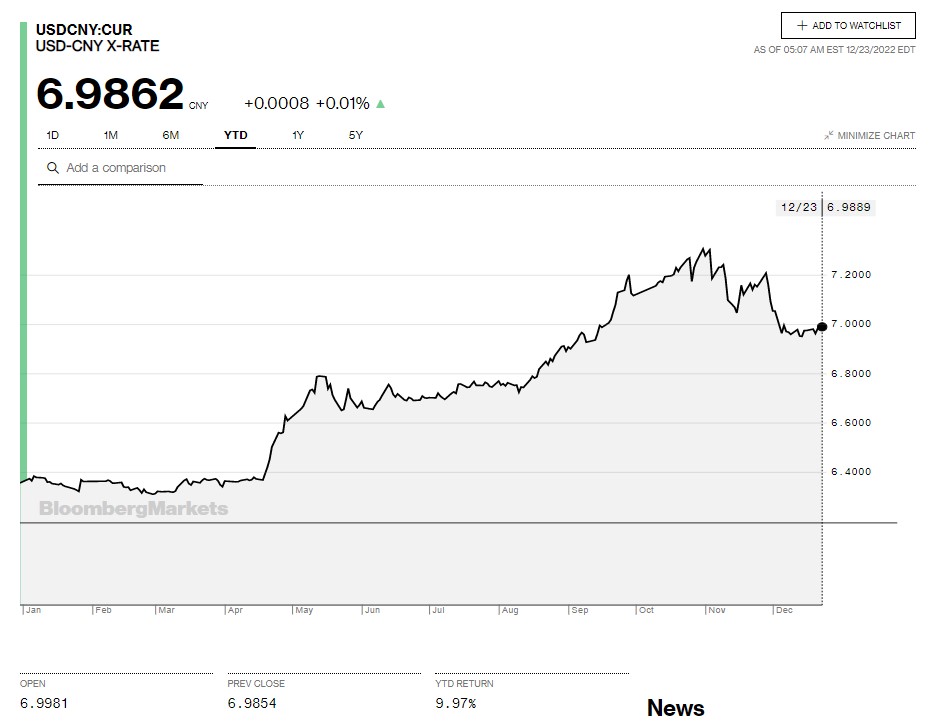

China Snapshot

Today’s Bank of China Fix: 6.9810, previous 6.9713

Shanghai Shenzhen CSI 300 fell 0.20% to 3828.22

Chart: USDCNY year-to-date

Source: Bloomberg