August 13, 2024

- PPI ex food and energy rises less than expected

- Oil rises on Iran /Israel risks.

- US dollar opens little changed and remains rangebound

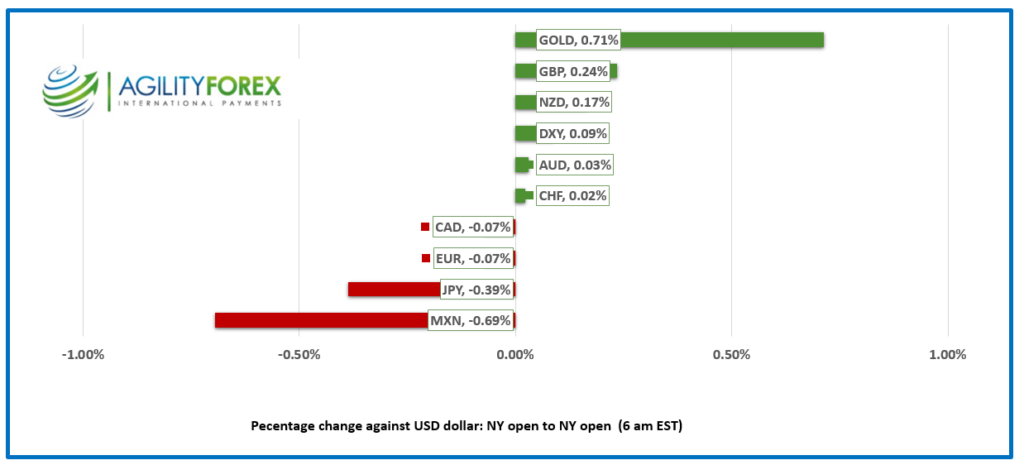

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3731, overnight range 1.3727-1.3748, previous close 1.3744

USDCAD is trading sideways and awaiting a fresh catalyst. That may come today in the form of US PPI data. A weaker than expected result will reinforce the current Fed rate cut outlook and renew US dollar selling pressure. USDCAD will slide in sympathy.

Oil prices rallied and filled the gap from July 22. That’s When WTI closed at 79.71 and opened at 78.23 the next day on the news Biden quit the presidential campaign. Rising Iran and Israel tensions have lifted prices steadily and WTI traded in a 79.31-80.14 range overnight. Fears of supply disruptions if (when)Iran attacks Israel are being held in check by concerns about an oil glut if Opec raises production in October. The International Energy Agency (IEA) agrees and said markets could swing from a deficit to a surplus in Q4.

USDCAD Technicals

The intraday USDCAD technicals are modestly bearish while trading below 1.3750, looking for a break of support in the 1.3690-1.3710 zone to extend losses to the 1.3650 area. A move above 1.3750 targets 1.3790, then 1.3840.

Fibonacci retracement analysis of the 11July-5August range suggests that the breech of 1.3768, the 50% retracement level followed by the break below the 61.8% level (1.3725) points to a retest of support at 1.3660.

For today, USDCAD support is at 1.3710 and 1.3680. Resistance is at 1.3740 and 1.3770. Today’s Range 1.3680-1.3780

Chart: USDCAD 4 hour

Source: DailyFX

Equities Mixed

Asian equity indexes closed with gains, highlighted by a robust 2.83% surge in Japan’s Topix. In contrast, the Australian ASX 200 lagged, rising just 0.17%. European bourses erased early gains and are down across the board, led by a 0.27% decline in the German Dax. S&P 500 futures are flat, and the US 10-year Treasury yield stands at 3.908%.

Producer Prices Rise Less Than Expected

Producer Prices were Fed friendly, at least for those anticipating a series of rate cuts beginning in September. The headline index rose 0.1% m/m, as expected but lower than the 0.2% increase in June. However, the more important PPI, ex-Food and Energy was flat (0% m/m vs forecast 0.2% ). Even better the June result was revised lower, to 0.3% from 0.4%. The US dollar retreated on the news.

Missiles Also Expected to Fall

Iran’s highly anticipated retaliation for Israel’s assassination of a Hamas leader in a Tehran suburb is expected imminently. The Israeli military remains on high alert, while the Pentagon has deployed the USS Abraham Lincoln strike force. Iran faces pressure to respond decisively to avoid losing influence and appearing weak.

