Source: ventralaquest.com

- Putin missile bombardment on civilians’ lifts US Treasury yields

- Bank of England ramps up bond-buying support program

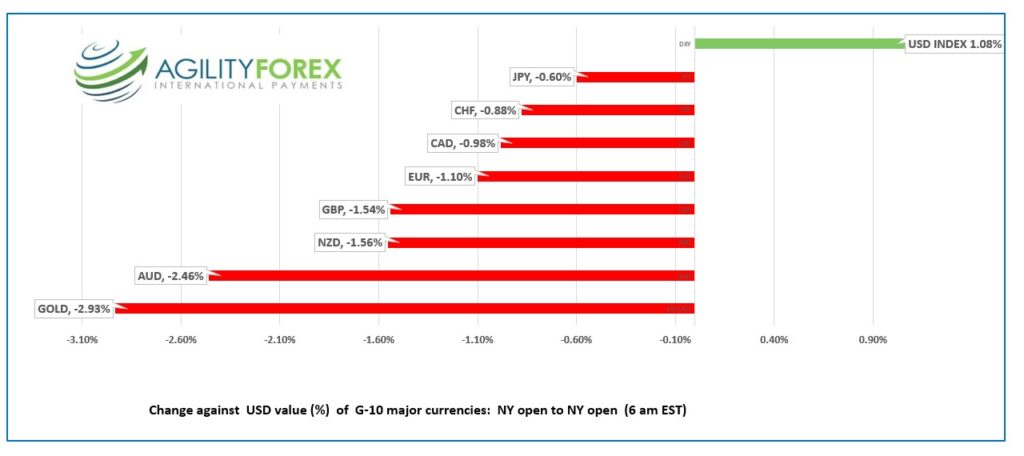

- US dollar remains bid, AUD underperforms.

FX at a glance:

Source: IFXA Ltd/RP

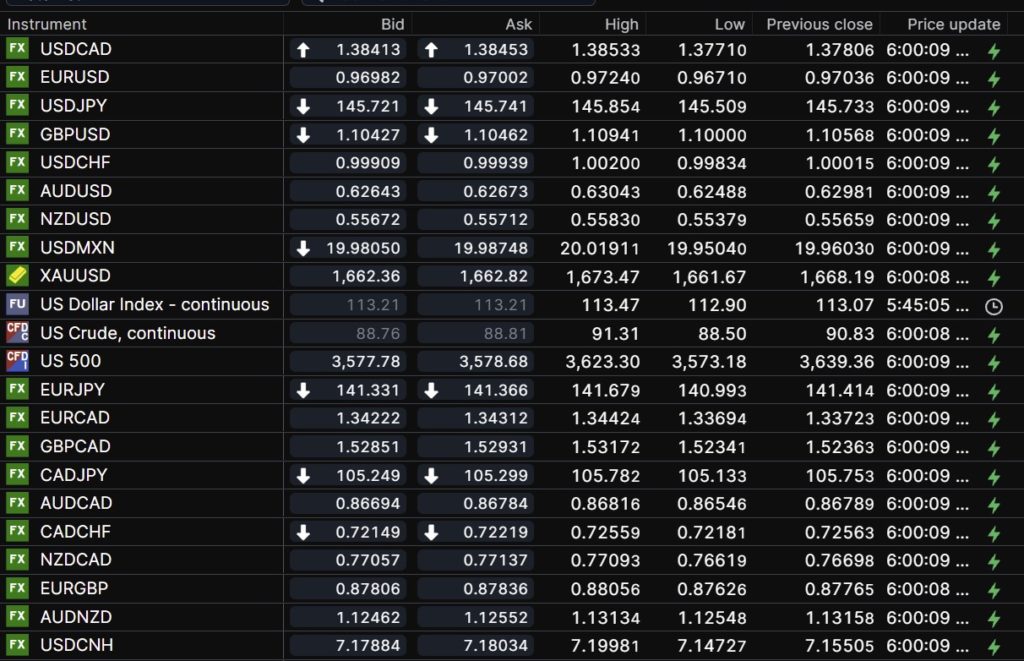

USDCAD Snapshot: open 1.3841-45, overnight range 1.3703-1.3853, close 1.3734

Friday’s Canadian employment report proved to be a non-issue for traders. They were more concerned about the US nonfarm payrolls report which was stronger than expected. Analysts declared that the results would not motivate the Fed to slow the pace of rate hikes, and the US dollar caught a bid.

USDCAD rallied Monday, reaching a new 2022 peak before consolidating the gains overnight. Prices dropped to 1.3768 in NY trading when the 10-year US Treasury yield retreated from its overnight peak and lifted S&P 500 futures, although they are still below yesterday’s close.

WTI oil prices surged from Friday’s low of $87.43 to $91.31/b yesterday. Prices retreated rapidly overnight and WTI is trading at $$88.85/b in NY. Concerns about supply shortages after Opec announced production cuts were alleviated 9somewhat) by concerns around Chinas economic growth outlook.

There are no Canadian economic reports today.

USDCAD Technical outlook

The intraday technicals are bearish following the drop below 1.3820, which sets up a test of minor support at 1.3760. A break below 1.3760 targets 1.3700, while a move above 1.3820 puts the spotlight on 1.3860. Longer term, the USDCAD technicals are bullish above 1.3620, the uptrend line from September 14.

For today, USDCAD support is at 1.3760 and 1.3700. Resistance is at 1.3820 and 1.3860. Today’s range: 1.3720-1.3820

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Ukrainian citizens and global financial markets were very unhappy with Putin’s’ targeted missile bombardment of civilians over the weekend. President Biden responded with a pledge to Ukraine President Zelenskiy to deliver advanced missile defence systems. Traders responded with a shift to risk aversion mode.

Monday, Fed Vice Chair Lael Brainard warned “Monetary policy will be restrictive for some time to ensure that inflation moves back to target over time. It will take time for the cumulative effect of tighter monetary policy to work through the economy broadly and to bring inflation down.”

Monday was a partial holiday in the US (Columbus Day). Trading volumes were very light, and Wall Street closed with small losses. Asian markets traded lower overnight led by a 2.64% drop in Japan’s Nikkei 225 index.

European equities opened soft and then added to the losses in European morning trade. The German Dax is down0.88%. The UK FTSE’s 1.24% decline is exacerbated by domestic issues. S&P 500 futures are down 0.89% pointing to a negative open on Wall Street.

The benchmark US 10-year Treasury yield touched 4.007% overnight before slipping to 3.931% in NY.

Gold traders are more afraid of higher US rates than a frustrated Putin escalating the Ukraine war. XAUUSD retraced all its October gains and fell from $1729.00 on October 4 to $1661.10 in Europe today.

EURUSD churned in a 0.9671-0.9724 range since Friday’s NY close. Prices churned with news of the Russian response to Ukraine blowing up a bridge linking Crimea to Ukraine, and rumors (since denied) that Germany supports a plan for joint EU debt issuance to combat the energy crisis. EURUSD was further pressured by rising US Treasury yields.

GBPUSD chopped about in a 1.1000-1.1107 range. Prices dropped to the low as risk aversion peaked, and US Treasury yields soared. GBPUSD rebounded from the low after the Bank of England intervened to alleviate dysfunction in the UK Gilt market and announced, “it will widen its gilt purchase operations to include index linked gilts.” The UK employment data was not a factor.

USDJPY traders taunted the Ministry of Finance and the Bank of Japan when they rallied the currency pair from 145.51 to 145.85. As usual, there were plenty of comments from officials warning “they were closely watching FX moves and would respond with urgency.”

AUDUSD was the worst performing major G-10 currency since Friday’s NY open, falling 2.46%. AUDUSD selling due to broad US dollar demand from higher Treasury yields was exacerbated by concerns around the weak Chinese Services data and a drop in Australia Consumer Confidence to -0.9% from 3.9% in September.

There isn’t any US data of note.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

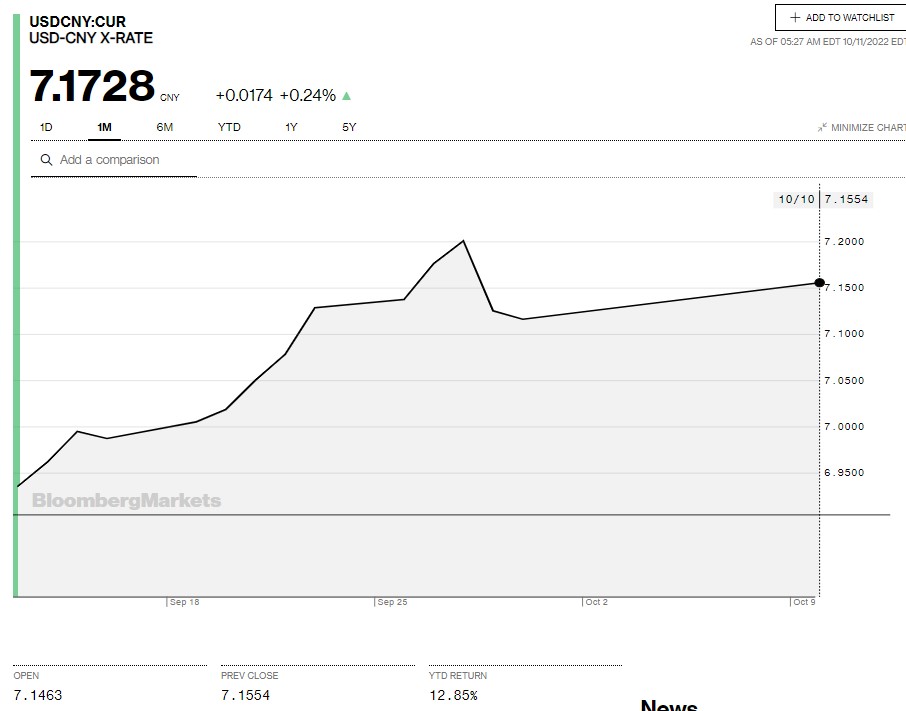

China Snapshot

Today’s Bank of China Fix: 7.1075, Monday, 7.0992, Sept. 30: 7.0998

Shanghai Shenzhen CSI 300: 3727.69 September 30 close 3804.94

China Securities Daily suggests PboC will cut RRR in Q4

Caixin September Services PMI dipped to 49.3 from 55 in August.

Xi Jinping’s Covid policies continue to weigh on risk sentiment. Shanghai has mandatory bi-weekly Covid testing.

Chart: USDCNY 1 month

Source: Saxo Bank