EURUSD

EURUSD is at the top of its 1.0913-1.0947 range with the peak occurring post-PPI. Today’s disappointing German ZEW data weighed on sentiment, with the Current Situation index falling to -77.3 from July’s -68.9, and Economic Sentiment dropping sharply to 19.2 from 41.8 in July. ZEW President Achim Wambach noted, “In the current survey, we observe the strongest decline in economic expectations over the past two years. Expectations for the eurozone, the US, and China also deteriorate markedly, particularly impacting export-intensive German sectors.”

GBPUSD

GBPUSD rallied from 1.2761 to 1.2813 following a robust employment report. However, prices have since eased to 1.2790 in New York. The UK unemployment rate rose to 4.2% for April-June, slightly below the forecast of 4.5% and down from 4.6% previously. Average earnings increased by 5.4%, above the expected 4.6% but below the previous 5.7%. Analysts suggest today’s data will not alter the BoE outlook.

USDJPY

USDJPY traded in a 146.92-147.95 range but slid to 146.99 in the wake of the soft US PPI report. The move was short lived and USDJPY popped to 147.36. Japan’s parliament has summoned BoJ Governor Kazuo Ueda to a special session next week to discuss the recent rate hike. As Desi Arnaz famously said, “Ueda has some ‘splaining to do.”

AUDUSD and NZDUSD

AUDUSD rallied overnight, climbing from 0.6579 to 0.6610, pushing prices just above yesterday’s New York opening level. The Westpac Consumer Confidence Index jumped to 2.8% from -1.1% in July, while the National Australian Bank Business Conditions Index rose to 6 from 4. The wage price Index remained unchanged at 4.1% q/q, indicating a tight labor market that supports the RBA’s stance on keeping interest rates elevated.

NZDUSD inched higher in a 0.6016-0.6610 range ahead of tomorrow’s RBNZ monetary policy meeting, with the odds slightly favoring a dovish hold.

USDMXN

USDMXN consolidated yesterday’s gains, trading within an 18.9639-19.0865 range. Prices remain supported by concerns that Banxico may cut interest rates again, despite the latest increase in inflation. Governor Victoria Rodríguez suggested that the rise in inflation was temporary and that inflationary pressures would ease soon.

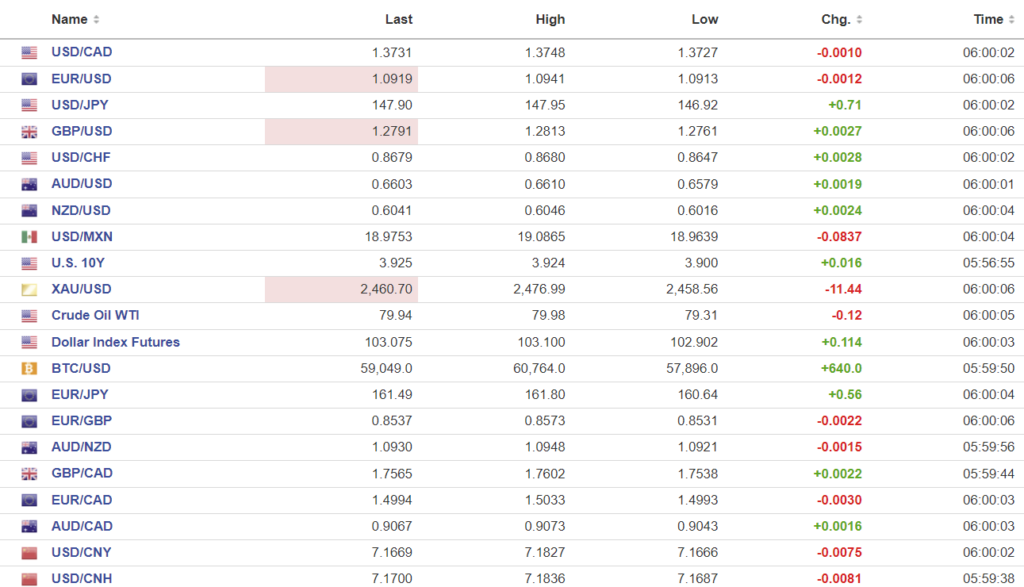

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1479 vs exp. 7.1760 (prev. 7.1458))

Shanghai Shenzhen CSI 300 fell rose 0.26% to 3334.39.

Bloomberg reports that analysts are concerned that Chinese authorities meddling in the bond market detaches market from fundamentals and undermines long term investor confidence. Friday, authorities ordered rural banks in China’s Jiangxi province not to settle recent purchases of government bonds. The intervention helped lift the 10-year yield from 2.12% to 2.22%.

Chart: USDCNY and USDCNH

Source: Investing.com